Aicinām vēl šonedēļ piedalīties lietotāju apmierinātības aptaujā!

Paldies par viedokli!

Regulations Regarding the Application of the Customs Procedure - TransitIssued pursuant to 1. General Provisions1. The Regulation prescribes: 1.1. individual conditions in relation to the application and drawing up of the customs procedure - transit - and also the procedures by which a transit declaration shall be invalidated; 1.2. the procedures by which the authorisation of the TIR carnet holder shall be issued, amended, suspended, renewed, and annulled; 1.3. the procedures by which the authorisation of an authorised consignor under the TIR procedure shall be issued, amended, suspended, renewed, and annulled, and also the procedures for the use of the authorisation; 1.4. the guaranteeing association in the Republic of Latvia which conforms to the conditions laid down in Article 1(q) and also Article 6 and Part I of Annex 9 to Customs Convention on the International Transport of Goods under Cover of TIR Carnets of 14 November 1975 (hereinafter - the TIR Convention of 1975) and which is a member of the international organisation specified in Article 6(2bis) of the TIR Convention of 1975; 1.5. the procedures by which the State Revenue Service and the guaranteeing association shall perform the approval of the road vehicles and containers for the transport of goods under customs seals specified in Articles 12 and 13 of the TIR Convention of 1975, the approval of the certificate of approval of a road vehicle, and the renewal of the validity of the certificate of approval of a road vehicle. 2. The terms used in the Regulation: 2.1. railway undertaking - a person registered in the Republic of Latvia which is moving goods in the territory of the Republic of Latvia as a carrier, using rail transport; 2.2. calculation of the debt of customs charges which may incur - the calculation of the debt of the customs duty, excise duty, and value added tax which may incur; 2.3. ITDB system - the International TIR Data Bank to be administrated by the TIR Secretariat of the Economic Commission for Europe of the United Nations Organisation; 2.4. holder of the procedure - a holder of the Union transit procedure or a holder of the common transit procedure; 2.5. TIR procedure - the TIR procedure specified in accordance with the TIR Convention of 1975; 2.6. authorisation of the TIR carnet holder - an authorisation giving the right to the holder of the authorisation to use the TIR procedure; 2.7. third country - a country or territory outside the customs territory of the Union; 2.8. empowered employee of the guaranteeing association - the authorised expert of the association Autopārvadātāju asociācija "Latvijas auto" [Association of Road Transport Operators Latvijas auto] who is entitled to perform an expert-examination of the conformity of vehicles and containers in accordance with Annexes 3 and 7 to the TIR Convention of 1975; 2.9. approval of vehicles or containers - the approval of vehicles or containers for the transport of goods under customs seals specified in accordance with Articles 12 and 13 of the TIR Convention of 1975; 2.10. certificate of approval of the vehicle - the certificate of approval of the vehicle for the transport of goods under customs seals specified in Annex 4 to the TIR Convention of 1975. 3. The performance and the end of the transit procedure shall be controlled by the State Revenue Service. 4. In accordance with the conditions laid down in Article 1(q) and also Article 6 and Part I of Annex 9 to the TIR Convention of 1975, the guaranteeing association of the Republic of Latvia is the Association of Road Transport Operators Latvijas auto (hereinafter - the guaranteeing association). 2. Calculation of the Debt of Customs Charges which May Incur5. Upon applying the Union transit procedure or the common transit procedure, the holder of the procedure shall submit to the customs office of departure the calculation of the debt of customs charges which may incur. 6. If, in accordance with the laws and regulations in the field of customs, the holder of the procedure is not required to submit a guarantee for the debt of customs charges of value added tax, "0 EUR" shall be indicated in the calculation of the debt of customs charges which may incur as the debt of customs charges of value added tax which may incur. 7. The holder of the procedure shall not provide the calculation referred to in Paragraph 5 of this Regulation to the customs office of departure if all of the following conditions are met: 7.1. the procedure is applied, using the status of the authorised consignor (hereinafter - the authorised consignor) specified in Article 233(4)(a) of Regulation (EU) No 952/2013 of the European Parliament and of the Council of 9 October 2013 laying down the Union Customs Code (hereinafter - Regulation No 952/2013); 7.2. the holder of the procedure is a railway undertaking or has received the status of the authorised economic operator in accordance with Article 39 of Regulation No 952/2013 (hereinafter - the authorised economic operator); 7.3. the holder of the procedure has developed the procedures for the supervision of the use of customs guarantees and coordinated them with the State Revenue Service. 3. Authorisation of the TIR Carnet Holder3.1. Issuing of the Authorisation of the TIR Carnet Holder8. The guaranteeing association shall issue the authorisation of the TIR carnet holder in the form of an electronic document. 9. In order to receive the authorisation of the TIR carnet holder, a person shall submit an application to the guaranteeing association. The following information regarding the person shall be indicated in the application: 9.1. the name; 9.2. the registration number assigned by the Enterprise Register of the Republic of Latvia; 9.3. the legal address; 9.4. the postal address, telephone number, electronic mail address, fax number (if any), the given name and surname of the contact person. 10. The guaranteeing association shall issue the authorisation of the TIR carnet holder if: 10.1. the person has been registered in the Republic of Latvia; 10.2. the State Revenue Service has established that the person conforms to the requirements referred to in Paragraph 13 of this Regulation; 10.3. the person is a member of the guaranteeing association; 10.4. the person, in accordance with paragraph 1(c) of Part II of Annex 9 to the TIR Convention of 1975, has proved knowledge in the application of the TIR Convention of 1975 and has received the certificate for the application of the TIR procedure issued by the guaranteeing association; 10.5. the person, in accordance with paragraph 1(b) of Part II of Annex 9 to the TIR Convention of 1975, has sound financial standing and sufficient current assets for the fulfilment of liabilities. This shall be assessed by calculating the following according to the data indicated in the previous annual statement or the statement of the relevant period of the current year: 10.5.1. the total liquidity coefficient (to be calculated by dividing the sum total of current assets by the sum total of current liabilities). The abovementioned coefficient shall not be less than 0.5; 10.5.2. the financial stability coefficient - the proportion of liabilities in the balance sheet (to be calculated by dividing the sum total of liabilities by the sum total of the balance sheet). The abovementioned coefficient may not exceed 1; 10.6. the person has confirmed its resolution to fulfil the declaration of commitment (specified in accordance with paragraph 1(e) of Part II of Annex 9 to the TIR Convention of 1975) and the regulations regarding the use of regular TIR carnets; 10.7. the following documents have been issued to the person: 10.7.1. the licence for international carriage of goods by goods vehicle for reward; 10.7.2. a permit of the European Community for the performance of carriage of goods by goods vehicles for reward in the territory of the European Union; 10.7.3. a copy of the permit of the European Community for the performance of carriage of goods by goods vehicles for reward in the territory of the European Union which has been issued for one year; 10.7.4. a document certifying the knowledge of the manager of carriage by road of the person - a certificate of professional competence for carriage of goods and passengers by road. 11. The guaranteeing association shall, within three working days after receipt of the application referred to in Paragraph 9 of this Regulation, verify the conformity of the person with the requirements referred to in Sub-paragraphs 10.1, 10.3, 10.4, 10.5, 10.6, and 10.7 of this Regulation. 