|

Republic

of Latvia

Cabinet

Regulation No. 691

Adopted 25 October 2016

|

Regulations Regarding Consumer

Credit

Issued pursuant to

Section 8, Paragraph four of the Consumer Rights Protection

Law

and Section 7, Paragraph two of the Advertising Law

I. General Provisions

1. This Regulation prescribes:

1.1. the requirements in relation to the advertising content

of a consumer credit service;

1.2. the content of the information to be provided prior to

entering into a consumer credit agreement (hereinafter - the

credit agreement) and the procedures for providing it;

1.3. the conditions for provision of ancillary services;

1.4. the requirements to be brought forward for the credit

agreement and the information to be included therein;

1.5. the method for calculating the annual percentage rate of

charge;

1.6. the conditions for a foreign currency loan and a variable

interest rate loan;

1.7. informing of a consumer during the term of operation of

the credit agreement;

1.8. early repayment of a credit and fair reduction of the

total costs of the credit;

1.9. the requirements to be applied to certain types of credit

agreements;

1.10. the requirements to be set for giving advice;

1.11. the duties of credit intermediaries and representatives

of credit intermediaries;

1.12. the legal framework for a consumer crediting against

movable property pledge.

2. Terms used in this Regulation:

2.1. total amount payable by consumer - the sum of the total

amount of the credit and the total cost of the credit to the

consumer;

2.2. annual percentage rate of charge - the total costs of the

credit to the consumer, expressed as an annual percentage of the

total amount of credit granted to the consumer, including the

costs in accordance with Paragraphs 5, 6, and 7 of this

Regulation;

2.3. borrowing rate - the interest rate expressed as a fixed

or variable percentage applied on an annual basis to the amount

of credit drawn down;

2.4. fixed borrowing rate - the only borrowing rate on which

the creditor and the consumer agree in the credit agreement for

the entire duration of the credit agreement or on several

borrowing rates for partial periods using exclusively a fixed

specific percentage. If not all borrowing rates are determined in

the credit agreement, the borrowing rate shall be deemed to be

fixed only for the partial periods for which the borrowing rates

are determined exclusively by a fixed specific percentage agreed

on the conclusion of the credit agreement. Credit agreements for

which the borrowing rate is regularly reviewed in accordance with

changes in the index rates (Libor, Euribor or

others) indicated in the credit agreement, shall not be

considered to be credit agreements with a fixed borrowing

rate;

2.5. foreign currency loan - a credit denominated in a

currency other than that in which the consumer receives the

income or holds the assets from which the credit is to be repaid,

or denominated in a currency other than that of the Member State

of the European Economic Area in which the consumer is

resident;

2.6. total amount of credit - the ceiling or the total sums of

the borrowing available to the consumer under a credit

agreement;

2.7. member benefit organisations - organisations which have

been established for the mutual benefit of its members, do not

make profits for any other person than its members, fulfil a

social purpose in accordance with the requirements of legal acts,

receive and manage investments, provide credit services to its

members only, providing credit with an annual percentage rate of

charge lower than that prevailing on the market or subject to a

ceiling specified by legal acts, and membership in which is

restricted to persons residing or employed in a particular

location, to employees and retired employees of a particular

employer or to persons meeting other criteria specified in legal

acts, which determine the existence of a common bond between the

members;

2.8. linked credit agreement - a consumer credit agreement

which serves exclusively to fully or partly finance an agreement

for the supply of specific goods or the provision of a specific

service, and these two agreements form a commercial unit. A

consumer credit agreement and a contract on delivery of

particular goods or provision of a particular service form a

commercial unit in the following cases:

2.8.1. the credit is granted to the consumer by the goods

manufacturer, seller or service provider;

2.8.2. the credit is granted to the consumer by a third party

and the creditor uses the services of the manufacturer, seller or

service provider in connection with the conclusion or preparation

of the credit agreement; or

2.8.3. the credit is granted to the consumer by a third party

and the specific goods or specific service is explicitly

specified in the credit agreement; and

2.9. credit intermediary in an ancillary capacity - a

manufacturer, seller or service provider whose activity as credit

intermediary is not the main purpose of its trade, business or

profession.

3. This Regulation shall not apply to:

3.1. credit agreements concluded between an employer and an

employee, where the credit is granted free of interest or at an

annual percentage rate of charge lower than that prevailing on

the market and not offered to the public generally, and if the

issuance of credits is not the type of core activity of the

employer;

3.2. credit agreements concluded with investment companies or

with credit institutions for the purposes of allowing an investor

to carry out a transaction relating to one or more of the

financial instruments regulated in accordance with the laws and

regulations regarding the financial instrument market, where the

investment company or credit institution granting the credit is

involved in such transaction;

3.3. credit agreements which are the outcome of a settlement

reached in court or before another authority specified in laws

and regulations;

3.4. credit agreements which apply to covering of a debt in

the form of deferred payments without paying the interest rate

and other additional payments, except for the credit agreement

the repayment of which is secured by an immovable property or the

purpose of the credit is to acquire or retain a right in

immovable property;

3.5. credit agreements for loans granted to a restricted

public in accordance with the procedures laid down in laws and

regulations with a general interest purpose and at lower interest

rates than those prevailing on the market or free of interest or

on other terms which are more favourable to the consumer than

those prevailing on the market and at interest rates not higher

than those prevailing on the market. Chapters II, III, and V of

this Regulation shall be applied to such credit agreements the

repayment of which is secured by an immovable property or the

purpose of credit is to acquire or retain a right in immovable

property;

3.6. such hiring or leasing contracts where an obligation to

purchase the object of the contract by the consumer or the right

to acquire the object of the contract into ownership is not

provided for, or complete or partial disbursement of the value of

the object of the contract during the duration of the contract is

not provided for; and

3.7. credit agreements according to which credit is granted

free of interest and other additional payments, except for

payments which are related to credit security. This exception

shall not be applied to the credit agreement upon entering into

which the consumer is requested to deposit an item as security in

the creditor's safe-keeping and where the liability of the

consumer is strictly limited to that pledged item. The

requirements referred to in Paragraph 13, Sub-paragraphs 14.4,

14.5, and 14.6, as well as in Sub-paragraphs 56.3, 56.5, 56.7,

and 56.8 of this Regulation shall also apply to the credit

agreements referred to in this Sub-paragraph.

4. The conformity with these Regulations shall be supervised

by the Consumer Rights Protection Centre.

II. Calculation of the Annual

Percentage Rate of Charge

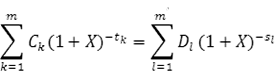

5. The annual percentage rate of charge shall be calculated in

accordance with the formula and terms set out in Annex 1 to this

Regulation, equating to the present value of all commitments

(drawdowns, repayments and charges), future or existing, agreed

by the creditor and the consumer.

6. In order to calculate the annual percentage rate of charge,

the total cost of the credit to the consumer shall be determined.

When calculating the total cost of the credit to the consumer,

the following charges shall not be taken into account:

6.1. any charges payable by the consumer for non-compliance or

inadequate compliance with any of the commitments laid down in

the credit agreement; and

6.2. charges which, for purchases of goods or services, except

the purchase price, the consumer pays, irrespective of whether

the transaction is effected in cash or on credit.

