|

Republic of Latvia

Cabinet

Order No. 129

Adopted 9 February 2016

|

On the Energy Development

Guidelines for 2016-2020

1. To support the Energy Development Guidelines for 2016-2020

(hereinafter - the Guidelines).

2. To determine the Ministry of Economics as the institution

responsible for the implementation of the Guidelines, and the

Ministry of Finance, the Ministry of the Interior, the Ministry

of Education and Science, the Ministry of Transport, the Ministry

of Agriculture, and the Ministry of Environmental Protection and

Regional Development as the co-responsible institutions.

3. For the institutions involved in the implementation of the

Guidelines to submit a report to the Ministry of Economics on the

results of the implementation of the activities provided for in

the Guidelines until 1 December 2017 and 1 December 2020.

4. For the Minister for Economics to submit the informative

report to the Cabinet:

4.1. until 1 October 2018 - on the implementation of the

Guidelines in 2016-2017;

4.2. until 1 October 2021 - on the implementation of the

Guidelines in 2018-2020.

5. For the institutions involved in the implementation of the

Guidelines to ensure the implementation of the measures included

in the Guidelines in 2016 within the limit of the funds granted

from the State budget. To examine the issue of granting

additional funds from the State budget for 2017 and subsequent

years during the preparation process of the draft law On the

State Budget for 2017 and the draft law On the Medium-term

Framework of the Budget for 2017, 2018, 2019, together with

applications of the new policy initiatives of all ministries and

other central State institutions, considering the financial

possibilities of the State budget.

6. To repeal the Cabinet Order No. 571 of 1 August 2006, On

the Energy Development Guidelines for 2007-2016 (Latvijas

Vēstnesis, 2006, No. 122).

Prime Minister Laimdota Straujuma

Minister for Economics Dana

Reizniece-Ozola

(Cabinet Order No. 129

9 February 2016)

ENERGY DEVELOPMENT

GUIDELINES

for 2016-2020

(Informative Part)

Ministry of Economics

Riga, 2016

CONTENTS

Introduction

1. Targets of the Energy Policy

1.1. Targets of the EU Energy Policy

1.2. Long-term Targets of the Energy Policy of Latvia

1.3. Policy Results to be Achieved and Their Performance

Indicators

2. Core Principles of the Energy Policy

3. General Characterisation and Development Trends of the

Energy Sector

3.1. Primary Energy Resources

3.1.1. Renewable Energy Resources

3.1.2. Fossil Energy Resources

3.1.3. Other Energy Resources

3.2. Establishment of the Internal Energy Market

3.2.1. Electricity Market

3.2.2. Natural Gas Market

3.3. Energy Infrastructure

3.3.1. Electricity Infrastructure

3.3.2. Natural Gas Infrastructure

3.3.3. Transport Charging/Fuelling Infrastructure

3.4. Heating Supply

3.5. Renewable Energy Sources

3.6. Energy Efficiency

3.7. Management of Crisis Situations

3.8. Innovative Solutions in the Energy Sector

3.9. Strengthening of International and Regional

Cooperation

4. SWOT Analysis

4.1. Electricity

4.2. Natural Gas

4.3. Heating Supply

4.4. Energy Efficiency

4.5. Most Significant Problems to be Solved

5. Planning of Subsequent Actions

6. Impact of the Policy on the State and Local Government

Budget

List of Abbreviations Used

|

ACER

|

Agency for the Cooperation of Energy

Regulators |

| RES |

Renewable Energy Sources |

| USA |

United States of America |

| BEMIP |

Baltic Energy Market Interconnection Plan

(regional cooperation and coordination with the countries

around the Baltic Sea) |

| BRELL |

Treaty entered into by and between the

transmission system operators of Belarus, Russia, Estonia,

Latvia and Lithuania |

| CEF |

Connecting Europe Facility |

| CSB |

Central Statistical Bureau of the Republic

of Latvia |

| MoE |

Ministry of Economics |

| ERDF |

European Regional Development Fund |

| EU |

European Union |

| ESCO |

energy service company |

| ETS |

Emissions Trading System |

| EUROSTAT |

Statistical Office of the European

Communities |

| ETS |

Emissions Trading System |

| MoF |

Ministry of Finance |

| GIPL |

Gas Interconnector Poland-Lithuania |

| GDP |

Gross domestic product |

| IRENA |

International Renewable Energy Agency |

| PCI |

Projects of common interest |

| Cabinet |

Cabinet |

| NDP2020 |

National Development Plan 2014-2020 |

| NPS |

Power spot trading Nord Pool Spot |

| NGO |

Non-governmental organisations |

| OECD |

Organisation for Economic Co-operation and

Development |

| MP |

Mandatory procurement |

| MPC |

Mandatory procurement component |

| UGSF |

Underground gas storage facility |

| TSO |

Transmission system operator |

| SAIDI |

Duration of electricity supply interruptions

per 1 client a year |

| SAIFI |

Frequency of electricity supply

interruptions per 1 client a year |

| LNG |

Liquefied natural gas |

| IEA |

International Energy Agency |

| GHG |

Greenhouse gases |

| SET |

Subsidised energy tax |

| PUC |

Public Utilities Commission |

| SWOT |

Strengths and weaknesses, opportunities and

threats |

| |

|

| Units of measurement: |

|

| GWh |

Gigawatt hour |

| ha |

Hectare |

| J |

Joule |

| kW |

Kilowatt |

| kWh |

Kilowatt hour |

| kV |

Kilovolt |

| Mtoe |

Millions of tons of oil equivalent |

| MWel |

Electric power in megawatts |

| MW |

Megawatt |

| MWh |

Megawatt-hour |

| m2 |

Square metre |

| m3 |

Cubic metre |

| PJ |

Peta-joule |

| TWh |

Terawatt-hour |

| V |

Volt |

| W |

Watt |

Introduction

The Energy Development Guidelines for 2016-2020 (hereinafter -

the Guidelines) are a policy planning document which prescribes

the core principles, targets, and action directions of the

Latvian government policy in the energy sector for the time

period from 2016 to 2020. Their objective is to define a strategy

for a competitive, safe, and sustainable energy policy,

concurrently outlining the long-term trends for the development

of the sector in all fields of the energy sector.

On 28 May 2013, the Cabinet (hereinafter - the Cabinet) noted

the informative report "Long-term Strategy of the Energy Sector

of Latvia 2030 - Competitive Energy Sector for the

Society"1 (hereinafter - the Energy Strategy 2030),

assigning the Ministry of Economics (hereinafter - the MoE) to

develop the energy policy guidelines for the period up to 2020

and to submit them to the Cabinet for examination.

During development of the Energy Policy Guidelines the

informative report "On the financing of the Energy Policy within

the Period from 2014 to 2020"2 was prepared which was

examined at the Cabinet meeting of 20 May 2014.

The Guidelines were developed based on the competence of the

MoE laid down in Sub-paragraph 5.3 of the Cabinet Regulation No.

271 of 23 March 2010, By-laws of the Ministry of Economics, to

develop and implement policy in specific sectors of national

economy, including the energy sector, and based on the laws and

regulations governing the drawing up of development planning

documents which lay down the information to be included in the

content of the Guidelines and the structure of the document, as

well as the outlined tasks and the measures to be implemented for

their fulfilment.

The Guidelines also provide detailed settings of the NDP2020

energy policy, as well as targets of the recommendation of the

Council of the European Union (hereinafter - the EU) for the 2014

National Reform Programme of Latvia (see Annex 2).

There are several other factors which justify the necessity

for the development of the Guidelines. In 2016, the applicable

Energy Development Guidelines for 2007-2016 have partially lost

their topicality, as well as several planning documents for the

period up to 2020 are in effect which also include energy issues.

During the period of operation of the Energy Guidelines for

2007-2016 new national development planning documents which are

higher in hierarchy have been adopted (Sustainable Development

Strategy of Latvia up to 2030, NDP2020), the situation in

strategic planning of the electricity sector of Latvia and Baltic

has changed, and the range of energy policy introduction

instruments has been reviewed.

On 23 October 2014, the draft Guidelines developed by the MoE

were handed over for public discussion and posted on the website

of the MoE

(https://em.gov.lv/lv/par_ministriju/sabiedribas_lidzdaliba/diskusijai_nodotie_dokumenti/),

fulfilling the obligation specified in Sub-paragraph 10.2 of the

Cabinet Regulation No. 970 of 25 August 2009, Procedures for

Public Participation in the Development Planning Process,

(hereinafter - Cabinet Regulation No. 970) to ensure public

access to the documents to be discussed throughout the period of

public discussion. Upon fulfilling that referred to in

Sub-paragraph 10.1 of Cabinet Regulation No. 970, the time period

for public discussion of the draft Guidelines during which public

representatives provided proposals was at least 30 days before

the announcement of the draft Guidelines in the meeting of State

Secretaries.

In addition to the public discussion on the website of the

MoE, a meeting for discussion of the draft Guidelines with

participation of the sectoral and public representatives was

organised at the MoE on 22 November 2014 and at the Energy

Sub-committee of the National Economy Council on 24 November.