12. If the guaranteeing association establishes that the person conforms to the requirements referred to in Sub-paragraphs 10.1, 10.3, 10.4, 10.5, 10.6, and 10.7 of this Regulation, it shall, within one working day, send a request to the State Revenue Service to provide the opinion on the conformity of the person with the requirements referred to in Paragraph 13 of this Regulation. The request of the guaranteeing association shall be accompanied by a copy of the application referred to in Paragraph 9 of this Regulation. 13. The State Revenue Service shall, within 10 working days after receipt of the request referred to in Paragraph 12 of this Regulation, assess the conformity of the person with the following requirements: 13.1. whether the person conforms to the conditions of paragraph 1(d) of Part II of Annex 9 to the TIR Convention of 1975; 13.2. whether a founder, member of the board or council of the person (legal person) has not been found guilty of a criminal offence regarding money laundering, misappropriation, accepting prohibited benefits, commercial bribery, accepting bribes, giving of bribes, misappropriation of a bribe, or intermediation in bribery, and also a coercive measure has not been applied to the person (legal person) for the relevant criminal offences in accordance with the Criminal Law; 13.3. whether the person has no debts of taxes, duties, and other debts of mandatory payments specified by the State or the time periods for the respective payments have been extended (suspended, divided) in accordance with the procedures laid down in the laws and regulations governing the field of taxes and the person is making payments in accordance with the decision of the tax administration (payment schedule) or execution of the decision of the tax administration has been suspended for the time period of pre-trial investigation or in accordance with Section 11 of the Customs Law. 14. The State Revenue Service shall, within one working day after assessment, send the opinion to the guaranteeing association on the conformity of the person with the requirements referred to in Paragraph 13 of this Regulation. 15. If the State Revenue Service has provided a positive opinion on the conformity of the person with the requirements referred to in Paragraph 13 of this Regulation, the guaranteeing association shall, within three working days after receipt of the abovementioned opinion: 15.1. issue the authorisation of the TIR carnet holder; 15.2. submit a submission to the State Revenue Service in the ITDB system to register the person as a TIR carnet holder. 16. The guaranteeing association shall, within three working days, take the decision on refusal to issue the authorisation of the TIR carnet holder if the following has been established: 16.1. the person has indicated information that does not conform to the requirements referred to in Paragraph 9 of this Regulation or false information; 16.2. the person does not conform to the requirements referred to in Paragraphs 10 and 13 of this Regulation. 17. The State Revenue Service shall, within one working day after receipt of the submission referred to in Sub-paragraph 15.2 of this Regulation, register the person in the ITDB system as a TIR carnet holder. 18. The guaranteeing association shall, within one working day after taking of the decision referred to in Paragraph 16 of this Regulation, notify the decision in writing to the person who has submitted the application referred to in Paragraph 9 of this Regulation and to the State Revenue Service. 19. The decision of the guaranteeing association to issue the authorisation of the TIR carnet holder or on refusal to issue the authorisation of the TIR carnet holder may be appealed to the Administrative Court in accordance with the procedures laid down in the Administrative Procedure Law. 3.2. Suspension and Renewal of the Authorisation of the TIR Carnet Holder20. If the State Revenue Service establishes that a person who has received the authorisation of the TIR carnet holder no longer conforms to the requirements referred to in Sub-paragraph 13.3 of this Regulation, the State Revenue Service shall, within one working day, send a notification to the guaranteeing association regarding the need to suspend the authorisation of the TIR carnet holder issued to the person. 21. The guaranteeing association shall, within three working days, take the decision to suspend the authorisation of the TIR carnet holder if at least one of the following conditions has been met: 21.1. it has established that the person who has received the authorisation of the TIR carnet holder does not conform to the conditions for the receipt of the authorisation; 21.2. it has received the notification referred to in Paragraph 20 of this Regulation. 22. The guaranteeing association shall, within one working day after taking of the decision to suspend the authorisation of the TIR carnet holder: 22.1. notify it to the person who has received the authorisation of the TIR carnet holder and the State Revenue Service in writing; 22.2. submit a submission to the State Revenue Service in the ITDB system to suspend the authorisation of the TIR carnet holder. 23. The State Revenue Service shall, within one working day after receipt of the submission referred to in Sub-paragraph 22.2 of this Regulation, register the suspension of the authorisation of the TIR carnet holder in the ITDB system. 24. If the authorisation of the TIR carnet holder has been suspended, the person: 24.1. shall be responsible for the ending of such TIR procedures which were applied prior to suspension of the authorisation; 24.2. shall, within 80 days after suspension of the authorisation of the TIR carnet holder, eliminate the established non-conformities and inform the guaranteeing association thereof. 25. The guaranteeing association shall, within three working days after receipt of the information referred to in Sub-paragraph 24.2 of this Regulation, if the authorisation of the TIR carnet holder has been suspended: 25.1. in accordance with Sub-paragraph 21.1 of this Regulation - take the decision to renew the authorisation of the TIR carnet holder and submit a submission to the State Revenue Service in the ITDB system for the revocation of the suspension of the authorisation of the TIR carnet holder in the ITDB system; 25.2. in accordance with Sub-paragraph 21.2 of this Regulation - prior to taking the decision to renew the authorisation of the TIR carnet holder, submit a submission to the State Revenue Service in the ITDB system for the revocation of the suspension of the authorisation of the TIR carnet holder in the ITDB system. 