7. The costs of maintaining an account used for payment

transactions and drawdowns, as well as the costs of using a means

of payment for payment transactions and drawdowns, and other

costs relating to payment transactions shall be included in the

total cost of the credit to the consumer, except where the

opening of the account is optional and the costs of the account

are clearly and separately shown in the credit agreement or in

any other agreement concluded with the consumer.

8. The calculation of the annual percentage rate of charge

shall be based on the assumption that the credit agreement is to

remain valid for the period agreed and that the creditor and the

consumer will fulfil their obligations under the terms and by the

dates agreed by the parties in the credit agreement.

9. In a credit agreement allowing variations in the annual

percentage rate of charge or other charges contained in the

annual percentage rate of charge but unquantifiable at the time

of calculation, the annual percentage rate of charge shall be

calculated on the assumption that the borrowing rate and other

charges remain fixed and will remain applicable until the end of

the credit agreement.

10. In calculating the annual percentage rate of charge, the

creditor has the right to use the additional assumptions referred

to in Paragraphs 3 and 4 of Annex 1 to this Regulation.

11. For credit agreements the repayment of which is secured by

an immovable property or the purpose of the credit is to acquire

or retain a right in immovable property, for which the fixed

borrowing rate has been determined for the initial time period of

at least five years at the end of which an agreement regarding a

new fixed borrowing rate for the subsequent time period is

intended, the calculation of the additional descriptive annual

percentage rate of charge indicated in the European Standardised

Information Sheet (Annex 2) shall apply only to the time period

of the initial fixed borrowing rate, and it shall be based on an

assumption that the credit not repaid at the end of the time

period of the fixed borrowing rate has been repaid.

12. If the credit agreement the repayment of which is secured

by an immovable property or the purpose of the credit is to

acquire or retain a right in immovable property allows changes in

the borrowing rate, the consumer must be informed regarding the

potential impact of changes on the payments to be made by the

consumer and on the annual percentage rate of charge at least

using the European Standardised Information Sheet (Annex 2).

Additional annual percentage rate of charge which shows the

potential risks related to essential increase in the borrowing

rate, shall be calculated for the consumer. If the maximum limit

of the borrowing rate has not been determined, a warning shall be

added to such information that the total costs of credit which

are shown by the annual percentage rate of charge, may change.

This Paragraph shall not be applied to credit agreements to which

Paragraph 11 of this Regulation applies.

III. Requirements for Advertising

Credit Services

13. The following is prohibited in an advertisement offering a

consumer credit:

13.1. the encouraging of irresponsible borrowing. When

determining whether an advertisement encourages irresponsible

borrowing, the overall content and the way it is presented, its

design and the information provided in the advertisement

regarding the credit service which enables the consumer to take

an economically justified decision, shall be taken into

consideration. The following advertisement shall be considered as

advertisement encouraging irresponsible borrowing in any case

which:

13.1.1. invites a consumer to take a credit in unconsidered

way or without assessment its necessity;

13.1.2. invites to take a credit regardless of the financial

situation of the consumer;

13.1.3. causes or may cause an impression that taking of a

credit is risk-free;

13.1.4. causes or may cause an impression that a credit is the

most appropriate way how to solve financial problems;

13.1.5. influences or may influence the decision of the

consumer on concluding the credit agreement by additionally

offering to acquire goods or receive services or other advantages

if they have no direct relation to the use of the credit;

13.2. the provision of information regarding the option of

receiving credit to persons with a poor credit history.

14. An advertisement offering a consumer credit and indicating

the interest rate or other numerical information regarding credit

charges, in a clear, concise and prominent way by means of a

representative example, shall indicate the following (unless it

is otherwise determined in specific credit agreements):

14.1. the borrowing rate (fixed, variable or both) together

with information regarding the applicable charges included in the

total cost of the credit to the consumer;

14.2. the total amount of the credit;

14.3. the annual percentage rate of charge. Such information

shall be indicated in a visual advertisement in at least as

clearly prominent way as any interest rate or other equivalent

numerical information regarding the credit charges;

14.4. the duration of the credit agreement, if applicable;

14.5. in the case of a credit in the form of deferred payment

for specific goods or services, the price of the goods or

services and the amount of any initial payment;

14.6. the total amount payable by the consumer and the amount

of the instalments, where possible; and

14.7. a compulsory requirement to undertake an ancillary

service related to the credit agreement, such as compulsory

insurance, if the conclusion of an agreement for an ancillary

service is required in order to receive credit or receive it with

the terms and conditions offered, and the charges of the service

referred to cannot be determined in advance.

15. At least the information referred to in Sub-paragraphs

14.1, 14.2, and 14.3 of this Regulation shall be indicated, by

means of a representative example, in an advertisement for

overdraft credit to be repaid upon request or within three

months, if the advertisement has been formulated indicating the

interest rate or other numerical information regarding the credit

charges.

16. The information referred to in Sub-paragraphs 14.1, 14.2,

14.3, 14.4, 14.5, 14.6 (if applicable), and 14.7 of this

Regulation shall be indicated, by means of a representative

example, in an advertisement regarding the credit agreement for

the purchase of immovable property or the credit agreement

repayment of which is secured by an immovable property mortgage,

if the advertisement has been formulated indicating the interest

rate or other numerical information regarding the credit charges,

as well as:

16.1. the name of the creditor or credit intermediary or the

representative of the credit intermediary. If the credit

intermediary or representative of the credit intermediary

involved is a natural person, the given name, surname and

registration number in the register of intermediaries shall be

indicated;

16.2. a clear reference that the credit is secured by an

immovable property mortgage or other rights in relation to the

immovable property;

16.3. if applicable, the number of payments to be made;

16.4. if applicable, a warning that currency fluctuations may

affect the amount to be paid by the consumer.

17. The information referred to in Sub-paragraphs 14.1, 14.2,

14.4, 14.5, and 14.6 of this Regulation shall be indicated, by

means of a representative example, in an advertisement regarding

a credit agreement, in accordance with which the consumer is

required to repay the credit in a time period not exceeding three

months and negligible additional payments are requested for the

use of credit in comparison with the total amount of the credit

and the duration of the credit agreement, if the advertisement

has been formulated indicating the interest rate or other

numerical information regarding the credit charges.

18. The information referred to in Sub-paragraphs 14.1, 14.2,

14.4, and 14.6 of this Regulation shall be indicated, by means of

a representative example, in an advertisement regarding the

credit agreement, upon the conclusion of which the consumer is

requested to deposit an item as security in the creditor's

safe-keeping and where the liability of the consumer is strictly

limited to that pledged item, if the advertisement has been

formulated indicating the interest rate or other numerical

information regarding the credit charges.

19. Only the requirements referred to in Paragraph 13 of this

Regulation shall apply to such advertisement for a consumer

credit agreement, in accordance with which the creditor has

consented by acquiescence that the consumer uses funds exceeding

the balance of funds remaining in the consumer's settlement

account or the granted overdraft facility.