Apart from the abovementioned meetings also several meetings with

representatives of individual sectors took place in order to

discuss the issues to be addressed in the draft Guidelines. The

proposals submitted by sectoral representatives prior and after

announcement of the draft Guidelines in the meeting of State

Secretaries were evaluated and the draft Guidelines were

updated.

During the preparation of the Guidelines, in accordance with

the procedures laid down in the law On Environmental Impact

Assessment, in order to assess the potential environmental impact

and to involve the public in discussing the document and

decision-making, as well as to draft proposals in order to

prevent or reduce the potential negative impact on human health

and environment, a strategic environmental impact assessment was

carried out.

1. Targets of

the Energy Policy

1.1. Targets of the EU Energy

Policy

In accordance with Article 4 of the Treaty on the Functioning

of the European Union, energy is one of the fields in which the

EU and Member States have a shared competence.

The EU must reach the following climate and energy policy

targets by 2020 which were brought forward in the European

Council of 8/9 March 20073:

- to achieve at least a 20 % reduction of GHG emissions by

2020 compared to 1990 level;

- to increase the share of renewable energies in energy

consumption up to 20 %;

- to increase energy efficiency by 20 %.

For the EU to achieve the target specified in the

Roadmap4 in 2050 for transition to a competitive

low-carbon economy - to reduce GHG emissions by 80-95 % and to

provide clarity to investors about the development of both

policies after 2020, the European Council of 23/24 October 2014

took a decision5 on climate and energy targets for

the time period from 2020 to 2030, and they are as

follows:

- to achieve at least a 40

% reduction of GHG emissions compared to 1990 level.

The EU Member States must jointly reach the abovementioned

target in a more cost-effective manner, providing that a

reduction in the following amounts is achieved by 2030 compared

to 2005:

- in the amount of 43 % in the sectors belonging to the

Emissions Trading System (hereinafter - the ETS), and

- in the amount of 30 % for non-ETS6 sectors.

The target of the ETS has been jointly specified for all EU

Member States - individual targets and freedom of choice for

their achievement (reduce emissions or acquire emission quotas)

has been specified for all participants, but the target for GHG

emissions of non-ETS sectors will be specified for each Member

State individually (at the national level with a binding target),

re-distributing the liabilities for reducing emissions;

- to increase the

share of renewable energies in the total energy consumption by at

least 27 %. This target is binding at the EU level which

means that Member States will have the right to determine the

national level targets themselves;

- to increase the

energy efficiency target by at least 27 % compared to the

estimates of future energy consumption. This target is indicative

at the EU level. A review clause of the target has been indicated

in the conclusions of the European Council, determining that

targets may be reviewed and increased up to 30 % until 2020;

- prevention of inadequate interconnections between the gas

and electricity networks of Member States, and also ensuring

synchronous operation of Member States in European networks as

foreseen in the European Energy Security Strategy will also

remain a priority after 2020. Therefore, by 2030 it is expected to achieve at

least the 15 % interconnection target. The 10 %

interconnection target which had to be achieved by 2005 was

already specified in the 2002 European Council, however, it still

has not been achieved in separate Member States.

The establishment of

the European Energy Union is one of the priorities of

Jean-Claude Juncker, President of the EC, who became the

President of the European Commission on 1 November 2014. It is

related to reforms in the energy policy in the EU, emphasising

the management of the energy policy. The reform has the following

objectives:

- solidarity and trust to improve safety of energy supply for

Member States through joint cooperation;

- coordination among Member States in the development of

national energy policy;

- joint investments for Member States by coordinating

investment programmes and their conditions;

- establishment of a functioning EU internal market providing

that Member States will gradually reduce the protection of

national markets from other Member States or will take decisions

for the benefit of particular companies;

- coordination of the EU Member States prior to negotiations

with the third countries.

The Energy Union is oriented towards diversification of energy

sources, reduction of energy dependence of the EU Member States,

the ability of the EU to change the direction and routes of flows

of energy resources in case of necessity, as well as to increase

the use of renewable energy sources (including local renewable

energy sources) in the Energy Union.

1.2. Long-term Targets of the Energy

Policy of Latvia

The energy policy of Latvia is directed towards ensuring

further development of the economy of Latvia, and also the

increase of its competitiveness in the region and the world, as

well as public welfare and environmental quality.

The main objective of the energy policy of Latvia is to

increase the competitiveness of national economy together with

the implementation of other sectoral policies by facilitating the

safety of supply, formation of energy resources and energy prices

specified by the free market and competition, sustainable

generation and consumption of energy with two targets of the

energy policy:

- improving the safety of energy supply which provides

for stable energy supply available to the consumers of energy by

reducing geopolitical risks, diversifying the sources and routes

of supply of energy resources, developing interconnections and

the infrastructure of the national internal energy supply,

introducing smart technologies in energy supply networks, forming

reserves of energy resources, and participating in the

improvement of the legal framework. Long term optimisation of the

costs of the safety of energy supply also requires regional

cooperation:

• further integration into the networks of the EU and

Scandinavian countries, achieving levelling of prices in the

region;

• diversification of energy supply by solving issues of both

electricity and gas infrastructure within the framework of the

internal energy market at the EU level;

- sustainable energy which ensures sustainability of

energy in economic, social, and environmental sense. This is

planned to be achieved by improving the energy efficiency,

introducing smart technologies, and promoting highly efficient

generation technology and technologies for the use of renewable

energy sources (hereinafter - the RES).

• In relation to the renewable energies, several

targets have been laid down in Latvia for the time period until

2020:

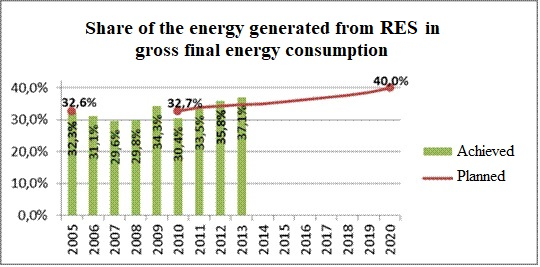

○ the share of the RES in gross final energy consumption in

2020 - 40 %, the target is binding, laid down in the RES

Directive 2009/28/EC7 and in the national reform

programme of Latvia "EU 2020";

○ the share of the RES in gross final energy consumption in

the transport sector in 2020 - 10 %, the target is binding, laid

down in the RES Directive 2009/28/EC and in the national reform

programme of Latvia "EU 2020";

• to reduce the GHG emissions per one unit of fuel or energy

supplied until 2020 by 6 %.

• In relation to energy efficiency, several targets

have been laid down in Latvia8 for the time period

until 2020:

○ savings of primary energy in 2020 - 0.670 Mtoe (28 PJ), the

target is not binding, laid down in the national reform programme

of Latvia "EU 2020";

○ mandatory national accumulated final energy savings until

2020 - 0.850 Mtoe, the target is binding, laid down in accordance

with the Energy Efficiency Directive 2012/27/EU9;

○ each year 3 % of the area of buildings of direct

administration are renovated (maximum forecast - in total 678 460

m2 renovated) - the target is binding, laid down in

the Energy Efficiency Directive 2012/27/EU;

○ to reduce the average consumption of thermal energy for

heating (with climate correction) by 50 % compared to the

consumption in 2009 (202 kWh/m2), the target of 150

kWh/m2 per year must be achieved by 2020. The target

is not binding, defined in the Energy Strategy for 2030.

○ reduction of energy intensity from the oil equivalent of

372.9 kg per EUR 1000 of the GDP in 2010 to the oil equivalent of

280 kg per EUR 1000 euro of the GDP in 2020.

Source: Directorate-General for Climate Action of the European

Commission

Figure 1. Non-ETS targets of the EU Member States for

202010

• At the EU level GHG emissions must be reduced by 20 %

until 2020 compared to the amount of emissions in 1990.

Therefore, Latvia11 has mandatory targets in the

environmental sector which also concern energy in the most direct

way:

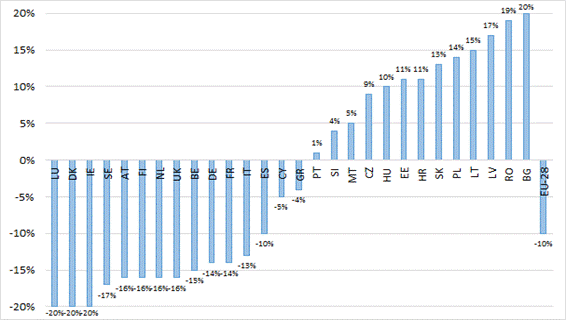

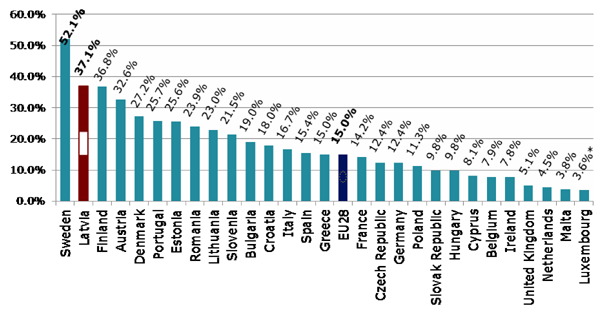

○ to restrict greenhouse gas emissions in non-ETS sectors in

such a way that the increase would not exceed 17 % compared to

2005 (see comparison with other EU Member States in Figure

1);

○ to restrict the total GHG emissions of the State so that

they would not exceed 12.16 Mt of CO2 equivalent in

2020.