26. The State Revenue Service shall, within three working days after receipt of the submission referred to in Sub-paragraph 25.1 of this Regulation, revoke the suspension of the authorisation of the TIR carnet holder in the ITDB system. 27. The State Revenue Service shall, within 10 working days after receipt of the submission referred to in Sub-paragraph 25.2 of this Regulation, assess the conformity of the person with the requirements referred to in Paragraph 13 of this Regulation and if: 27.1. the person conforms to the abovementioned requirements, shall revoke the suspension of the authorisation of the TIR carnet holder in the ITDB system within one working day; 27.2. the person does not conform to the abovementioned requirements, shall reject the submission referred to in Sub-paragraph 25.2 of this Regulation in the ITDB system within five working days and send the relevant opinion to the guaranteeing association. 28. The guaranteeing association shall, within three working days after receipt of the notification of the ITDB system regarding the revocation of the suspension of the authorisation of the TIR carnet holder, take the decision to renew the authorisation of the TIR carnet holder if it had been suspended in accordance with Sub-paragraph 21.2 of this Regulation. 29. The guaranteeing association shall, within one working day after taking of the decision to renew the authorisation of the TIR carnet holder, notify it to the person and the State Revenue Service in writing. 30. The decision of the guaranteeing association to suspend or renew the authorisation of the TIR carnet holder may be appealed to the Administrative Court in accordance with the procedures laid down in the Administrative Procedure Law. 3.3. Annulment of the Authorisation of the TIR Carnet Holder31. If the State Revenue Service establishes that a person who has received the authorisation of the TIR carnet holder no longer conforms to the requirements referred to in Sub-paragraphs 13.1 and 13.2 of this Regulation, the State Revenue Service shall, within one working day, send a notification to the guaranteeing association regarding the need to annul the authorisation of the TIR carnet holder issued to the person. 32. The guaranteeing association shall, within three working days, annul the authorisation of the TIR carnet holder if: 32.1. the person has not eliminated the non-conformities indicated in the decision within 80 days after suspension of the authorisation of the TIR carnet holder; 32.2. the person has not met any of the conditions for the receipt of the authorisation of the TIR carnet holder or the obligations determined by the status of the TIR carnet holder and it is not possible to eliminate the established non-conformities; 32.3. the guaranteeing association has received the notification referred to in Paragraph 31 of this Regulation; 32.4. the person who has received the authorisation of the TIR carnet holder submits the application regarding the annulment of the abovementioned authorisation. 33. The guaranteeing association shall, within one working day after taking of the decision to annul the authorisation of the TIR carnet holder issued to the person: 33.1. notify it to the person and the State Revenue Service in writing; 33.2. submit a submission to the State Revenue Service in the ITDB system to annul the authorisation of the TIR carnet holder. 34. The State Revenue Service shall, within one working day after receipt of the submission referred to in Sub-paragraph 33.2 of this Regulation, register the annulment of the authorisation of the TIR carnet holder in the ITDB system. 35. If the authorisation of the TIR carnet holder is annulled, the person shall be responsible for the ending of such TIR procedures which had been applied prior to annulment of the authorisation. 36. The decision of the guaranteeing association to annul the authorisation of the TIR carnet holder may be appealed to the Administrative Court in accordance with the procedures laid down in the Administrative Procedure Law. 3.4. Amending of the Authorisation of the TIR Carnet Holder37. The guaranteeing association shall, within three working days after receipt of the application of the TIR carnet holder regarding changes in the information referred to in Sub-paragraph 9.1 or 9.3 of this Regulation, verify whether the abovementioned changes have been registered in the Enterprise Register of the Republic of Latvia. 38. The guaranteeing association shall, within three working days, make amendments to the authorisation of the TIR carnet holder and submit a submission to the State Revenue Service in the ITDB system to make amendments to the registration data of the authorisation of the TIR carnet holder if: 38.1. the application of the TIR carnet holder regarding changes in the information referred to in Sub-paragraph 9.4 of this Regulation has been received; 38.2. changes in the information referred to in Sub-paragraph 9.1 or 9.3 of this Regulation have been registered in the Enterprise Register of the Republic of Latvia. 39. The State Revenue Service shall, within three working days after receipt of the submission referred to in Paragraph 38 of this Regulation, register amendments to the registration data of the authorisation of the TIR carnet holder in the ITDB system. 40. The decision of the guaranteeing association to amend the authorisation of the TIR carnet holder may be appealed to the Administrative Court in accordance with the procedures laid down in the Administrative Procedure Law. 4. Approval of Vehicles and Containers in Accordance with the Provisions of the TIR Convention of 197541. Approval of a vehicle or container shall be requested by the owner or holder of the vehicle or container. 42. The certificate of approval of the vehicle shall be issued by the guaranteeing association. 43. The certificate of approval of the vehicle shall be approved, registered and the extension of its term of validity shall be confirmed by the customs offices stipulated by the State Revenue Service. 44. In order to receive the certificate of approval of the vehicle or to extend its term of validity, the owner or holder of the vehicle or container shall present the relevant vehicle or container to the empowered employee of the guaranteeing association. 45. The empowered employee of the guaranteeing association shall verify: 45.1. the conformity of the vehicle with Annex 2 to the TIR Convention of 1975; 45.2. the conformity of the container with Annex 7 to the TIR Convention of 1975. 46. The empowered employee of the guaranteeing association shall, within one working day, issue the certificate of approval of the vehicle if it is established in the check that: 46.1. the vehicle conforms to Annex 2 to the TIR Convention of 1975; 46.2. the container conforms to Annex 7 to the TIR Convention of 1975. 47. If, during the check, the empowered employee of the guaranteeing association establishes that the vehicle does not conform to Annex 2 to the TIR Convention of 1975 or the container does not conform to Annex 7 to the TIR Convention of 1975, he or she shall, within three working days after completing the check of the vehicle or container, inform the applicant for approval of the established non-conformities. 48. If the non-conformities referred to in Paragraph 47 of this Regulation have been eliminated, the owner or holder of the vehicle or container shall repeatedly present the vehicle or container to the empowered employee of the guaranteeing association. 