IV. Information to be Provided to

a Consumer Before Concluding a Credit Agreement

20. Before a consumer has undertaken obligations of the credit

agreement or accepted an offer, the creditor or credit

intermediary shall, on the basis of the credit terms and

conditions offered by the creditor and the preferences expressed

and information supplied by the consumer, if the consumer has

provided such, provide the consumer with the information needed

to compare different offers in order to take an informed decision

on whether to conclude the credit agreement.

21. The following shall be indicated in the information

provided to a consumer in accordance with Paragraph 20 of this

Regulation:

21.1. the type of credit;

21.2. the name, registration number, legal address and address

of the actual provision of services, if different from the legal

address, of the creditor and, if a credit intermediary is

involved, the credit intermediary. If the credit intermediary

involved is a natural person, the given name, surname, declared

place of residence and address of the actual provision of

services shall be indicated;

21.3. the total amount of credit and the conditions governing

the drawdown;

21.4. the duration of the credit agreement;

21.5. the good or service and the price thereof, if, in

accordance with the credit agreement, it is intended to grant a

loan in the form of deferred payment for the specific good or

service or it is anticipated to conclude the linked credit

agreement;

21.6. the borrowing rate, the conditions governing the

application of the borrowing rate, and the index rate, if such is

applied to the initial borrowing rate, as well as the periods,

conditions and procedure for changing the borrowing rate. If

different borrowing rates are applied to the credit, the

abovementioned information shall be shown on all the applicable

rates;

21.7. the annual percentage rate of charge and the total

amount payable by the consumer. The abovementioned information

shall be illustrated by means of a representative example

indicating all the assumptions used for calculation of the annual

percentage rate of charge. Where the consumer has informed the

creditor of one or more components of the preferred credit, the

creditor shall take the components indicated by the consumer into

account in the example. If a credit agreement provides different

ways of drawdown with different charges or borrowing rates and

the creditor uses the assumption set out in Annex 1,

Sub-paragraph 3.2 to this Regulation in the calculation of the

annual percentage rate of charge, he shall indicate that other

drawdown mechanisms for this type of credit agreement may result

in higher annual percentage rate of charges;

21.8. the amount, number and frequency of payments to be made

by the consumer, as well as the procedure by which payments will

be allocated to different outstanding balances charged at

different borrowing rates for the purpose of reimbursement (if

such procedure is specified);

21.9. the charges for maintaining one or several accounts

recording both payment transactions and drawdowns, indicating the

charges for using a means of payment for both payment

transactions and drawdowns, any other charges deriving from the

credit agreement and the conditions under which those charges may

be changed. The information referred to shall not be indicated if

the opening of the account in accordance with the credit

agreement is optional or is not provided for;

21.10. the notarial costs payable by the consumer on

conclusion of the credit agreement (if such are anticipated);

21.11. the obligation to enter into an ancillary service

contract relating to the credit agreement, for example, mandatory

insurance, where the conclusion of such a contract is compulsory

in order to obtain the credit or to obtain it on the terms and

conditions marketed;

21.12. the interest rate in the case of late payments and the

procedures for the application thereof, as well as any penalties

or other compensation for the non-compliance or inadequate

compliance with the contractual obligations (if such are

anticipated);

21.13. information regarding the consequences of missing

payments;

21.14. the sureties, where applicable;

21.15. information on the right of withdrawal from the credit

agreement;

21.16. the right of early repayment of the credit and

information concerning the creditor's right to compensation and

the procedures by which that compensation will be determined in

accordance with Paragraph 101 of this Regulation (if such is

anticipated);

21.17. the consumer's rights to be informed immediately and

free of charge, in compliance with the Consumer Rights Protection

Law, of the use of a database for the purposes of assessing the

ability of the consumer to repay the credit;

21.18. the consumer's right to be supplied, on request and

free of charge, with a copy of the draft credit agreement;

and

21.19. the period of time during which the creditor is bound

by the information provided prior to entering into contract.

22. The information referred to in Paragraph 21 of this

Regulation shall be provided in conformity with the Standard

European Consumer Credit Information form included in Annex 3 to

this Regulation on paper or using another durable medium. All the

information referred to is required to be equally visible. The

creditor has fulfilled the information requirements in compliance

with this Paragraph and the requirements specified in the

regulations on distance contracts for the provision of financial

services for informing the consumer prior to the conclusion of a

distance contract for financial services, if he has provided

information to the consumer in compliance with the form referred

to.

23. Other information not indicated in Paragraph 21 of this

Regulation, which is provided by the creditor to the consumer,

shall be included in a separate document to be appended to the

Standard European Consumer Credit Information form included in

Annex 3 to this Regulation.

24. The requirements referred to in Paragraphs 20, 21, 22, and

23 of this Regulation shall not apply to:

24.1. credit agreements which provide that the consumer is

required to repay the credit in a time period not exceeding three

months and with which negligible additional payments are

requested for the use of credit in comparison with the total

amount of the credit and the duration of the credit

agreement;

24.2. credit agreements in accordance with which the creditor

has consented by acquiescence that the consumer uses funds which

exceed the balance of funds in the consumer's settlement account

or the overdraft facility granted.

25. For credit agreements upon the conclusion of which the

consumer is requested to deposit an item as security in the

creditor's safe-keeping and where the liability of the consumer

is strictly limited to that pledged item before the consumer has

undertaken the liabilities of the credit agreement or agreed to

the offer, the creditor shall provide the information indicated

in Sub-paragraphs 21.3, 21.4, 21.6 of this Regulation in free

form, as well as the information regarding the total amount to be

paid by the consumer.

26. Upon request by the consumer, the creditor shall issue a

draft copy of the credit agreement free of charge, except where

the creditor does not wish to conclude a credit agreement with

the consumer at the time of the request being expressed.

27. If voice telephony has been used as a means of

communication between the creditor and consumer in accordance

with the regulations on distance contracts for the provision of

financial services, the description of financial services to be

provided in accordance with the abovementioned regulations shall

include at least the information referred to in Sub-paragraphs

21.3, 21.4, 21.5, 21.6, and 21.8 of this Regulation, as well as

information regarding annual percentage rate of charge

illustrated by means of a representative example and the total

amount to be paid by the consumer.

28. If the agreement has been concluded at the consumer's

request using a means of distance communication which does not

enable the information to be provided in accordance with

Paragraphs 20, 21, 22,and 23 of this Regulation, the creditor

shall provide the consumer with the information specified using

the Standard European Consumer Credit Information form (Annex 3)

immediately after the conclusion of the credit agreement.

29. Upon concluding the credit agreement under which payments

made by the consumer are not directed for an immediate repayment

of the total amount of credit, but are used to accumulate capital

in accordance with time periods and conditions laid down in the

credit agreement or in an ancillary agreement, the information

which in accordance with the requirements of Paragraphs 20, 21,

22, and 23 of this Regulation must be provided to the consumer

prior to entering into the credit agreement, shall include a

clear and concise statement that such credit agreement does not

provide for a guarantee of repayment of the total amount of

credit issued in accordance with the credit agreement, except the

case when such a guarantee is given.