1.3. Policy Results to be Achieved

and Their Performance Indicators

In order to evaluate the progress in achieving the targets,

the policy results to be achieved and their performance

indicators have been laid down, and they are both binding and

indicative at the level of the EU or Member States (see Table

1).

Table 1

Results of the Energy Policy of the

EU and Latvia and their Performance Indicators

|

Policy

result

(performance indicator)

|

EU-27/EU-28 |

Latvia |

| Target value |

Actual value |

Indicative intermediate value |

Target value |

| 2020 |

2030 |

Base value (year) |

2013 |

2017 |

2020 |

| |

Sustainable

energy |

| |

Action directions for

achieving the target: Diversification of primary energy

resources, increase of the share of RES |

|

1.1. |

Share of the energy

generated from RES in the final gross energy consumption

(%) |

20 |

27 |

34.3

(2009) |

37.1 |

37 |

40 |

|

1.2. |

Share of the energy

generated from RES in the final gross energy consumption in

transport (%) |

10 |

|

1.35

(2005) |

3.1 |

5 |

10 |

| |

Action directions for

achieving the target: 4. Efficient thermal energy market;

6. Improved energy efficiency |

|

1.3. |

Increase in energy

efficiency (%) |

20 |

27 |

|

|

|

|

|

1.4. |

Primary energy savings

(gross domestic energy consumption, Mtoe) |

|

|

0.144

(2012) |

0,160 |

n/a |

0.670 |

|

1.5. |

National mandatory

accumulated final energy savings, Mtoe (GWh;

PJ) |

|

|

1161

(2012) |

1896 |

3483 |

0.85 Mtoe (9897 GWh; 35.6

PJ) |

|

1.6. |

Each year 3 % of the area

of buildings of direct administration is renovated (in

total renovated, m2) |

|

|

|

|

|

678 460 m2 |

|

1.7. |

Specific consumption of

thermal energy in buildings(kWh/m2/year) |

|

|

250

(2012) |

230 |

160 |

150 |

|

1.8. |

Energy consumption for the

creation of domestic gross product (kg of oil equivalent

per 1000 euros of the GDP) |

280 |

<150 |

372.9 |

350 |

320 |

280 |

| |

Increasing the safety

of energy supply in the region |

| |

Action directions for

achieving the target Diversification of primary energy

resources, Creation of an efficient energy market, Efficient

energy infrastructure, Strengthening of international and

regional cooperation |

| |

|

|

|

|

|

|

|

|

2.1. |

Connections of the

infrastructure in the electricity market (capacity of

interconnections compared to the installed generating

capacity, %) |

10% |

15% |

|

4% 12 |

n/a |

10% |

|

2.2. |

Connections of the

infrastructure in the gas market

Integration in the

EU networks, possibilities to procure natural gas from

different sources (number of sources) |

|

|

1 |

1 |

≥

1 |

≥

1 |

|

2.3. |

Energy dependence -

net import of energy resources/gross domestic energy

consumption plus bunkering (%) |

n/a |

n/a |

41.6

(2010) |

42.4

(2014) |

43.2 |

44.1 |

2. Core

Principles of the Energy Policy

The future energy policy will be created on the basis of the

following core principles:

- integration of the EU climate and energy policy targets into

the national policy;

- regional cooperation with Estonia and Lithuania and other

countries around the Baltic Sea (Baltic Energy Market

Interconnection Plan (hereinafter - the BEMIP)) (see Sub-section

3.9) in order to ensure coordinated development and

implementation of the energy policy in the region;

- competitive energy price which is based on the principles of

operation of the market and respects interaction between

different sectors;

- safety of energy supply which is the basis for taking each

decision so that the provision of energy resources would be

sufficient for national economy, including households;

- improvement of safety and quality of energy supply as the

basis for restoring and developing the existing infrastructure

with the objective of promoting the competitiveness of national

economy;

- efficient use of resources, including cost effectiveness is

promoted at all stages of energy generation, transformation,

transportation, and use;

- equal conditions of competition for individual groups of

producers or suppliers;

- availability of energy to consumers with a comparatively low

level of income;

- availability of information regarding the measures that

ensure implementation of the energy policy;

- introduction of innovative solutions, including smart

technologies;

- being conscious of environmental protection and climate

change problems, sustainable policy oriented towards reduction of

GHG emissions;

- energy efficiency as one of the main policy instruments

which allows to reduce costs and, by reducing the energy

consumption, increases the safety level of energy supply;

- efficient use of renewable energy sources in all sectors,

including transport.

3. General

Characterisation and Development Trends of the Energy Sector

3.1. Primary Energy Resources

The dependence of Europe on imported energy resources keeps

increasing. According to the forecasts of the International

Energy Agency (hereinafter - the IEA) more than 80 % of the

consumed oil and gas will be imported in 2035. The global energy

consumption in 2035 could increase by more than a third where

China, India, and Middle Eastern countries will consume more than

60 % of the forecasted increase.

The price variations of electricity in the global market are

significantly affected by the prices of fossil energy. For

example, shale gas revolution in the United States of America

(hereinafter - the USA) ensures certain advantages to

energy-intensive industrial producers of the USA in comparison to

the EU producers. In 2012, the gas price for industrial producers

in the USA was four times lower than for the EU producers. Within

seven years (2005-2012) the industrial price index determined by

the IEA for the actual price of electricity increased by 37 % for

the European members states in the Organisation for Economic

Co-operation and Development (hereinafter - the OECD) (see Annex

1), while it decreased by 4 % in the USA. Shale gas revolution in

the USA also prompted more intense use of black coal in the EU,

because otherwise the competitiveness of the EU would decrease.

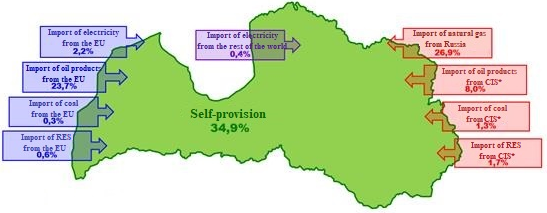

Latvia mostly uses imported energy resources. In 2013 local

energy resources ensured 34.9 % from the total consumption of

primary energy resources. Majority of them were RES - wood

biomass, hydro-resources, wind, biogas, biofuels, and local

energy resources - peat, waste. The remaining part or 65.1 % of

energy resources among which oil products and natural gas are the

most important were imported from different countries of the

Baltic region, EU, and the third countries, including from

Russia. Natural gas was supplied only from Russia, which

represented 26.9 % (50.27 PJ) (see Figure 2).

Source: The External Trade database of the Statistical Office

of the European Union (hereinafter - EUROSTAT) was used in

estimates.

* Commonwealth of Independent States

Figure 2. Flow of primary energy

sources in Latvia in 2013

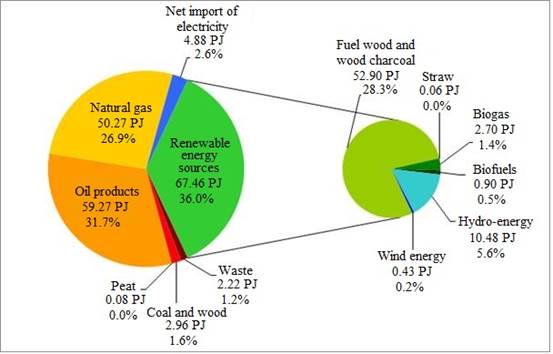

Renewable energy sources, oil products and natural gas prevail

in the structure of the primary energy resources of Latvia (see

Figure 3). Contrary to individual EU countries, the consumption

of black coal keeps decreasing in Latvia, and in 2013 it amounted

to only 121 thousand tonnes. Significant changes in the structure

of primary energy resources are not planned in the time period

until 2020.

Source: Central Statistical Bureau of the Republic of Latvia

(hereinafter - the CSB)

Figure 3. Structure of the

consumption of the primary energy resources of Latvia in 2013 (by

the types of energy resources), PJ and %

3.1.1. Renewable Energy Sources

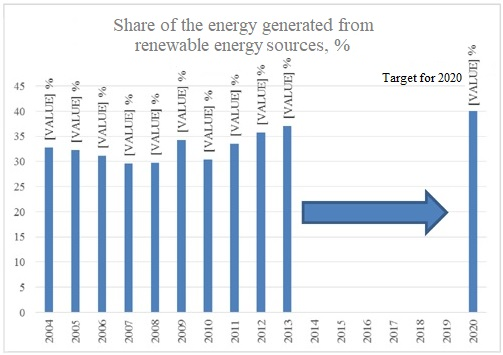

The actual share of RES in the total consumption of primary

energy resources keeps slowly rising (see Figure 4). It is

expected that by 2020 it will reach the target laid down in the

RES Directive 2009/28/EC - 40 %.