49. The empowered employee of the guaranteeing association shall fill in the following in the certificate of approval of the vehicle: 49.1. boxes 1, 2, 3, 4, 5, 6, and 8 and place the stamp of the guaranteeing association on the left side of box 7 upon performing the primary approval and issuing a new certificate; 49.2. box 9 and place the stamp of the guaranteeing association on its left side upon extending the term of validity of the certificate of approval of the vehicle. 50. The customs office shall approve and register the certificate of approval of the vehicle, and also approve the extension of its term of validity if the following conditions are met concurrently: 50.1. the vehicle or container has been presented to the relevant customs office; 50.2. the vehicle conforms to Annex 2 to the TIR Convention of 1975, while the container conforms to Annex 7 to the TIR Convention of 1975; 50.3. the empowered employee of the guaranteeing association has issued the certificate of approval of the vehicle or has drawn up the extension of its term of validity accordingly. 51. If the customs office establishes that the conditions referred to in Paragraph 50 of this Regulation have been met, it shall, within one working day, approve and register the certificate of approval of the vehicle, and also approve the extension of the term of validity of the certificate of approval of the vehicle. 52. The guaranteeing association shall regularly update the following information on its website: 52.1. the list of empowered employees of the guaranteeing association, indicating their given name, surname, telephone number, electronic mail address, and working hours; 52.2. the fee approved by the guaranteeing association for the issuance of the certificate of approval of the vehicle. 53. The State Revenue Service shall regularly update the list of customs offices responsible for the approval and registration of the certificates of approval of the vehicle on its website. 5. TIR Procedure54. Upon applying a TIR procedure (except for the case if a TIR procedure is applied only for goods released in the customs procedure - export), the TIR carnet holder shall submit to the customs office of departure the calculation of the debt of customs charges which may incur. 55. Upon applying a TIR procedure, the TIR carnet holder must be the owner or holder of the road vehicle indicated in the TIR carnet. 56. If the TIR carnet holder registered in the Republic of Latvia uses a road transport vehicle of a third party, it shall require a permission of the guaranteeing association for the use of the road transport vehicle of the third party under the TIR procedure. 57. The permission referred to in Paragraph 56 of this Regulation shall not be required if the TIR carnet holder is using the following of a third party: 57.1. a trailer or semi-trailer; 57.2. a road transport vehicle used to replace a road transport vehicle that has been damaged during a TIR procedure. 6. Authorisation of a TIR Consignor6.1. General Provisions58. The authorisation of an authorised consignor under the TIR procedure which has been specified in Section 23 of the Customs Law (hereinafter - the authorisation of the TIR consignor) shall be issued, amended, suspended, renewed, revoked, and annulled by the State Revenue Service. 59. The application for the receipt, amending, renewal, and revocation of the authorisation of the TIR consignor and the documents related thereto shall be submitted to the State Revenue Service in printed form or in the form of an electronic document, or using the electronic declaration system (EDS) of the State Revenue Service. 60. The State Revenue Service shall notify the decisions to issue, amend, suspend, renew, revoke, and annul the authorisation of the TIR consignor in the electronic declaration system (EDS) of the State Revenue Service. 6.2. Application of the Authorisation of the TIR Consignor61. The authorisation of the TIR consignor shall be applied for the bringing out of Union and non-Union goods from the customs territory of the Union. 62. The authorisation of the TIR consignor shall not be applied: 62.1. to the following goods which have been excluded from the TIR guarantee system in the customs territory of the Union: 62.1.1. undenatured ethyl alcohol of an alcoholic strength by volume of 80 % vol. or higher classified under the commodity code of the Harmonised Commodity Description and Coding System (HS) (hereinafter - the HS commodity code) 2207 10; 62.1.2. spirits, liqueurs, and other spirituous beverages classified under the item 2208 of HS commodities; 62.1.3. cigars and cigarillos containing tobacco classified under the HS commodity code 2402 10; 62.1.4. cigarettes containing tobacco classified under the HS commodity code 2402 20; 62.1.5. smoking tobacco containing or not containing tobacco substitutes in any amount classified under the HS commodity codes 2403 11 and 2403 19; 62.2. to motor cars traveling by their own means and classified under the item 8703 of the HS commodities; 62.3. to non-Union goods intended to be carried with one TIR carnet if the debt of the customs duty, value added tax, and excise duty for non-Union goods which may incur exceeds the sum specified in Article 163 of Commission Implementing Regulation (EU) 2015/2447 of 24 November 2015 laying down detailed rules for implementing certain provisions of Regulation (EU) No 952/2013 of the European Parliament and of the Council laying down the Union Customs Code (hereinafter - Regulation No 2015/2447); 62.4. to the goods of strategic significance; 62.5. to radioactive substances, nuclear materials, and other sources of ionising radiation; 62.6. to weapons and special means to which the requirements laid down in the Law on the Handling of Weapons and Special Means are applicable; 62.7. to narcotic and psychotropic substances, raw materials intended for the manufacture of such substances (precursors), new psychoactive substances or articles containing them, and medicinal products containing these substances; 62.8. to waste; 62.9. to endangered specimens of wild animal and plant species and their derivatives (CITES goods); 62.10. to other goods the transit of which is prohibited or restricted. 63. Upon applying the TIR procedure, a holder of the authorisation of the TIR consignor shall use the customs seals (Annex 1) and stamp (Annex 2) approved by the State Revenue Service. 6.3. Issuing of the Authorisation of the TIR Consignor64. In order to receive the authorisation of the TIR consignor, a person shall submit an application to the State Revenue Service indicating the following information therein: 64.1. the name of the person; 64.2. the legal address; 64.3. the registration and identification number provided for in Article 1(18) of Commission Delegated Regulation (EU) 2015/2446 of 28 July 2015 supplementing Regulation (EU) No 952/2013 of the European Parliament and of the Council as regards detailed rules concerning certain provisions of the Union Customs Code (hereinafter - Commission Regulation No 2015/2446) (hereinafter - the EORI number); 64.4. the postal address, telephone number, electronic mail address, fax number (if any), the given name and surname of the contact person; 64.5. the address of the place (premises or territory) where the applying of the TIR procedure is intended; 64.6. the procedures for the recording of goods (the type and content). The procedures for the recording of goods shall not be indicated if the person is the authorised consignor or the authorised economic operator. 65. The application referred to in Paragraph 64 of this Regulation shall be accompanied by the plan (in one copy) of such place where the applying of the TIR procedure is intended. The name of the person and the EORI number shall be indicated in the plan, the address and location of the premises or territory shall be accurately marked and clearly identified. 