30. In order to enable the consumer to assess whether the

proposed credit agreement is adapted to his needs and to his

financial situation, the creditor or credit intermediary shall

explain to the consumer, upon his or her request, the information

included in the Standard European Consumer Credit Information

form (Annex 3), as well as the essential characteristics of the

services proposed and the consequences which may arise to the

consumer, caused due to the non-compliance or inadequate

compliance with the agreement.

V. Information to be Provided to a

Consumer Prior to Concluding a Credit Agreement Regarding a

Credit the Repayment of which is Secured by an Immovable Property

or the Purpose of which is to Acquire or Retain a Right in

Immovable Property

31. A creditor or credit intermediary shall ensure that the

consumer has access, at any time, to general information in a

clear an concise form, free of charge, regarding credit

agreements on paper, using durable medium, or electronically. At

least the following shall be indicated in the abovementioned

information:

31.1. the name, registration number, legal address and actual

address of the provision of services, if different from the legal

address, of the provider of information. If the provider of

information is a natural person, the given name, surname, address

of the declared place of residence and actual address of the

provision of services, as well as the number in the register of

credit intermediaries, if the natural person is a credit

intermediary, shall be indicated;

31.2. the possible purposes for which the credit may be

used;

31.3. the types of security, including information regarding

the possibility of the security to be located in another Member

State of the European Economic Area;

31.4. the possible terms of operation of credit

agreements;

31.5. the types of available borrowing rates by indicating

whether this is fixed or variable or a combination of both,

adding a short description of characteristics of the fixed and

variable interest rates, including the impact on the consumer

related thereto;

31.6. if a loan in foreign currency is available - information

regarding the foreign currency or currencies, including an

explanation as to what is the impact of the credit expressed in a

foreign currency on the consumer;

31.7. the total amount of the credit in the form of a

representative example, the total charges of the credit for the

consumer, the total amount to be paid by the consumer, and the

annual percentage rate of charge;

31.8. the possible further costs which are not included in the

total charges of the credit for the consumer and which must be

paid in relation to the credit agreement;

31.9. different possibilities for repayment of the credit to

the creditor, including the amount, number and frequency of the

possible regular payments to be made by the consumer;

31.10. in the relevant case a clear and concise reference that

conformity with the provisions of the credit agreement does not

guarantee repayment of the total amount of the credit issued

according to the credit agreement;

31.11. information regarding the conditions for early

repayment of the credit;

31.12. information regarding the necessity to perform an

evaluation of the immovable property, regarding the party

responsible for the performance of the evaluation, as well as

regarding whether it causes any costs for the consumer;

31.13. a reference regarding the obligation to conclude an

ancillary service contract relating to the credit agreement, if

the conclusion of such a contract is compulsory in order to

obtain the credit or to obtain it on the terms and conditions

marketed. Where applicable, an explanation shall be appended that

ancillary services may be acquired from a service provider other

than the creditor;

31.14. a general warning regarding the consequences, if the

liabilities arising from the credit agreement are not

fulfilled.

32. Before the consumer has undertaken the liabilities of the

credit credit agreement or offer, the creditor, credit

intermediary or representative of the credit intermediary shall,

on the basis of the information provided by the consumer

regarding his or her needs, financial situation and preferences,

without undue delay and free of charge, provide personalised

information to the consumer which is necessary in order to

compare different offers, assess their impact, and take a

conscious, informed decision on whether to conclude

agreement.

33. The personalised information referred to in Paragraph 32

of this Regulation shall be provided in conformity with the

European Standardised Information Sheet included in Annex 2 to

this Regulation on paper or using another durable medium. All the

information referred to is required to be equally visible. The

creditor, credit intermediary or representative of the credit

intermediary has fulfilled the information requirements in

conformity with this Paragraph and the requirements specified in

the regulations regarding distance contracts for the provision of

financial services for informing the consumer prior to the

conclusion of a distance contract for financial services, if he

has provided information to the consumer in conformity with the

abovementioned Sheet prior to concluding the credit

agreement.

34. Other information other than indicated in the Sheet

included in Annex 2 to this Regulation and which is provided by

the creditor, credit intermediary or representative of the credit

intermediary to the consumer, shall be included in a separate

document to be appended to the Sheet included in Annex 2 to this

Regulation.

35. If an offer is given to a consumer which is binding to the

creditor, it shall be provided on paper or using another durable

medium by appending the Sheet referred to in Annex 2 to this

Regulation, if it has not already been previously issued to the

consumer or the characteristics of the offer are different from

the information indicated in the Sheet issued previously.

36. If an offer is given to a consumer which is binding to the

creditor, the creditor, credit intermediary or representative of

the credit intermediary shall offer to issue a copy of the draft

credit agreement to the consumer free of charge.

37. If voice telephony is used as means of communication with

the consumer in accordance with the regulations regarding

distance contract for the provision of financial services, at

least the information referred to in Part 1, Paragraphs 3, 4, 5,

and 6 of Annex 2 to this Regulation shall be included in the

description of financial services to be provided in accordance

with the abovementioned regulations.

38. In order to enable the consumer to assess whether the

proposed credit agreement and ancillary services proposed are

adapted to his needs and to his financial situation, the

creditor, credit intermediary or representative of the credit

intermediary shall, upon request of the consumer, explain to the

consumer the information to be provided to the consumer in

accordance with this Chapter and Annex 2, as well as the

essential characteristics of the services proposed and the

consequences which may be caused for the consumer by use of the

services, including inform regarding the consequences arising

from the non-performance or inadequate performance of the

agreement.

39. If the credit agreement is offered together with ancillary

services, information shall be provided to the consumer as to

whether it is possible to terminate the operation of each

additional ancillary service contract individually, as well as

the impact of such termination on the consumer.

40. The credit intermediary or representative of the credit

intermediary shall provide the information referred to in Chapter

XIV of this Regulation to the consumer.

VI. Information On Overdraft

Credit, Credit Agreements Concluded by Member Benefit

Organisations and Credit Agreements for the Fulfilment of Initial

Credit Agreement Obligations to be Provided to a Consumer Prior

to the Conclusion of a Credit Agreement

41. Before a consumer is bound by a credit agreement or offer

in relation to overdraft credits to be repaid on demand or within

three months, as well as to the credit agreements referred to in

Paragraph 44 of this Regulation, the creditor or credit

intermediary, in good time, on the basis of the credit terms and

conditions offered by the creditor and, if applicable, the

preferences expressed and information supplied by the consumer,

if any, shall provide the consumer with the information needed to

compare different offers in order to take an informed decision on

whether to conclude a credit agreement.