In Latvia, the most important RES are wood biomass and

hydro-energy. Wood biomass is the most important local fuel

which in Latvia is used for the centralised and local heating

supply, as well as in co-generation. In the last five years, the

total consumption of fuelwood has been constantly rising. 6477

m3 solid (45.65 PJ) of fuelwood were consumed in 2010,

6677 m3 solid (46.90 PJ) - in 2011, 7314 m3

solid (52.50 PJ) - in 2012, 7327 m3 solid (53.11 PJ) -

in 2013, and 7668 m3 solid (55.92 PJ) in 2014. Its

share in the balance sheet of the primary energy resources of

Latvia of 2014 amounted to 30 % of the total consumption of

primary energy resources. It is expected that the consumption of

biomass will continue to rise in the energy sector.

Source: EUROSTAT

Figure 4. Actual share of RES in the total consumption of

primary energy resources13

In terms of cost-effectiveness,

hydro-energy14 is characterised by the

comparatively lowest amount of capital investments per generated

quantity of energy. Latvia has suitable conditions for the use of

hydro-energy, and individual hydroelectric power plants in

combination with accumulation of energy in water reservoirs with

flexible generation possibilities from fossil or biogas energy

resources may be used also as base electric power plants.

Considering the development of modern and environment-friendly

technologies, the use of hydro-energy resources in all rivers

should be based only on nature-friendly methods related to

conservation of the environment. This principle should also be

applied to all operated hydroelectric power plants. For it to be

implemented, it is necessary to review the conditions and rates

for the application of the natural resources tax for all

hydroelectric power plants.

Theoretical hydro-energy resources of the medium and small

rivers of Latvia are 900 GWh of electricity per year, without

using River Venta, River Lielupe, and the middle and lower

sections of River Gauja. The hydro-energy resources of small

rivers that can be practically used are estimated to be within

the borders of 250-300 GWh of electricity per year. Hitherto only

70 GWh have been mastered, that is 23-28 % of the potential power

of the former water mills and former small HPPs. Taking into

account the legal framework currently in force15, it

is prohibited to build and restore hydroelectric power plants on

specific rivers and river sections. In relation to the other

rivers and river sections which are not included in the

abovementioned legal framework, it is necessary to receive the

documentation necessary for construction and to perform the

necessary environmental protection procedures to construct new

hydroelectric power plants.

The quantity of electricity output in Latvia depends on the

flow of River Daugava. Cascade on River Daugava - Riga HPP,

Ķegums HPP, and Pļaviņas HPP ensures on overage 40 % of the

electricity consumed in Latvia. In concern for efficient use of

water resources and environmentally safe economic activity,

hydro-aggregates of Rīga HPP on River Daugava are being gradually

restored. The main objective of reconstruction projects is to

replace the outdated hydraulic turbines in order to ensure safe,

efficient, continuous, and competitive operation of Rīga HPP on

River Daugava in the common energy supply system. As a result of

reconstruction the operational parameters of hydraulic turbines,

such as installed capacity and efficiency coefficients, will be

improved, thus increasing the output of electricity in a year. In

total twelve of the twenty three hydro-aggregates of Rīga HPP on

River Daugava were modernised in 2015. At the end of 2013 a

contract on the replacement of two hydro-aggregates in Pļaviņas

HPP was entered into, but at the beginning of 2014 - on the

reconstruction of three hydro-aggregates in Ķegums HPP. The

reconstruction process of all 11 hydro-aggregates that have not

been reconstructed by now is planned to be completed in 2022, and

it is estimated that the total restoration costs might exceed 200

million euros. In 2014, the total investments in the assets of

Rīga HPP on River Daugava were 20.4 million euros of which 9.9

million euros were invested in the programme for the restoration

of hydro-aggregates of Rīga HPP on River Daugava and 8.1 million

euros were invested in implementation of various projects for the

safety of hydroelectric structures.

In relation to the potential threats in the sector, floods in

the river Daugava near Pļaviņas HPP may endanger the

hydrostructure itself, as well as tear the sluices of Riga HPP

and Ķegums HPP. Consequently, damage would be caused throughout

the lower reaches of River Daugava up to the sea. Solutions for

reducing such threats should be evaluated after 2020.

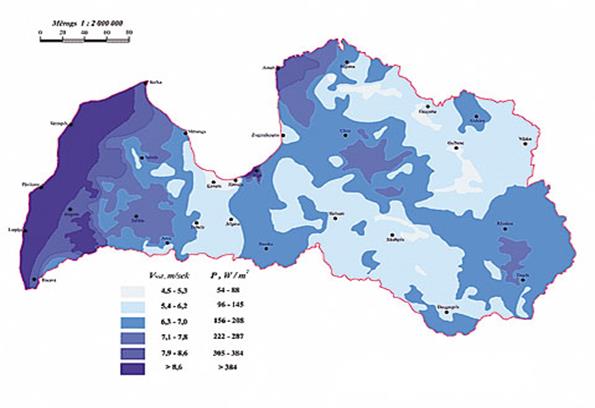

Whereas the division of wind energy resources in Latvia

is distinctly uneven (see Figure 5). Areas with different average

annual intervals of wind speed - from 2.8 m/s up to more than 5.4

m/s - are marked in the wind atlas of Latvia. Wind turbines start

to generate energy when the wind speed reaches 2.5 m/s.

Only those regions of the inner part of the territory of

Latvia where wind forms due to elevations are favourable to the

wind energy. The region of Latvia that has the highest wind speed

is the coast of the Baltic Sea and the western coast of the Gulf

of Riga, its northern part. Wind speed in these areas is from 5.1

to 5.8 m/s.

The wind potential in the inner part of the territory of

Latvia is up to 1.5 TWh (rationally obtainable electricity per

year). The forecast of transmission system operators (hereinafter

- the TSO) shows that the potential of wind energy in the deep

sea might reach 95 MWh. In 2014, the total installed electric

power in wind parks of Latvia was 69 MW (from them support within

the framework of the mandatory procurement (hereinafter - the MP)

was received by 53 wind parks with the total installed power 58.3

MW) and potentially two projects of wind parks with the total

electric power of 73 MW could be implemented.

Source: http://www.windenergy.lv

Figure 5. Wind atlas of Latvia

(average wind speed per year at 100 m height)

In Latvia solar energy as a resource for the generation

of electricity or thermal power has been used in a restricted

manner, as the high technological costs16 have

hitherto hindered full use of the existing resource. In 2013, the

renewable energies generated from sun amounted to less than one

per cent in the balance sheet of renewable energy sources of

Latvia, regardless of the fact that globally solar energy

technologies are considered one of the most significant energy

sources17 of the future. As the possibilities for the

storage of renewable energies are developing, significant

attention should be paid to the energy accumulation and stocking

solutions, as well as to the combination of solar energy

technologies with other renewable energy sources. Such approach

ensures sustainable energy supply and enables optimal use of the

available solar radiation potential.

The main geothermal resources of the territory of

Latvia are related to ground waters the temperature of which

exceeds 30 ºC, and to basement hot rock. The possibilities for

the use of geothermal waters are related to geothermal anomalies

of Eleja and Southern Latvia where temperature exceeds 57 ºC on

the basement in Eleja District and 50 ºC to 65 ºC in the coast

area of the Baltic Sea.

From 1993 to 1996 Latvia and Lithuania implemented a project

under management of a Danish undertaking Petroleum Geology

Investigators within the framework of which an assessment of

the potential of geothermal energy in Latvia was carried out. In

Devonian and Cambrian layers it was estimated to amount to 65 000

PJ, equating to 1.6 billion toe. Based on the calculations made

within the research, if hot waters would be extracted in the

territory of Latvia, the total capacity of thermal plants could

be starting from 175 MW18.

The use of geothermal energy is a perspective direction in

Latvia as the use of geothermal energy in heating technologies of

high efficiency allows to reduce the CO2 emissions,

allowing to partially refrain from the use of fossil fuel and

increase the independence from imported fuel. However, currently

one of the most substantial restrictions for the use of

geothermal energy in Latvia is the relatively large investments

that are necessary for the introduction of new technological

solutions in Latvia.

3.1.2. Fossil Energy Resources

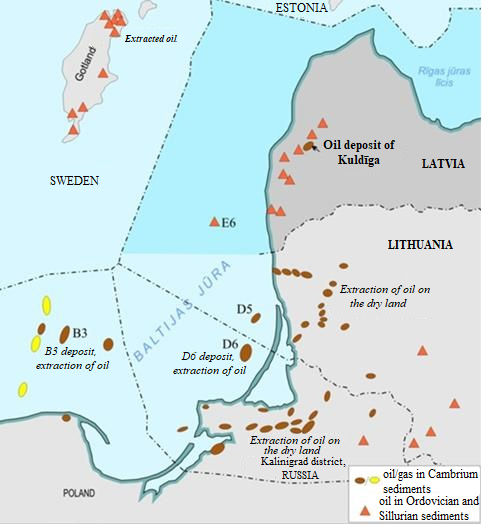

Latvia has a potential for the extraction of hydrocarbons (see

Figure 6). In total approximately 35 hydrocarbon deposits,

including one oil deposit (Kuldīga) has been discovered in Latvia

both on dry land and also in internal maritime waters,

territorial sea and exclusive economic zone of the Republic of

Latvia. Moreover, oil manifestations (signs) in rock pores or

cracks were observed in oil search and exploration drills.