66. The application referred to in Paragraph 64 of this Regulation shall not be accompanied by the plan of the place where the applying of the TIR procedure is intended if the abovementioned place is used upon applying another authorisation issued by the State Revenue Service. 67. The State Revenue Service shall issue the authorisation of the TIR consignor if: 67.1. the person has been registered in the Republic of Latvia; 67.2. the person has not been punished for serious or repeated violations of the customs or tax provisions laid down in Section 28 of the Customs Law; 67.3. a founder, member of the board or council of the person (legal person) has not been found guilty of a criminal offence regarding money laundering, misappropriation, accepting prohibited benefits, commercial bribery, accepting bribes, giving of bribes, misappropriation of a bribe, or intermediation in bribery, and also a coercive measure has not been applied to the person (legal person) for the relevant criminal offences in accordance with the Criminal Law; 67.4. the guaranteeing association has provided a positive opinion on the conformity of the person with the requirements referred to in Paragraph 70 of this Regulation; 67.5. the person has no debts of taxes, duties, and other debts of mandatory payments specified by the State or the time periods for the respective payments have been extended (suspended, divided) in accordance with the procedures laid down in the laws and regulations governing the field of taxes and the person is making payments in accordance with the decision of the tax administration (payment schedule) or execution of the decision of the tax administration has been suspended for the time period of pre-trial investigation or in accordance with Section 11 of the Customs Law; 67.6. the person has sound financial standing and has sufficient current assets for the fulfilment of obligations. It shall be assessed by calculating the following according to the data indicated in the statement of the previous year: 67.6.1. the total liquidity coefficient (to be calculated by dividing the sum total of current assets by the sum total of current liabilities). The abovementioned coefficient shall not be less than 1; 67.6.2. the financial stability coefficient - the proportion of liabilities in the balance sheet (to be calculated by dividing the sum total of liabilities by the sum total of the balance sheet). The abovementioned coefficient may not exceed 0.5. 68. The State Revenue Service shall, within five working days after receipt of the application referred to in Paragraph 64 of this Regulation, send a request to the guaranteeing association to provide the opinion on the conformity of the person with the requirements referred to in Paragraph 70 of this Regulation. 69. The guaranteeing association shall, within 10 working days after receipt of the request of the State Revenue Service referred to in Paragraph 68 of this Regulation, send the opinion to the State Revenue Service on the conformity of the person with the requirements referred to in Paragraph 70 of this Regulation. 70. The guaranteeing association shall assess the conformity of the person with the following requirements: 70.1. if the person has received the authorisation of the TIR carnet holder: 70.1.1. whether the person does not have violations in application of the TIR procedure; 70.1.2. whether claims and objections not solved in accordance with the TIR Convention of 1975 regarding carriage performed by the person have been received from the State Revenue Service or another competent authority of the member state to the TIR Convention of 1975; 70.2. if the person has not received the authorisation of the TIR carnet holder: 70.2.1. whether the person holds the status of an associated member of the guaranteeing association; 70.2.2. whether the person has confirmed its resolution to fulfil and fulfils the declaration of commitment (specified in accordance with paragraph 1(e) of Part II of Annex 9 to the TIR Convention of 1975) regarding the use of regular TIR carnets; 70.2.3. whether the person, in accordance with paragraph 1(c) of Part II of Annex 9 to the TIR Convention of 1975, has proved knowledge in the application of the TIR Convention of 1975 and has received the certificate for the application of the TIR procedure issued by the guaranteeing association. 71. The State Revenue Service shall, within a month after receipt of the application referred to in Paragraph 64 of this Regulation and the documents referred to in Paragraph 65 of this Regulation, verify whether all the conditions for accepting such application have been met. If the State Revenue Service concludes that all the information necessary for taking the decision has been indicated in the application, it shall notify the person that the application has been accepted. 72. The State Revenue Service shall consider the opinion of the guaranteeing association on the person and issue the authorisation of the TIR consignor or take the decision on refusal to issue the authorisation of the TIR consignor. 73. The State Revenue Service shall take the decision on refusal to issue the authorisation of the TIR consignor if it establishes that the person: 73.1. has indicated information that does not conform to the requirements referred to in Paragraph 64 or 65 of this Regulation or false information; 73.1. does not conform to the condition or criterion for issuing the authorisation referred to in Paragraph 67 of this Regulation. 74. The State Revenue Service shall indicate the following information in the authorisation of the TIR consignor: 74.1. the information necessary for identification of such place where the holder of the authorisation of the TIR consignor has the right to apply the TIR procedure, and also the supervising customs office (customs control point) of such place; 74.2. the procedures by which the circulation of information and documents between the holder of the authorisation of the TIR consignor and the relevant supervising customs office (customs control point) takes place; 74.3. the measures to be taken in order to ensure conformity with the provisions for the application of the TIR procedure; 74.4. information regarding the customs seal and stamp to be used by the holder of the authorisation of the TIR consignor. 75. The State Revenue Service shall ensure the holder of the authorisation of the TIR consignor with the possibility of using an information system (computerised transit control system) for the submission of a customs declaration in electronic form to such extent that the State Revenue Service and the holder of the authorisation would be able to perform all the activities necessary for customs clearance according to the conditions of the authorisation of the TIR consignor. 76. The State Revenue Service shall, within five working days after taking the decision to issue the authorisation of the TIR carnet holder or on refusal to issue the authorisation of the TIR carnet holder, inform the guaranteeing association thereof in writing. 6.4. Suspension, Renewal, Revocation, and Annulment of the Authorisation of the TIR Consignor77. If the guaranteeing association establishes that the person who has received the authorisation of the TIR consignor no longer conforms to the requirements referred to in Paragraph 70 of this Regulation, it shall, within one working day, send a negative opinion on the person to the State Revenue Service. 