42. The following shall be indicated in the information

referred to in Paragraph 41 of this Regulation:

42.1. the type of credit;

42.2. the name, registration number, legal address and address

of the actual provision of services, if different from the legal

address, of the creditor and, if a credit intermediary is

involved, the credit intermediary. If the credit intermediary

involved is a natural person, the given name, surname, declared

place of residence and address of the actual provision of

services shall be indicated;

42.3. the total amount of the credit;

42.4. the duration of the credit agreement;

42.5. the borrowing rate, the conditions governing the

application of that rate, any index rate applicable to the

initial borrowing rate, the charges applicable from the time the

credit agreement is concluded and the conditions under which

those charges may be changed, if the change in charges is

permitted;

42.6. the annual percentage rate of charge illustrated by

means of a representative example indicating all the assumptions

used for calculation of the abovementioned rate;

42.7. the procedure for terminating the credit agreement;

42.8. for overdraft credit agreements to be repaid on demand

or within three months, an indication shall be included that the

consumer may be requested to repay the amount of the credit in

full at any time, if this condition is applicable to the specific

credit;

42.9. the interest rate in the case of late payments and the

procedures for the application thereof, as well as any penalties

or other compensation for the non-compliance with the contractual

obligations (if any);

42.10. the consumer's rights to be informed immediately and

free of charge, in compliance with the Consumer Rights Protection

Law, of the use of a database for the purposes of assessing the

ability of the consumer to repay the credit;

42.11. for overdraft credit agreements to be repaid on demand

or within three months, information shall be indicated regarding

the charges applicable from the time the agreement is concluded

and the conditions by which these charges may be changed (if the

change in charges is permitted); and

42.12. the period of time during which the creditor is bound

by the information provided prior to entering into contract (if

such is specified).

43. The information referred to in Paragraph 42 of this

Regulation shall be provided in compliance with the Standard

European Consumer Credit Information form included in Annex 4 to

this Regulation on paper or using another durable medium. All the

abovementioned information is required to be equally visible. The

creditor has fulfilled the information requirements in compliance

with this Paragraph and the requirements specified in the

regulations on distance contracts for the provision of financial

services for informing the consumer prior to the conclusion of a

distance contract for financial services, if he has provided

information to the consumer in compliance with the form referred

to.

44. For credit agreements which have been concluded by member

benefit organisations, as well as credit agreements in which the

creditor and the consumer have agreed on the procedure for

repayment, if the consumer has not honoured the initial credit

agreement obligations, and such procedure would prevent potential

court proceedings for not honouring the obligations specified in

the consumer credit agreement, and, therefore, less favourable

terms than those specified in the initial consumer credit

agreement would not apply to the consumer, the following

information shall be indicated in addition to the information

referred to in Paragraph 42 of this Regulation:

44.1. the amount, number and frequency of payments to be made

by the consumer, as well as the procedure by which payments will

be allocated to different outstanding balances charged at

different borrowing rates for the purpose of reimbursement (if

such procedure is specified);

44.2. the right of early repayment of the credit and

information concerning the creditor's right to compensation and

the procedures by which that compensation shall be determined in

accordance with Paragraph 101 of this Regulation (if any).

45. If voice telephony has been used as a means of

communication between the creditor and the consumer and the

consumer is requesting immediate access to overdraft credit, at

least the information referred to in Sub-paragraphs 42.3, 42.5,

42.6, and 42.8 of this Regulation shall be included in the

characteristics of the financial services. The creditor shall

also provide this information regarding overdraft credit to be

repaid within one month. In addition to the characteristics of

the credit agreements referred to in Paragraph 44 of this

Regulation, the duration of the credit agreement shall also be

included.

46. If an agreement has been concluded upon request of the

consumer, using a distance means of communication which does not

enable information to be provided in accordance with Paragraphs

41, 42, 43, and 44 of this Regulation, the creditor shall provide

the consumer with information regarding the credit agreement in

accordance with Chapter VIII of this Regulation, insofar as it is

applicable, immediately after the conclusion of the credit

agreement.

47. Upon request of the consumer, the creditor shall issue a

draft copy of the credit agreement containing information in

accordance with Chapter VIII of this Regulation, insofar as it is

applicable. This provision shall not be applied if the creditor

at the time of the request does not wish to conclude a credit

agreement with the consumer.

VII. Requirements to be Brought

Forward for Advisory Services

48. Advice may be provided by creditors, credit intermediaries

or representatives of credit intermediaries only. The creditor,

credit intermediary or representative of the credit intermediary

shall, prior to providing advice or accordingly prior to entering

into a contract regarding provision of advisory service,

explicitly inform the consumer as to whether the consumer is

being provided or may be provided advice, as well as shall

provide the following information free of charge - as additional

information to the pre-contractual information provided for in

Chapter IV, V or VI of this Regulation - on paper or using

another durable medium:

48.1. whether the advice will be based on considering only the

product range of the creditor, credit intermediary or

representative of the credit intermediary or a wide range of

products from across the market so that the consumer can

understand the basis on which the advice is made;

48.2. where applicable, the fee to be paid by the consumer for

the advisory service or, where the amount cannot be ascertained

at the time of provision of the information, the method used for

its calculation.

49. Creditors, credit intermediaries or representatives of the

credit intermediary shall obtain the necessary information

regarding the consumer's personal situation and financial

standing, his preferences and objectives so as to enable the

recommendation of suitable credit agreements. Such an assessment

shall be based on information that is up to date at that moment

in time and shall take into account reasonable assumptions as to

risks to the consumer's situation during the term of operation of

the proposed credit agreement.

50. Creditors, credit intermediaries which are tied to one

creditor only, one group of companies of the creditor or several

creditors or their groups of companies which do not represent the

largest part of the credit service market (hereinafter - the tied

credit intermediaries) or representatives of the tied credit

intermediaries shall consider a sufficiently large number of

credit agreements available in their range of credit services and

recommend a suitable credit agreement or several suitable credit

agreements for the consumer's needs, financial standing and

personal situation.

51. Credit intermediaries or representatives credit

intermediaries which are not deemed to be the tied credit

intermediaries within the meaning of Paragraph 50 of this

Regulation, shall consider a sufficiently large number of credit

agreements available on the market and recommend a suitable

credit agreement or several suitable credit agreements available

on the market for the consumer's needs, financial standing and

personal situation.

52. Creditors, credit intermediaries or representatives of

credit intermediaries shall act in the best interests of the

consumer by informing themselves about the consumer's needs and

circumstances and recommending suitable credit agreements, and

shall give the consumer a record on paper or on another durable

medium of the recommendation provided.

53. The creditor, credit intermediary or representative of the

credit intermediary shall warn the consumer if the credit

agreement may cause special risk to the consumer due to the

financial standing of the consumer.

54. The use of the term "independent advising" and

"independent advice" or similar terms shall be permitted if the

creditor, credit intermediary or representative of the credit

intermediary considers a sufficiently large number of credit

agreements available on the market and is not remunerated for

those advisory services by one or more creditors.

55. The provisions of this Chapter shall not affect the duty

of creditors, credit intermediaries or representatives of credit

intermediaries to provide explanations to the consumer regarding

the information to be provided to the consumer in accordance with

the requirements of this Regulation.