Experimental extraction of hydrocarbons is taking place in once

licence field on dry land. At the same time significant changes

in the energy balance sheet of Latvia are not expected to be made

until 2020.

The southern part of the shelf of Latvia with the lowest

degree of geological risk, i.e., the possibilities of discovering

the foreseeable oil deposits, is the most perspective. Commercial

oil deposits could have formed here in large- and medium-sized

local rises. Several objects of significance from the point of

view of searching for oil are located in the dispute zone of the

Latvia-Lithuania border and, regardless of the interest, are not

available for exploration.

The other group of perspective oil objects is the objects

identified in the central shelf and the dry land next to it. Oil

manifestations and small oil deposits were found in many of them,

and also the oil deposit of Kuldīga which is the only such

deposit in Latvia was discovered.

At the end of 2015, several licences for the use of

subterranean depths issued by the Ministry of Economics were in

effect for the search, exploration, and extraction of

hydrocarbons both in the Baltic Sea (E6, E5, E23 structures) - in

internal maritime waters, territorial sea and exclusive economic

zone of the Republic of Latvia, and in the territory and on the

dry land. The undertaking Odin Energi Latvia SIA has a

licence for the use of subterranean depths for the search,

exploration, and extraction of hydrocarbons in the

sea19. In turn, for the exploration and extraction of

hydrocarbons on the dry land10 in the territory of the

Republic of Latvia:

• in Dunalka rural territory of Liepāja district and in Durbe

municipality the licence has been issued to the undertaking

GotOil Resources Limited, Loon Energy, Alvils

Bušenieks;

• in Nīca rural territory of Liepāja district the licence has

been issued to the undertaking Baltic Oil Corporation

PS;

• in Gudenieki rural territory of Kuldīga district the licence

has been issued to the undertaking Baltic Oil Management

SIA.

Source: Latvian Environment, Geology and Meteorology

Centre

Figure 6. Hydrocarbon deposits and

extraction of oil in the Baltic oil province

Natural gas has a significant place in the structure of

primary energy resources of Latvia, in 2013 it amounted to 26.9 %

or 50.27 PJ of the total consumption of primary energy resources,

but in 2014 - 24.4 % or 45.39 PJ.

In 2013, the total consumption of natural gas in Latvia was

1461 mill. m3 which is 3.1 % less than in 2012. The

majority of natural gas - 1007 mill. m3 or 68.9 % was

used in the transformation sector, including 877 mill.

m3 were consumed for the generation of electricity and

thermal energy in co-generation, and 130 mill. m3 -

for the generation of thermal energy in boiler-houses. In 2013,

124 mill. m3of natural gas or 8.5 % of the total

consumption of natural gas of Latvia was used in the household

sector, 174 mill. m3 (11.9 %) - in manufacturing, and

156 mill. m3 (10.7 %) - in other sectors. In 2014, the

consumption of natural gas decreased to 1313 mill.

m3.

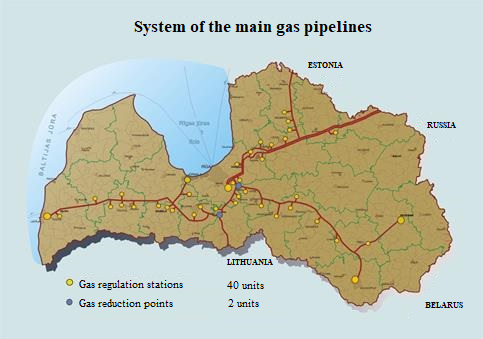

The main supply route of natural gas to consumers of Latvia is

the main networks of gas pipelines which branch off

Yamal-European gas pipe in Tver district (Russia), to Saint

Petersburg, Pskov, and then to Estonia, Latvia. The main networks

of natural gas of the Baltic States are well developed, and their

ability of providing stable supply is increased by the Inčukalns

underground gas storage facility (hereinafter - the UGSF) the

capacity of which is 2.3 bill. m3 of active gas.

Inčukalns UGSF is the only functioning storage facility in the

Baltic States, and it ensures the stability of regional gas

supply. In summer season when the consumption of natural gas in

the region is lower than during the cold season, natural gas is

pumped into the storage facility for it to be supplied to

consumers in Latvia, Estonia, north-western region of Russia, and

(in smaller amounts) Lithuania during the heating season.

Inčukalns UGSF gives an opportunity to provide natural gas to

consumers of Latvia, and it is not affected by short-term changes

in demand for natural gas in other countries.

At the beginning of 2015, the liquefied natural gas terminal

in Klaipėda (Lithuania) was accepted into operation, thus there

is a possibility to purchase LNG transported by ships and,

therefore, to improve the situation in the field of the safety of

gas supply even more. Moreover, with completing the

Klaipėda-Kuršėnai pipeline, additional volumes of gas may be

supplied to Latvia, enabling that a significant part of the daily

consumption of Latvia of 12.5 million cubic metres comes from an

alternative source.

Terminals for ensuring transit of oil products by sea

routes in Latvia are well developed (Riga, Ventspils),

significantly expanding the diversity and competition of supply.

Supply channels of oil products are sufficiently diversified as

the oil products are supplied from both Eastern and Western

markets. International retail oil companies that operate in

Latvia may procure oil and oil products from different regions of

the world. Bringing in of motor gasoline and diesel fuel for

retail and wholesale needs in Latvia is possible from at least 10

oil processing undertakings within the radius of 1000-1500 km.

The oil product pipeline from Samara in Russia and Novopolotsk in

Belarus allows transportation of diesel fuel with the possibility

of supplying it in Ilūkste and Ventspils.

Evaluation by product categories in 2014 compared to 2013

shows - the sales volume has increased for diesel fuel (by 7 %),

car gas (by 13 %), fuel gas (by 9 %). In turn, the sales volume

has decreased for gasoline (by 3 %), petrol (by 32 %), fuel oil

(by 57 %)9.

3.1.3. Other Energy Resources

The remaining part in the structure of primary energy

resources of Latvia is formed by net import of electricity, as

well as peat, coal, coke, and waste.

Extraction of peat provides certain potential for

ensuring energy independence. Extraction of energy peat from

already prepared peat deposits, for the harvesting of which there

are licences in effect, may be commenced in the area of

approximately 4000 ha, extracting at least 700 thous. t of energy

peat per year20. More than 300 boilers in which peat

can be incinerated were operating in Latvia in 2015.

Approximately 462 thous. t of peat per year may be used for the

generation of thermal energy. At the same time, by using peat as

a heating fuel, it is important that the environmental quality

does not deteriorate, particularly it is not permissible in more

densely populated areas and, mainly, in Riga. Concurrently, it is

important that the use of peat does not endanger achievement of

the GHG emission reduction targets.

A small number of coal boiler facilities is still remaining in

Latvia, mainly in private sector, part of them in Riga.

Use of waste for the generation of energy currently is not

widely developed in Latvia. Primarily, this issue must be

addressed within the framework of the waste management policy.

Here such preconditions as the preparation of waste for

regeneration, as well as economic efficiency from the aspect of

waste processing are of significance. If new waste sorting

facilities are constructed, then, for example, such household

waste as textile, wood, cardboard, polymer admixtures or the so

called alternate fuel (RDF) may be used for the generation of

energy.

3.2. Establishment of the Internal

Energy Market

Establishment of an integrated internal energy market of

Europe that functions efficiently ensures, in the long term,

higher flexibility of the system, competition among undertakings,

thus promoting the development of services and competitive

prices, as well as strengthens transparency of the market and

improves energy safety.

The third energy package determines that it is necessary to

strengthen and deepen the cooperation of the TSOs of the EU

Member States which would guarantee the efficiency of control of

transmission systems and transparent approach to the electricity

and natural gas transmission infrastructure on the national

borders of countries. The third energy package establishes an

institutional framework for the development of network codes and

guidelines with the purpose of coordinating, when necessary,

technical, operational and market regulations governing

electricity and gas networks.

In the field of electricity in 2013, the EC presented an

initiative to develop a package of EU documents, determining the

network codes of the EU level which until this moment were laid

down only in the regulations of Member States or electricity

transmission systems operators of the European network (ENTSO-E).

The network codes in the sector of European electricity

transmission will cover three areas - network connection, network

operation, and transboundary electricity market. Altogether 10

network codes will be developed in these three areas (see Table

2). Concurrently, the development of regulation of more technical

level - network codes in electricity and natural gas sectors - is

taking place.

Table 2

Network Codes in Electric

Energy

| 1.

Requirement for network connections |

- for electricity producers |

| - for consumers of electricity |

| - for high-voltage direct current systems

and modules of an electricity park |

| 2.

Operation of the network |

- operational safety |

| - planning and schedule of operation |

| - regulation of the network frequency and

reserves |

| - emergencies and restoration of

operation |

| 3.