78. The State Revenue Service shall take the decision to suspend the operation of the authorisation of the TIR consignor if: 78.1. the person does not conform to any of the conditions for the receipt of the authorisation of the TIR consignor; 78.2. the State Revenue Service has received the opinion referred to in Paragraph 77 of this Regulation. 79. The holder of the authorisation of the TIR consignor shall, within 80 days after suspension of the authorisation of the TIR consignor, eliminate the non-conformities indicated in the decision referred to in Paragraph 78 of this Regulation and shall inform the State Revenue Service thereof. 80. Prior to taking the decision to renew the authorisation of the TIR consignor, the State Revenue Service shall, within five working days after receipt of the information referred to in Paragraph 79 of this Regulation, send a request to the guaranteeing association to assess the conformity of the person with the requirements referred to in Paragraph 70 of this Regulation. 81. The guaranteeing association shall, within 10 working days after receipt of the request referred to in Paragraph 80 of this Regulation, send the opinion to the State Revenue Service on the conformity of the person with the requirements referred to in Paragraph 70 of this Regulation. 82. The State Revenue Service shall take the decision to renew the authorisation of the TIR consignor if the person has eliminated the non-conformities indicated in the decision referred to in Paragraph 78 of this Regulation within 80 days after suspension of the authorisation. 83. The State Revenue Service shall, within 10 working days, take the decision to revoke the authorisation of the TIR consignor if: 83.1. it establishes that the person has not eliminated the non-conformities indicated in the decision referred to in Paragraph 78 of this Regulation and has not informed the State Revenue Service about elimination of the abovementioned non-conformities within 80 days after suspension of the authorisation of the TIR consignor; 83.2. it establishes that any of the conditions for the receipt of the authorisation of the TIR consignor referred to in Paragraphs 67 and 70 of this Regulation has not been fulfilled and it is not possible to eliminate the established non-conformities; 83.3. it has not received the application of the holder of the authorisation of the TIR consignor regarding revocation of the authorisation. 84. The State Revenue Service shall take the decision to annul the authorisation of the TIR consignor in the case specified in Article 27(1) of Regulation No 952/2013. 85. The State Revenue Service shall, within five working days after taking of the decision to suspend, renew, revoke, or annul the authorisation of the TIR consignor, inform the guaranteeing association thereof in writing. 6.5. Amending of the Authorisation of the TIR Consignor86. The holder of the authorisation of the TIR consignor shall, within five working days, inform the State Revenue Service in writing of all changes in the documents and information referred to in Paragraphs 64 and 65 of this Regulation. 87. The information provided in accordance with Paragraph 86 of this Regulation must be easy to identify and clearly attributable to further activity related to the authorisation of the TIR consignor. 88. If necessary, the State Revenue Service shall, within a month after receipt of the information referred to in Paragraph 86 of this Regulation, make amendments to the authorisation of the TIR consignor and ensure the possibility of using an information system (computerised transit control system) for the submission of a customs declaration in electronic form in accordance with the conditions referred to in Paragraph 75 of this Regulation or shall take the decision on refusal to make amendments to the authorisation of the TIR consignor. 89. The State Revenue Service shall take the decision on refusal to make amendments to the authorisation of the TIR consignor if it establishes that the person has provided inappropriate or false information on making changes in the documents and information referred to in Paragraph 64 or 65 of this Regulation. 90. The State Revenue Service shall, within five working days after making of amendments to the authorisation of the TIR consignor, inform the guaranteeing association thereof in writing. 7. Other Conditions for the Application and Ending of the Transit Procedure7.1. Action of a Person if Inaccurate Information is Established in the Declaration after Release of Goods in Transit Procedure and Prior to the Start of the Movement of Goods91. If, after release of goods in transit procedure and prior to the start of the movement of goods, the holder of the procedure, the TIR carnet holder, the holder of the authorisation of the TIR consignor, or the authorised consignor establishes that inaccurate information has been indicated in the declaration, it shall inform the customs office of departure of the established non-conformities. 92. The person referred to in Paragraph 91 of this Regulation shall present goods to the customs office of departure and shall coordinate further actions with the customs office of departure. The customs office of departure shall close the transit procedure. 7.2. Movement of Goods with Fixed Transport Installations93. Upon applying the transit procedure to petroleum products moved along a pipeline, the holder of the procedure shall declare goods in accordance with the following procedures: 93.1. the consignor of goods shall, once in 24 hours (excluding weekends and public holidays) after applying the transit procedure for petroleum products which have been sent with one deed of delivery and acceptance, submit the deed of delivery and acceptance of goods to the State Revenue Service; 93.2. the consignee of goods shall, once in 24 hours (excluding weekends and public holidays) after receipt of petroleum products which have been sent with one deed of delivery and acceptance, submit the deed of delivery and acceptance of goods to the State Revenue Service; 93.3. the holder of the procedure shall ensure that the Union transit procedure is applied for, goods are released in the Union transit procedure, the Union transit procedure is performed, the Union transit procedure is ended, and information is exchanged according to the procedures stipulated by the customs office. 94. Upon applying the transit procedure to natural gas moved along pipelines, the holder of the procedure shall: 94.1. declare goods by submitting the deed of delivery and acceptance of goods; 94.2. ensure that the Union transit procedure is applied for, goods are released in the Union transit procedure, the Union transit procedure is performed, the Union transit procedure is ended, and information is exchanged according to the procedures stipulated by the customs office. 95. Upon applying the transit procedure to electricity, the holder of the procedure shall: 95.1. declare goods by submitting the deed of coordination; 95.2. ensure that the Union transit procedure is applied for, goods are released in the Union transit procedure, the Union transit procedure is performed, the Union transit procedure is ended, and information is exchanged according to the procedures stipulated by the customs office. 