VIII. Information to be Included

in the Credit Agreement

56. The following shall be clearly and concisely indicated in

the credit agreement (if it has not been specified otherwise for

particular types of credit agreement):

56.1. the type of credit;

56.2. the name, registration number, legal address of the

creditor and the credit intermediary, if a credit intermediary is

involved, the consumer and the address thereof. If the credit

intermediary involved is a natural person, the given name,

surname, declared place of residence and address of the actual

provision of services shall be indicated;

56.3. the duration of the credit agreement;

56.4. the total amount of the credit and the conditions

governing the drawdown;

56.5. the good or service and the price thereof, if, in

accordance with the credit agreement, it is intended to grant a

loan in the form of deferred payment for the specific good or

service or it is anticipated to conclude the linked credit

agreement;

56.6. the borrowing rate, the conditions governing the

application of the borrowing rate, and the index rate, if such is

applied to the initial borrowing rate, as well as the periods,

conditions and procedures for changing the borrowing rate. If

different borrowing rates are applied in different circumstances,

the information referred to in respect of all the rates

applicable shall be indicated in the credit agreement;

56.7. the annual percentage rate of charge and total amount

payable by consumer, which is calculated at the time of

concluding the credit agreement, mentioning the assumptions used

in the calculation of the annual percentage rate of charge;

56.8. the amount, number and frequency of payments to be made

by the consumer, as well as the procedures by which payments will

be allocated to different outstanding balances charged at

different borrowing rates for the purpose of reimbursement (if

such procedure is specified);

56.9. the consumer's right to receive, on request and free of

charge, at any time throughout the duration of the credit

agreement, a statement of account with a credit repayment table

on paper or using other durable medium, on which the parties have

agreed in the credit agreement if the repayment of the total

credit amount is specified in the credit agreement within a

specified time period. The payments to be made by the consumer,

the periods and conditions relating to the payment thereof shall

be indicated in the credit repayment table. The table shall

contain a breakdown of each repayment showing the repayment of

the total credit amount, the interest calculated on the basis of

the borrowing rate and any additional costs if such are provided

for in the credit agreement. Where the interest rate is not fixed

or the additional costs may be changed under the credit

agreement, the credit repayment table shall indicate, clearly and

concisely, that the data contained in the table will remain valid

only until such time as the borrowing rate or the additional

costs are changed in accordance with the credit agreement;

56.10. a statement showing the periods and conditions for the

payment of the interest and of any associated recurrent and

non-recurrent charges, if charges and interest are to be paid

without capital amortisation in accordance with the credit

agreement;

56.11. if the credit agreement provides for the mandatory

opening of an account, the charges for maintaining one or several

accounts recording both payment transactions and drawdowns,

indicating the charges for using a means of payment for both

payment transactions and drawdowns, any other charges deriving

from the credit agreement and the conditions under which those

charges may be changed;

56.12. the interest rate applicable in the case of delayed

payments at the time of the conclusion of the credit agreement

and the procedures for the application thereof and the penalty or

other compensation for non-compliance or inadequate compliance of

contractual obligations (if such is provided for);

56.13. information on the consequences of missing

payments;

56.14. the duty to pay notarial costs (if such are

anticipated);

56.15. the sureties and insurance (if such is necessary);

56.16. information on the right of withdrawal from the credit

agreement, the period during which the right of withdrawal may be

exercised and other conditions governing the exercise of the

rights referred to, including information concerning the

obligation of the consumer to repay the amount of credit received

to the creditor and the interest in accordance with the Consumer

Rights Protection Law, as well as the amount of interest payable

per day;

56.17. information concerning the consumer claims specified in

Section 31 of the Consumer Rights Protection Law related to

customer credit for the purchase of goods or services, as well as

the conditions for the exercise of these rights;

56.18. information concerning the right of early repayment of

the credit, the procedure for early repayment, as well as

information concerning the creditor's right to compensation and

the procedures by which that compensation will be determined in

accordance with Paragraph 101 of this Regulation (where

applicable);

56.19. the procedure to be followed in exercising the right of

termination of the credit agreement;

56.20. information concerning the mechanism for examining

out-of-court disputes for the consumer and the opportunities for

having access thereto (if such is anticipated);

56.21. other contractual terms and conditions (where

applicable); and

56.22. the name and address of the supervisory authority.

57. In the case referred to in Sub-paragraph 56.9 of this

Regulation the creditor shall make available to the consumer,

free of charge and at any time throughout the duration of the

credit agreement, a statement of account in the form of a credit

repayment table.

58. In the case of a credit agreement under which payments

made by the consumer do not give rise to an immediate

corresponding amortisation of the total amount of credit, but are

used to constitute capital during periods and under conditions

laid down in the credit agreement or in an ancillary agreement,

the creditor shall include a clear and concise statement in the

information referred to in Paragraph 56 of this Regulation that

such credit agreements do not provide for a guarantee of

repayment of the total amount of credit drawn down under the

credit agreement, unless such a guarantee is given.

59. The following shall be clearly and concisely indicated in

the agreement for overdraft credit to be repaid on request or

within three months:

59.1. the type of credit;

59.2. the name, registration number, legal address of the

creditor and the involved credit intermediary, the consumer and

the address thereof. If the credit intermediary involved is a

natural person, the given name, surname, declared place of

residence and address of the actual provision of services shall

be indicated;

59.3. the duration of the credit agreement;

59.4. the total amount of the credit and the conditions

governing the drawdown;

59.5. the borrowing rate, the conditions governing the

application of the borrowing rate, and the index rate, if such is

applied to the initial borrowing rate, as well as the periods,

conditions and procedures for changing the borrowing rate. If

different borrowing rates are applied to the overdraft credit,

the abovementioned information shall be indicated in the credit

agreement in respect of all the applicable rates;

59.6. the annual percentage rate of charge and the total cost

of the credit to the consumer, calculated at the time the credit

agreement is concluded. All assumptions used for the calculation

of the abovementioned rate in accordance with the definition

"total costs of the credit to a consumer" laid down in Section 1

of the Consumer Rights Protection Law and Sub-paragraph 2.2 and

Paragraph 6 of this Regulation shall be indicated in the credit

agreement;

59.7. an indication that the consumer may at any time, upon

request of the creditor, be requested to repay the credit amount

in full; and

59.8. information concerning the charges applicable from the

time of concluding the overdraft credit agreement and the

conditions under which these charges may be changed.

60. In a credit agreement which provides that the consumer is

required to repay the credit in a time period not exceeding three

months and in accordance with which negligible additional

payments are requested for the use of credit in comparison with

the total amount of the credit and the duration of the credit

agreement, the information referred to in Sub-paragraphs 56.1,

56.2, 56.3, 56.4, 56.5, 56.6, 56.8, 56.11, 56.12, 56.13, 56.14,

56.15, 56.18, 56.19, 56.20, 56.21, and 56.22 of this Regulation,

as well as the total amount payable by the consumer shall be

indicated.

61. In the credit agreement the repayment of which is secured

by an immovable property or the purpose of the credit is to

acquire or retain a right in immovable property, the information

referred to in Sub-paragraphs 56.1, 56.2, 56.3, 56.4, 56.5, 56.6,

56.7, 56.8, 56.9, 56.10, 56.11, 56.12, 56.13, 56.14, 56.15,

56.16, 56.18, 56.19, 56.20, 56.21, and 56.22 of this Regulation

shall be indicated.