Single electricity market |

- guidelines for assigning capacity and

overload control |

| - assigning of future capacity |

| - balancing of electricity |

In turn, in the natural gas sector gas regulations regarding

overload control procedures, assigning of capacity, balancing and

cooperation ability, and data exchange have been adopted in the

time period until 2015. The following documents are to be

developed in 2016:

- regulations regarding coordinated structures of transmission

tariffs;

- regulations regarding a market-oriented approach of EU scale

to distribution of the newly-built gas transmission capacity;

- regulations in relation to the oncoming CEN standard

regarding the quality of high calority gas.

Network codes will promote the efficiency of control of the

transmission systems, uniform conditions for linking the regional

markets, ensuring the use of electricity and natural gas

transmission infrastructure between the borders of the EU Member

States for the single EU energy market.

3.2.1. Electricity Market

Consumption of Electricity

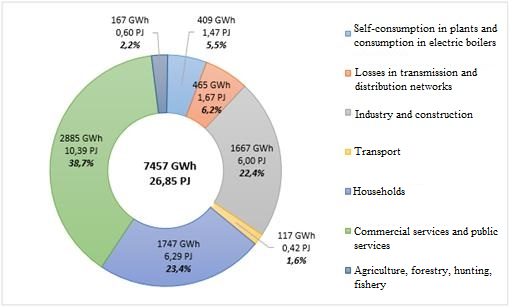

Gross consumption of electricity of Latvia was 7564 GWh in

2013 which is by 3.8 % less than in 2012. In 2014 gross

consumption of electricity was 7457 GWh which is by 19 % less

than in 2013. Three dominating consumption sectors should be

highlighted in the gross electricity consumption structure of

2014 - commercial services and public services (38.7 %),

household sector (23.4 %), and industry and construction (22.4 %)

(see Figure 7).

Industry and construction is the second largest final consumer

of electricity in Latvia. The largest energy consumers in the

manufacturing industry are the manufacturing sector of wood

products (except for manufacturing of furniture), the

manufacturing sector of metals, the manufacturing sector of food

products and beverages, as well as the manufacturing sector of

non-metallic mineral products. Further rise in prices of energy

resources may affect several sectors of significance to the

economy, namely, sector of commercial and public services,

processing industry (including all types of wood processing), as

well as manufacturing of food, and construction. The largest

undertaking of metallurgical industry in Latvia Liepājas

metalurgs AS, whose consumption of electricity has decreased

significantly in 2014, has a significant impact on consumption of

electricity.

Source: CSB

Figure 7. Structure of gross electricity consumption in

Latvia in 2014, GWh, PJ, %21

Generation of Electricity

From the total gross electricity consumption of 7457 GWh of

2014 Latvenergo AS generated 64.2 % in its plants (Rīga 1

and 2 thermal power plants, cascade power plants of Rīga HPP on

River Daugava, Aiviekste HPP, Ainaži wind power plant, Liepāja

generation units), procured 17.9 % from the small electricity

producers, as well as 17.9 % was formed by the net import of

electricity. Rīga 1 and 2 thermal power plants are the only power

plants of base capacities in Latvia with the installed capacity

above 100 MW which can ensure continuous generation of

electricity and heat both in co-generation and condensation mode

with the maximum summary annual load up to 7500 h. The price of

natural gas is one of the most significant cost factors which

affect the operation of Rīga 1 and 2 thermal power plants.

Short-term reaching of the maximum price at Nord Pool Spot

(hereinafter - the NPS) in the trading district of Latvia is less

motivating for the operation of Rīga 2 thermal power plant in

condensation mode, however, it allows for the operation of the

plant in co-generation mode - taking into account the low heat

load of the Rīga city during the summer season because

inexpedient use of the producer thermal energy reduces the

operation efficiency of the plants and, accordingly, increases

the costs per MWh generated. Limited loading of Rīga 2 thermal

power plant in co-generation mode in the summer season is

possible, if the electricity price in NPS trading district of

Latvia on 24 hour basis exceeds 45 EUR/MWh. Concurrently, it

should be noted that, as the oil prices are decreasing, the

competitiveness of natural gas technologies is also increasing -

at relatively low prices of natural gas thermal power plants

could implement a significant increase in domestic electricity

output which, in turn, would cause increase in consumption of

natural gas, activating the natural gas market.

In Latvia, the largest part of electricity is generated in

three power plants of the HPP cascade on River Daugava - Ķegums,

Pļaviņas and Rīga HPP the total installed capacity of which in

2013 was 1559.5 MW. In 2013, 2852 GWh of electricity were

generated in these plants, forming 46 % of the total gross

electricity amount generated in Latvia. The full installed

capacity of HPPs can only be used in spring during the flood or

high water period which lasts approximately two months. The

highest amount of electricity output is usually in April. In

individual cases, short periods of high water are also observed

in winter. On an annual basis, power plants of the HPP cascade on

River Daugava are able to ensure 200-250 MW in base mode. Plants

of the HPP cascade on River Daugava also serve as the capacities

for balancing of the electricity system and covering the peak

(maximum) loads. Electricity outputs of the high water period

allow the HPP cascade on River Daugava to successfully compete

with the Baltic and Finnish NPS in the electricity market. In the

time period until 2020, construction of new HPPs of higher

capacity on River Daugava is not intended.

In the future, the dispersed generation of electricity might

have a larger role, particularly it might have the potential in

such places where services of the system are not available.

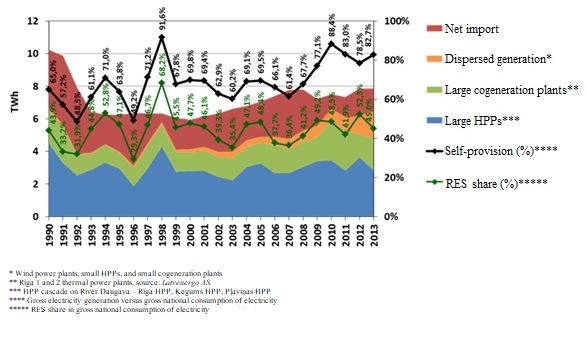

Self-sufficiency in electricity in Latvia by years varies (see

Figure 8); it amounted to 61 % in 2013 accordingly (88 % in

2014). In turn, the annual evaluation report of TSOs on 2015, by

evaluating the forecast of balance sheets of electricity and

electrical power according to a conservative

scenario22, indicates that the deficit of capacities

might increase from 60 MW in 2015 to 160 MW in 2020 which, in

turn, forms 96 % from the self-provision in 2015 and 89 % - in

2020. Approximately 1/5 part of the total gross electricity

consumption of Latvia is formed by net import of electricity

(17.9 % in 2013). Electricity is mainly imported when the water

level is insufficient for the generation of hydro-electric power,

as well as when it is not necessary to operate thermal power

plants in co-generation mode, mostly during the summer. By

ensuring sufficient interconnections in the EU global market,

self-provision is of smaller significance for safe energy

supply.

Source: CSB

Figure 8. Electricity supply

structure of Latvia

Retail Trade of Electricity

In order to develop cross-border trade, and also to stimulate

competition in the Baltic electricity market, NPS trading

districts of electricity exchange platform were opened in the

Baltic. The trading district of Latvia commenced operation on 3

June 2013, whereas Lithuania joined the NPS electricity exchange

in June 2012, and Estonia - in 2010.

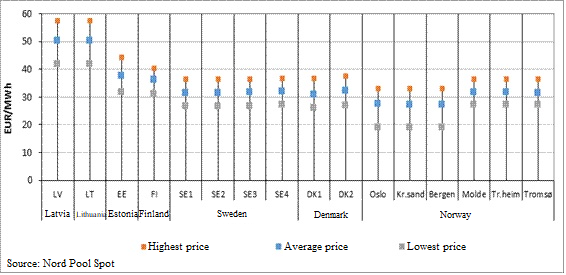

Source: NPS

Figure 9. Electricity prices in the

NSP exchange in 2014, EUR/MWH

Distinct price variations can be observed by comparing trading

districts of Latvia-Lithuania with trading district of

Estonia-Finland (see Figure 9). The basis for the formation of

price variations is insufficient capacity of power transmission

in the cross-section of Estonia-Latvia, and insufficiency of

market competitive generation in Latvia and Lithuania due to

comparatively high variable costs of electricity generation.

Prices of Latvia and Lithuania as regions of electricity deficit

are the same because the transmission capacity between both

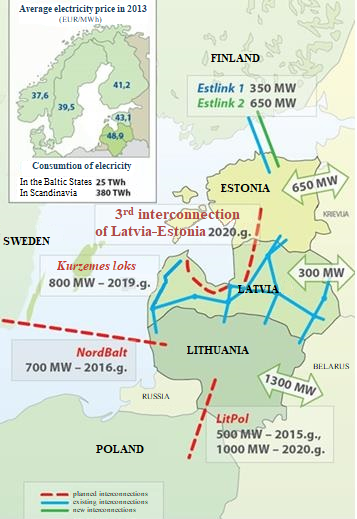

countries is sufficient. After switching on of the

NordBalt (interconnection of Sweden-Lithuania, flow

capacity 700 MW) cable at the end of 2015, levelling of prices is

anticipated in different trading districts of the region.