7.3. Movement of Goods by Rail Transport96. Upon applying the transit procedure to goods which do not have the customs status of Union goods and which are moved within the scope of the transit procedure by rail from a customs office of departure located in the territory of the Republic of Latvia to a customs office of destination located in the territory of the Republic of Latvia, the international railway consignment note set by Annex 1 to the Agreement on International Goods Transport by Rail of 1 November 1951 may be used as the transit declaration if the following conditions are met: 96.1. the holder of the procedure is a railway undertaking; 96.2. the holder of the procedure regularly uses the Union transit procedure; 96.3. the holder of the procedure has not been punished for serious or repeated violations of the customs or tax provisions laid down in Section 28 of the Customs Law; 96.4. the holder of the procedure has received an authorisation for the use of the comprehensive guarantee; 96.5. the holder of the procedure ensures that the Union transit procedure is applied for, goods are released in the Union transit procedure, the Union transit procedure is performed, the Union transit procedure is ended, and information is exchanged according to the procedures stipulated by the customs office. 97. In accordance with Article 297(1) and 314(2)(b) of Regulation No 2015/2447, the customs office of departure or the authorised consignor shall determine the time period for the ending of the transit procedure of up to 40 days if the following conditions are met: 97.1. the holder of the procedure is a railway undertaking or the authorised economic operator; 97.2. the transit procedure is applied to the goods referred to in Paragraph 98 of this Regulation which are moved along rail in the time period from 1 November to 31 March. 98. The regulation referred to in Paragraph 97 of this Regulation shall apply to the goods classified in the following HS chapters: 98.1. in Chapter 10 - the goods referred to in items 1001, 1002, 1003, 1004, and 1005 of goods; 98.2. in Chapter 23 - the goods referred to in items 2301, 2302, 2303, 2304, 2305, and 2306 of goods; 98.3. in Chapter 27 - the goods referred to in items 2701, 2702, 2704 of goods and in the code 2710 19 of goods; 98.4. in Chapter 29 - the goods referred to in item 2902 of goods. 7.4. Missing Goods99. If the customs office of destination or a person who has received the authorisation referred to in Article 233(4)(b) of Regulation No 952/2013 for the use of the status of the authorised consignee (hereinafter - the authorised consignee) establishes a non-conformity of the quantity of the presented goods with the quantity indicated in the Union transit declaration, the missing goods shall not be considered removed from customs supervision in the customs territory of the Union if all of the following conditions are met: 99.1. the goods in a vehicle or container with which they are moved in the Union transit procedure have been loaded outside the customs territory of the Union and the vehicle or container has not been opened in the customs territory of the Union. This condition shall be considered conformed to also if opening of the vehicle or container in the customs territory of the Union is performed by customs services or other competent services; 99.2. a seal of the customs office of a third country or a goods seal of the consignor of goods has been affixed to a vehicle or container and it conforms to the international goods security (seal) standards (for example, ISO 17712:2013, Freight containers - Mechanical seals) or the essential characteristics and technical specification specified in Article 301(1) of Regulation No 2015/2447, it has been indicated in the transport documents or in the customs documents drawn up for goods in the third country, and it is intact. This condition shall not be applicable to international carriage of goods by road transport if goods are brought into the customs territory of the Union by crossing the land border with a third country; 99.3. upon applying the Union transit procedure, a customs seal or a seal of the authorised consignor has been affixed to a vehicle or container according to the authorisation, and it is intact; 99.4. there are not damages on a vehicle or container which attest to the possibility of accessing the goods or to possible access to the goods; 99.5. the holder of the procedure submits a document of the consignor of goods or of such carrier which has brought in the corresponding vehicle or container directly from the customs territory located outside the Union, or a document of the authorised consignee in international carriage of rail freight which has been prepared in printed form or in electronic form and contains the following information: 99.5.1. the details of the consignor, carrier, or authorised consignee in international carriage of rail freight - the name, address, registration number (if any), contact details (telephone number, electronic mail address (if any)), signature, and date of preparation of the document; 99.5.2. information regarding the accompanying documents of goods in which inappropriate quantity of goods has been indicated by mistake (the number, date of the document, and the inappropriate quantity of goods indicated by mistake); 99.5.3. the actual quantity of goods loaded in the vehicle or container. 100. In addition to the holder of the procedure, the carrier of goods or the authorised consignee is entitled to submit the documents referred to in Sub-paragraph 99.5 of this Regulation to the State Revenue Service. 101. The holder of the procedure, the carrier of goods, or the authorised consignee shall submit an application and the documents referred to in Sub-paragraph 99.5 of this Regulation to the State Revenue Service in printed form or in the form of an electronic document, or using the electronic declaration system (EDS) of the State Revenue Service. 8. Invalidation of a Transit Declaration after Release of Goods102. The holder of the procedure or TIR carnet holder shall submit the application for invalidation of a transit declaration after release of goods in the cases specified in Article 148(4)(b) and (c) of Regulation No 2015/2446 to the State Revenue Service in printed form or in the form of an electronic document, or using the electronic declaration system (EDS) of the State Revenue Service. 103. The State Revenue Service shall invalidate the transit declaration indicated in the application referred to in Paragraph 102 of this Regulation if: 103.1. the holder of the procedure or TIR carnet holder has presented the goods declared therein to the customs office of departure and has coordinated further actions with the customs office of departure; 103.2. the holder of the procedure or TIR carnet holder has drawn up more than one transit declaration with identical information for the goods by mistake (information regarding goods, the quantity of goods, the data of the vehicle, customs seals, and the number of accompanying documents). In such cases the holder of the procedure or TIR carnet holder is not required to present the goods to the customs office of departure and may continue the performance of the transit procedure applied. 9. Closing Provisions104. Cabinet Regulation No. 426 of 25 July 2017, Regulations Regarding the Application of the Customs Procedure - Transit (Latvijas Vēstnesis, 2017, No. 148; 2018, No. 209), is repealed. 105. The authorisations of the TIR carnet holder and the authorisations of the TIR consignor which have been issued to persons prior to the day of the coming into force of this Regulation shall be valid until the annulment of the relevant authorisation or issuing of a new authorisation. 106. If according to the methodology for ensuring customs supervision which has been previously coordinated with the State Revenue Service, the simplification of a Union transit procedure referred to in Paragraph 96 of this Regulation was applied prior to the coming into force of this Regulation, its application shall be continued until revocation of the abovementioned simplification. Prime Minister A. K. Kariņš Minister for Finance J. Reirs