62. In the credit agreement upon the conclusion of which the

consumer is requested to deposit an item as security in the

creditor's safe-keeping and the liability of the consumer is

strictly limited to that pledged item, the information referred

to in Sub-paragraphs 56.1, 56.2, 56.3, 56.4, 56.6, 56.8, 56.12,

56.13, 56.14, 56.15, 56.18, 56.19, 56.20, 56.21, and 56.22 of

this Regulation, as well as the total amount to be paid by the

consumer, a detailed description of the pledge which would ensure

the identification thereof, an evaluation of the pledge and the

liability of the creditor for retaining the pledge throughout the

duration of the credit agreement shall be indicated by indicating

the insurance company with which the civil liability of the

creditor is insured for losses caused to the pledge transferred

to the creditor for safe-keeping in accordance with Paragraph 81

of this Regulation as a result of his or her action or failure to

act.

63. In a credit agreement concluded by a member benefit

organisation, at least the information referred to in

Sub-paragraphs 56.1, 56.2, 56.3, 56.4, 56.5, 56.6, 56.7, 56.8,

and 56.12 of this Regulation shall be indicated.

64. In a credit agreement in which the creditor and the

consumer have agreed on the procedures for repayment, if the

consumer has not honoured the initial credit agreement

obligations, and such procedures would prevent potential court

proceedings for failure to honour the obligations specified in

the consumer credit agreement, and, therefore, less favourable

terms than those specified in the initial consumer credit

agreement would not apply to the consumer, at least the

information referred to in Sub-paragraphs 56.1, 56.2, 56.3, 56.4,

56.5, 56.6, 56.7, 56.8, 56.9, 56.12, and 56.18 of this Regulation

shall be included. However, if the conditions referred to in

Paragraph 59 of this Regulation apply to the credit agreement,

only Paragraph 59 of this Regulation shall be applicable.

65. If an agreement has been concluded between the consumer

and the creditor regarding the opening of a settlement account

with the option that the consumer has the right to use funds

exceeding the balance of funds in the settlement account of the

consumer or the granted overdraft facility, information regarding

the borrowing rate, the conditions governing the application of

this rate, the index rate applicable to the initial borrowing

rate, the charges applicable from the time of concluding the

credit agreement and the conditions under which these charges may

be changed, if a change in charges is permitted, shall also be

included in the agreement regarding the opening of a settlement

account. The requirements referred to in Paragraphs 56, 57, 58,

and 59 of this Regulation shall not apply to such agreements.

66. All amendments and supplements to a credit agreement shall

be made in writing (on paper or using another durable medium),

and they shall be signed on both sides, except amendments arising

from the conditions for changing the borrowing rate specified in

the credit agreement, if the creditor has informed the consumer

of the changes referred to in compliance with Paragraph 90, 91 or

94 of this Regulation.

67. A consumer has a duty to pay only the payments provided

for in the credit agreement.

68. The information shown in the credit agreement is required

to be equally visible.

IX. Requirements Applicable to

Consumer Credit for Pledging Movable Property

69. It shall be permitted to provide a credit service in which

it is required to deposit a movable property as security in the

creditor's safe-keeping and where the liability of the consumer

is strictly limited to that pledged movable property (hereinafter

- the pledge) only in a building or part of the building. It is

prohibited to organise consumer credit for a pledge in short-term

use, temporary and seasonal buildings.

70. The creditor shall ensure the safe-keeping of the pledge

deposited thereto for safe-keeping in the storage facility

provided for this purpose, ensuring such storage conditions that

prevent unauthorised persons from accessing the pledges.

71. The storage facility shall be located in the same building

as the customer service area, and it shall be isolated from other

premises and customer service areas. The entrance to the storage

facility shall not be in the access area of the customers.

72. Large-sized pledges, physically impossible to store in the

storage facility referred to in Paragraph 71 of this Regulation,

may be stored in another specially equipped space, which may be

located in a separate building, or in a car park, ensuring such

storage conditions that prevent unauthorised persons from

accessing the pledges. The creditor shall ensure twenty-four hour

guarding and video surveillance of the storage area of the

large-sized pledge, in accordance with Paragraph 73 of this

Regulation.

73. The creditor shall conclude one or more contracts with

security guard merchants which operate in accordance with the

Security Guard Activities Law, in order to ensure that the

following conditions are fulfilled in the premises of the credit

service provision:

73.1. the building or part of a building referred to in

Paragraph 69 of this Regulation, which is used in order to

provide the service of consumer credit for pledging movable

property, including the storage facility, is equipped with an

automatic security and fire alarm system, which is connected to

the central security control panel, using not less than two

different alarm signal transmission channels;

73.2. continuous internal and external video surveillance of

the storage facility, customer service area and entrance takes

place, using closed circuit television cameras and performing a

video recording in real time mode (the resolution of the video

recording shall incorporate not less than 520 TV channels, 25

frames per second, the video recording of each camera having an

initial data flow not lower than 184.25 Mb/s, and using

H.264/AVC/MPEG-4 Part 10 standard video data compression),

ensuring secure safe-keeping of the recording equipment and video

recordings in order to prevent illegal disposal thereof. Video

recordings shall be stored for at least one month counting from

the day of making the video recording;

73.3. credit service provision, pledge acceptance and issuance

shall take place in an area with video surveillance;

73.4. informative signs shall be placed by the entrance to the

service provision premises, alerting the consumer to the video

surveillance; and

73.5. the premises of the credit service provision and storage

facility shall be equipped with an emergency alarm button which

is connected to the central security control panel of the

security guard merchant.

74. It is prohibited to accept as pledge an item:

74.1. for which the creditor cannot ensure the special storage

conditions required thereby (special temperature mode, lighting,

humidity mode and other conditions), due to which the item may be

damaged;

74.2. which has been removed from circulation in the private

sector;

74.3. the turnover of which is restricted; or

74.4. the identification number of which, allocated by the

manufacturer, has been destroyed or damaged or otherwise

encumbered or the identification of the item has been made

impossible.

75. The creditor has duty to verify the identity of the person

from whom the pledge is being accepted.

76. The creditor must ensure the accounting of the pledges

deposited to the safe-keeping thereof by complying with the

following conditions:

76.1. the recording shall be performed in electronic form,

using an appropriate accounting programme which ensures:

76.1.1. the secure storage of data;

76.1.2. the retaining of the history of any operation

performed with data (entry, amendment, review, deletion);

76.1.3. automatic generation of the entry number;

76.1.4. the storage of any appended files, for example, photo

images and scanned documents together with the registration

entry;

76.1.5. user identification;

76.1.6. performance of a printout of the entries made;

76.2. if the electronic accounting is performed locally (data

is not sent online and is stored on a remote server, which

ensures the copying of data back-up and remote access to

information of the register), written accounting shall also be

performed, using a registration journal bound together, stamped,

with numbered pages.