In 2014, operation of contracts of the Nasdaq OMX

Commodities exchange of financial instruments was commenced

in Latvia. The financial instruments market organised by the

Nasdaq OMX Commodities exchange has been operating in the

Nordic countries for ten years already. Until establishment of

the third Estonia-Latvia interconnection in 2020, limited

liquidity can be anticipated in the financial instruments market

of Nasdaq OMX Commodities in these countries, however, the

risk of price instability might reduce.

Retail Trade of Electricity

The electricity price in the conditions of a free market is

most efficiently determined in the long term. Therefore, there

are no more regulated electricity tariffs in an open electricity

market, however, the system services and the mandatory

procurement component are being regulated. Consumers of

electricity may choose the electricity trading offer which is the

most appropriate for their consumption of electricity.

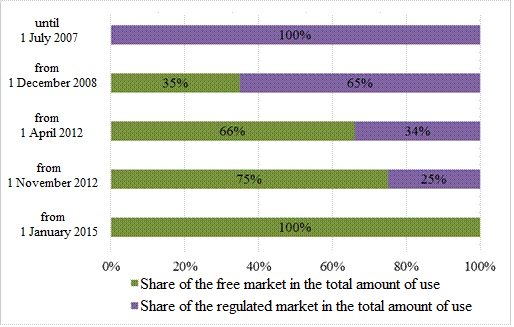

In Latvia, opening of the electricity market began on 1 July

2007. The different stages of opening the electricity market are

presented in Figure 10:

Source: Ministry of Economics

Figure 10. Division of the

electricity market according to stages

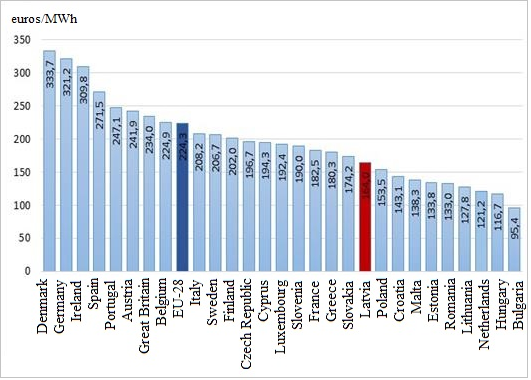

In accordance with the Eurostat data, the electricity price

(including all taxes and duties) for households (with the annual

consumption of 1000-2500 kWh) in Latvia in the first half of 2015

was the tenth lowest in the EU - 164 euros/MWh (see Figure 11).

Accordingly, in Estonia - 133.8 euros/MWh and in Lithuania -

127.8 euros/MWh.

Source: Eurostat

Figure 11. Electricity price

(including all taxes and duties) for households (with the annual

consumption 1000-2500 kWh) in the first half of 2015,

euros/MWh

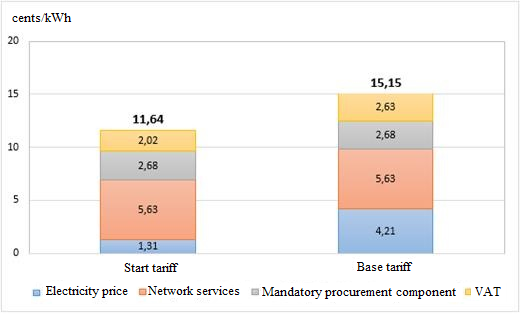

The total price of electricity is formed from the electricity

price, services of the transmission and distribution network, the

mandatory procurement component (hereinafter - the MPC), the

trade service, and the value added tax (VAT 21 %). After

liberalisation of the electricity market in 2015, the prices of

network services approved by the Public Utilities Commission

(hereinafter - the PUC) are in effect - 5.63 cents/kWh and the

MPC which currently is specified 2.68 cents/kWh and is partially

financed from the State budget funds. Therefore, only the

wholesale price of electricity is variable, varying depending on

the market situation. In 2014, the average wholesale price in the

price zone of Latvia was 50.12 cents/kWh which exceeded the

wholesale price of electricity included in both the start tariff

and the base tariff (see Figure 12).

Source: Ministry of Economics

Figure 12. Electricity tariff

structure for household electricity users (in effect from 1 April

2011 to 31 December 2014)

On 1 January 2015, the electricity market was opened also to

households as it is provided for by the amendments to the

Electricity Market Law of 20 March 2014. Concurrently with

opening the electricity market to households, approximately 847

300 household consumers joined the market, forming approximately

90 % of the total number of users. The electricity price is not

subsidised for all households anymore. The reduced electricity

price is provided for the vulnerable groups of inhabitants - poor

or low-income families (persons), families with a disabled child,

persons with the first group disability, and large families (the

difference of the electricity price is subsidised).

A poor or low-income family (person), as well as a family with

a disabled child and a person with the first group disability is

provided with 100 kilowatt hours of electricity for the

subsidised price of 0.0131 euros per kilowatt hour in each

accounting period (calendar month) and a large family - with 300

kilowatt hours of electricity for the price of 0.0131 euros per

kilowatt hour in each accounting period (calendar month). In such

case, the total electricity price (including the electricity

price, trading services, mandatory procurement component, value

added tax, and network services) is equivalent to the previous

start tariff - 11.64 cents per kilowatt hour. In turn, for the

amount of electricity which exceeds the abovementioned 100

kilowatt hours for a poor or low-income family (person), as well

as family with a disabled child and a person with first group

disability, and 300 kilowatt hours for a large family in the

accounting period, the protected consumer pays the price offered

by the electricity trader and selected by the protected consumer

or the specified universal service price. The obligation of the

service provider of a protected consumer in 2015 was fulfilled by

the Latvenergo AS, however, it will be selected according

to the procedures of a competition in accordance with the

requirements laid down in the Electricity Market Law and the

Public Procurement Law. Henceforth, the operation of this

solution should be evaluated, improving it in case of necessity

(including evaluating the possibilities of providing assistance

to less protected social groups also for the provision of other

essential services).

3.2.2. Natural Gas Market

At large the European Union still depends, to a great extent,

on the natural gas supplies of the third countries. The natural

gas supply system of Latvia is not directly connected to the

systems of other EU Member States, except for Lithuania and

Estonia. However, since Klaipėda LNG terminal is operating, there

is a possibility to receive natural gas physically not only from

Russia, but also from other countries.

Consumption of Natural Gas

The structure of natural gas consumption of Latvia is very

much seasonal by nature (see Figure 13). The heat loads of the

centralised heating supply system increase significantly in the

winter.

Source: CSB

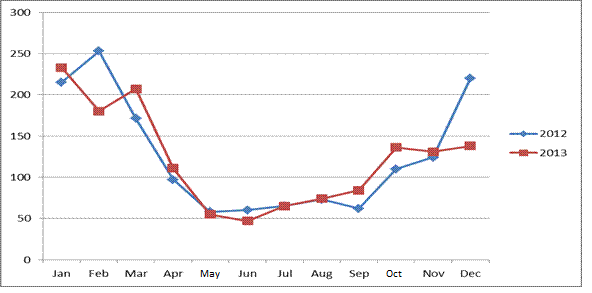

Figure 13. Fluctuations of the

natural gas consumption in 2012-2013 by months, mill.

m3

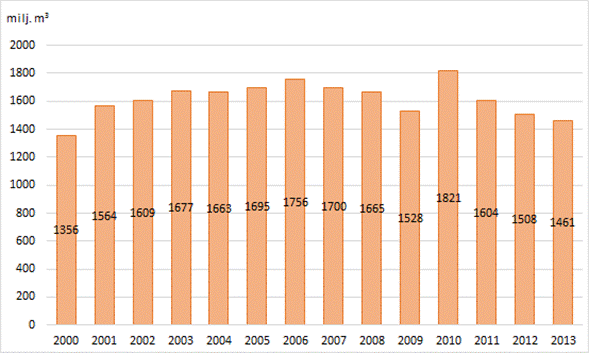

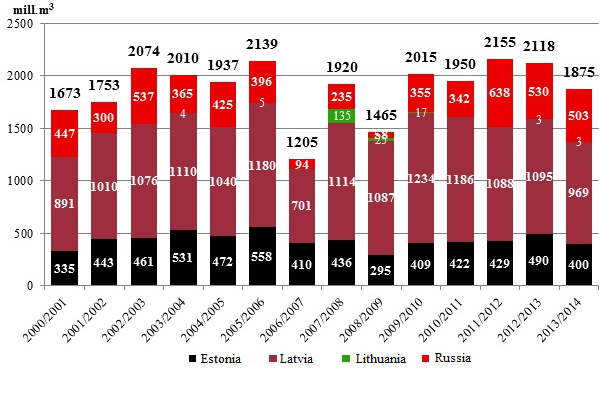

Since 2010 the consumption of natural gas has decreased in

Latvia (see Figure 14). The main sectors where natural gas is

consumed are the transformation sector (energy sector), industry,

and construction, as well as the household or individual

consumption sector. Approximately more than 50 % of the total

consumption of natural gas in the country is used for the

generation of electricity and centralised thermal energy in

cogeneration plants. The two largest power plants of Latvia (Rīga

1 and 2 thermal power plants) are the plants of combined cycle

natural gas in which electricity and heat for the heating supply

of the Riga city is simultaneously generated. Taking into account

the seasonal nature of high heat loads, intensity of the large

cogeneration plant electricity generation in co-generation mode

is also seasonal.