Annex 1 Essential Characteristics and Technical Specification of Seals to be Used under the TIR Procedure of the Authorised ConsignorThe seals under the TIR procedure of the authorised consignor shall conform to the requirements laid down in Article 301 of Commission Implementing Regulation (EU) 2015/2447 of 24 November 2015 laying down detailed rules for implementing certain provisions of Regulation (EU) No 952/2013 of the European Parliament and of the Council laying down the Union Customs Code and to the following essential characteristics of technical specifications: 1. Strap seal of Tyden Seal type (image) shall consist of: 1.1. a metal strap which is 21.43 cm in length and 0.95 cm in width. The strap shall bear the inscription "LATVIJAS MUITA" [customs of Latvia], the number of the authorisation of the TIR consignor, and the identification number thereof consisting of two letters and seven digits; 1.2. a locking mechanism. 2. Strap seal of Tyden Seal type shall have an extending strap the width of which is 4-5 mm, the length of perforation - 8-12 mm, and the interval between perforations - 13 mm.

Image Minister for Finance J. Reirs

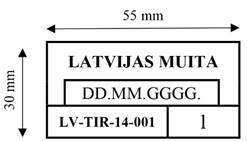

Annex 2 Stamp of the Holder of the Authorisation of the TIR Consignor1. Dimensions of the stamp (image): 1.1. length - 55 mm; 1.2. width - 30 mm. 2. The specimen of the stamp depicts the text: 2.1. in the upper part - the inscription "LATVIJAS MUITA"; 2.2. in the centre - date (day, month, year); 2.3. in the bottom left corner - the number of the authorisation of the authorised TIR consignor; 2.4. in the bottom right corner - the serial number of the stamp.

Image Minister for Finance J. Reirs Translation © 2021 Valsts valodas centrs (State Language Centre) |

Document information

Title: Muitas procedūras – tranzīts – piemērošanas noteikumi

Status:

In force

Language:   Related documents

|

|

Latvijas Vestnesis, the official publisher ensures legislative acts systematization function on this site. All Likumi.lv content is intended for information purposes. |

About Likumi.lv News archive For feedback Training Contacts |

Mobile version Terms of service Privacy policy Cookies Accessibility |

|