77. The following data shall be registered in the accounting

system referred to in Paragraph 76 of this Regulation:

77.1. the given name, surname and data of a personal

identification document (personal identity number, number of the

personal identification document) of the consumer;

77.2. the number of the credit agreement concluded and the

date of conclusion;

77.3. the total amount of the credit;

77.4. the pledge evaluation amount;

77.5. a description of the pledge, observing the following

conditions:

77.5.1. if precious metals and the products thereof are

deposited to the creditor for safe-keeping, the type, proof,

weight in grams (with 0.1 g accuracy), a description of the item

which ensures the identification thereof, shall be indicated in

the accounting by appending a photographic image of the item;

77.5.2. if precious stones and products containing them are

deposited to the creditor for safe-keeping, their type and, if

possible, weight in carats, as well as a description of the item

which ensures the identification thereof, shall be indicated in

the accounting by appending a photographic image of the item;

77.5.3. in the accounting of other types of pledges the name

of the item, the identification number assigned by the

manufacturer, the make, model, a description of the item which

ensures the identification thereof, shall be indicated, appending

a photographic image of the item;

77.6. the payments made by the consumer in accordance with the

credit agreement; and

77.7. the date of the redemption of the pledge or the date of

the sale of the pledge, if the pledge is sold to extinguish the

debt obligations of the consumer.

78. The data referred to in Sub-paragraphs 77.1, 77.2, 77.3,

77.4, and 77.5 of this Regulation shall be registered in the

accounting system immediately after the conclusion of the credit

agreement. The data referred to in Sub-paragraph 77.6 of this

Regulation shall be registered in the accounting system

immediately after the receipt of the payment made by the

consumer. The data referred to in Sub-paragraph 77.7 of this

Regulation shall be registered in the accounting system

immediately after the redemption of the pledge or the sale of the

pledge.

79. The pledge accounting data referred to in Paragraph 77 of

this Regulation shall be kept for not less than one year from the

day of the redemption of the pledge or not less than five years

from the day of the sale of the pledge.

80. The creditor shall formulate an identification system for

the pledges deposited to the safe-keeping thereof which would

ensure unambiguous identification of pledges in conformity with

the entry made in the accounting system referred to in Paragraph

76 of this Regulation and the concluded credit agreement.

81. The creditor has a duty to insure his civil liability for

the losses caused to the pledge deposited to the creditor for

safe-keeping as a result of the action or failure to act thereof.

The limit of the abovementioned civil liability insurance for the

insurance period shall not be lower than the total amount of the

loan issued by the creditor.

X. Additional Requirements for

Credit Agreements the Repayment of Which is Secured by an

Immovable Property or the Purpose of the Credit is to Acquire or

Retain a Right in Immovable Property

82. Offering or selling of the credit agreement in one package

with other distinct financial services where the credit agreement

is not made available to the consumer separately, is prohibited.

The abovementioned prohibition shall not apply to offering of the

following financial services to the consumer or his or her family

member (parents, grandparents, children, grandchildren, siblings,

spouse):

82.1. opening or maintaining a payment or a savings account,

where the only purpose of such an account is to accumulate

capital to repay the credit, to service the credit, to pool

resources to obtain the credit, or to provide additional security

for the creditor in the event of default;

82.2. purchasing or keeping an investment product or a private

pension product, where such service which primarily offers the

investor an income in retirement serves also to provide

additional security for the creditor in the event of default or

to accumulate capital to repay the credit, to service the credit

or to pool resources to obtain the credit;

82.3. concluding a separate credit agreement in conjunction

with a shared equity credit agreement to obtain the credit.

Within the meaning of this Regulation, a shared equity credit

agreement means the credit agreement where the capital to be

repaid is based on a contractually set percentage of the value of

the immovable property at the time of the capital repayment or

repayments;

82.4. purchasing a relevant insurance policy related to the

credit agreement where the creditor accepts the insurance policy

from other service providers where such policy has a level of

guarantee equivalent to the one the creditor has proposed.

83. The prohibition referred to in Paragraph 82 of this

Regulation shall not be applicable to cases when the creditor is

able to prove to the supervisory authority that the services

offered in a package provide a clear benefit to the consumer in

comparison to similar services by taking into account the

availability and market price of such services.

84. A credit agreement may be offered or sold in a package

with other distinct financial services where the credit agreement

is made available to the consumer separately. In such case the

credit agreement may be offered to the consumer based on the

provisions or conditions other than if it is acquired together

with ancillary services.

85. Where according to the credit agreement such loan has been

granted which was a foreign currency loan at the time of

concluding the credit agreement, and where during the term of

operation of the credit agreement the remainder from the total

amounts payable to the consumer or the amount of regular payments

differs by more than 20 % from the case where the currency

exchange rate between the currency of the credit agreement and

the currency of the Member State applicable at the time of

concluding the credit agreement would be applicable, the creditor

shall provide the consumer with the right to converting the loan

in alternative currency in accordance with the agreement reached

in the credit agreement or to use another solution provided for

in the credit agreement for limiting the exchange rate risk.

86. The alternative currency referred to in Paragraph 85 of

this Regulation in accordance with the agreement reached in the

credit agreement may be one or both of the following

currencies:

86.1. the currency in which the consumer primarily receives

income or holds assets from which the credit is to be repaid, as

indicated at the time the most recent creditworthiness assessment

in relation to the credit agreement was made;

86.2. the currency of the Member State of the European

Economic Area in which the consumer either was resident at the

time the credit agreement was concluded or is currently

resident.

87. The exchange rate at which the conversion referred to in

Paragraph 85 of this Regulation is carried out is the market

exchange rate applicable on the day of application for

conversion, unless it is otherwise provided for in the credit

agreement.

88. Where a consumer has been granted a loan which at the time

of concluding the credit agreement is a foreign currency loan,

the creditor shall, during the term of operation of the credit

agreement, warn the consumer on a regular basis (however not less

than once a year) on paper or on another durable medium at least

where the value of the total amount to be paid by the consumer

which remains outstanding or of the regular instalments varies by

more than 20 % from what it would be if the exchange rate between

the currency of the credit agreement and the currency of the

Member State applicable at the time of the conclusion of the

credit agreement were applied. The warning shall inform the

consumer of a rise in the total amount to be paid by the

consumer, in the relevant case set out therein the right to

convert to an alternative currency and the conditions for doing

so in accordance with the agreement reached in the credit

agreement or the right to use another solution provided for in

the credit agreement for limiting the exchange rate risk.

89. Information regarding the measures to be applied in

accordance with Paragraphs 85, 86, 87, and 88 of this Regulation

shall be provided to the consumer free of charge in the European

Standardised Information Sheet included in Annex 2 to this

Regulation and in the credit agreement. Where there is no

provision in the credit agreement to limit the exchange rate risk

to which the consumer is exposed to if a fluctuation in the

exchange rate does not exceed 20 %, the European Standardised

Information Sheet shall include an illustrative example of the

impact of a 20 % fluctuation in the exchange rate.

90. Where the credit agreement is a variable rate credit, the

index ratesLibor, Euribor or others) used to

calculate the borrowing rate shall be clear, accessible,

objective and verifiable by the parties to the credit agreement