Source: CSB

Figure 14. Total consumption of

natural gas in Latvia in 2000-2013, mill. m3 per

year

The total consumption of natural gas is affected by the

following factors:

• external air temperature that, for example, significantly

exceeded the average statistical norm during the warm winter

period in 2013;

• joint development of national economy, including industry.

For example, in 2013 the operation of Liepājas Metalurgs

AS which is one of the largest energy consumers in the

country was temporarily suspended;

• transition from natural gas to alternative fuels in the

generation of centralised heat;

• introduction of energy efficiency measures, for example,

thermal insulation of buildings.

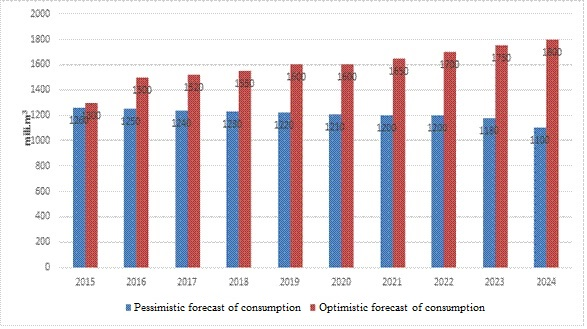

The natural gas transmission system operator has developed the

forecast of the natural gas consumption of Latvia for two

scenarios - pessimistic and optimistic (see Figure 15). The

pessimistic scenario takes into account the specific objectives

for the improvement of energy efficiency and accordingly

reduction of the total consumption of primary energy resources,

for the replacement of imported energy resources with local

energy resources, including RES, as a result of which gradual

reduction of natural gas consumption is foreseen in Latvia from

1260 mill. m3 in 2015 to 1100 mill. m3 in

2024 (see Figure 15).

Source: Annual evaluation report of the natural gas

transmission system operator on 2014.

Figure 15. Forecast of natural gas

consumption for 2015-2020 (the pessimistic and optimistic

scenario), mill. m3

In the optimistic scenario changes in the consumption of

natural gas are anticipated, taking into account the

globalisation trends of the natural gas market and the

development of new technologies as a result of which the prices

of energy resources could become more equivalent, as well as the

planned development of the natural gas market as a result of

which the Eastern Baltic region, including Latvia, will be

provided with supplies of natural gas that are alternative to

supplies from Russia, and isolation of the natural gas market of

the Baltic States and Finland from the joint EU natural gas

market will be prevented.

Increase in consumption of natural gas might be facilitated by

reduction in prices of oil products and, therefore, also natural

gas. Thus, the share of natural gas as the fossil fuel that is

most friendly to the environment in the total balance sheet of

energy resources might remain in the current level, ensuring a

small increase in the demand for natural gas from 1300

mill.m3 in 2015 to 1800 mill.m3 in 2024

(see Figure 21).

In case of the optimistic scenario it is expected that the

structure of the use of natural gas will change and, as a result

of support of energy efficiency measures and renewable energy

sources, the consumption of natural gas will decrease in

centralised heating supply, however, it will increase in

transport, manufacturing, and decentralised heating systems.

Taking into account the significantly lower intensity of

emissions compared to coal and oil products, and the development

of market in the world, natural gas will preserve a significant

role in the balance sheet of primary energy resources of Latvia

alongside with renewable energy sources.

Consumption of natural gas may be affected by more extensive

use of natural gas in the transport sector. In relation to

introduction of the requirements of Directive 2014/94/EC (see

Sub-section 3.3.3). According to the forecasts of sectoral

representatives the number of vehicles operated by natural gas

might increase until the end of 2020.

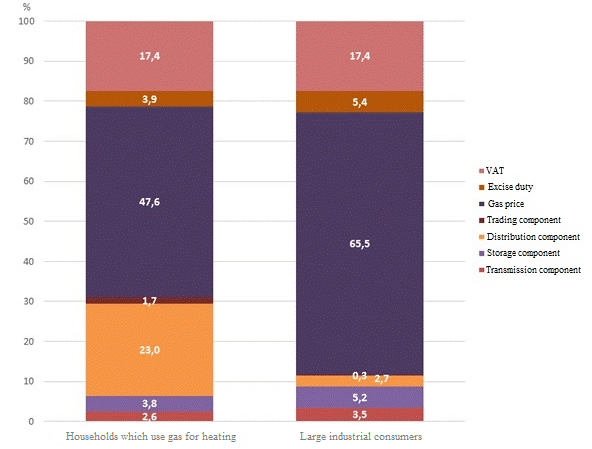

The total price of natural gas is formed by the price of

natural gas, the trading component, services of the storage,

transmission and distribution system, trading service, and tax

(see Figure 16).

Source: Ministry of Economics

Figure 16. Structure of the natural

gas price/tariff (%)

In 2009, Latvijas Gāze AS entered into long-term

contracts with gas suppliers Gazprom AAS and ITERA

Latvija SIA until 2030 which provide for sufficient supplies

of natural gas to consumers in Latvia. These contracts also lay

down the technical parameters of the natural gas supply

(pressure, calority, etc.), supply and storage amounts (annual

and monthly), formula for calculating the prices of natural gas,

payment conditions, conditions for reviewing the contracts, and

other liabilities. As it is common in the natural gas business,

the supply contracts include the "take-or-pay" clause.

The formula for calculating the price of natural gas laid down

in the contracts takes into account the price/quotation index FOB

ARA (Free On Board Amsterdam, Rotterdam, Antwerp) of heavy fuel

oil with sulphur content up to 1 % and diesel fuels with sulphur

content up to 0.1 % in exchanges of oil products, as well as the

relation of the rate of euro specified by the European Central

Bank and the USA dollar.

In 2014, 5 contracts were entered into for the transportation

and storage of natural gas in Inčukalns UGSF (see Table 3).

Table 3.

Existing long-term natural gas

supply contracts of Latvijas Gāze AS

| Contracting party |

Date of signing |

Term of operation |

Service |

|

LITGAS UAB

|

30 December 2013 |

10 February 2017 |

Transport, storage |

| Lietuvos duju tiekimas

UAB |

19 December 2014 |

1 April 2017 |

Transport, storage |

| Baltic Energy Partners OÜ |

30 October 2014 |

31 December 2014 |

Transport |

| Baltic Energy Partners OÜ |

19 December 2014 |

30 April 2015 |

Transport |

| Elering Gaas AS (EG Võrguteenus AS) |

19 December 2014 |

31 December 2015 |

TSO |

Five more contracts for the transportation and storage of

natural gas were entered into in 2015.

Latvijas Gāze

AS

The largest stockholders of the Latvijas Gāze AS are

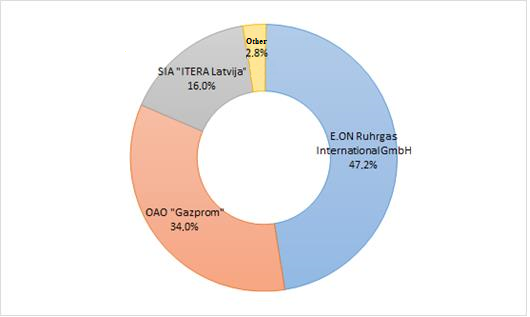

E.ON Ruhrgas International GmbH, Gazprom AAS, and

ITERA Latvija SIA (see Figure 17). The largest stockholder

of Latvijas Gāze AS E.ON Ruhrgas International GmbH

has published a notification on the planned withdrawal from the

natural gas market of the Baltic States, including Latvia. The

stocks of Latvijas Gāze AS are quoted on the NASDAQ OMX

Rīga exchange, and their total number is 39.9 million.

Source: Latvijas Gāze AS

Figure 17. Structure of the

Latvijas Gāze AS shareholders, as of 31 December 2013

Until the natural gas market liberalisation is completed, the

Latvijas Gāze AS keeps being a vertically integrated

undertaking which provides trading, distribution, transmission,

and storage services. By fulfilling the requirements of Directive

2009/73/EC it is expected that after 3 April 2017 the

transmission and storage functions in the natural gas sector of

Latvia will be completely separated from trading.

Within the context of Directive 2009/37 EC two individual

derogations from several requirements which are applicable within

different terms, correspond to Latvia.

- "Emergent market" derogation was in force until 4 April

2014, when ten years had passed since the first commercial

natural gas supply according to the first long-term contract.

Therefore, starting from 4 April 2014 access of the third parties

to the natural gas distribution, transmission systems and natural

gas storage facility, introduction of the balancing fee, and

prohibition of cross-subsidisation should be ensured as provided

for in amendments of 13 March 2014 to the Energy Law.

- "Isolated market" derogation which was in force until the

moment when Latvia is connected to the natural gas systems of any

European Union Member State, except for Estonia, Lithuania, and

Finland, or the dominating supplier̕'s share in the total natural

gas consumption of Latvia will decrease below 75 %.

Taking into account that from 2015 natural gas supplies are

physically possible also from the LNG terminal of Lithuania and

alongside with reconstruction of the gas pipe Klaipėda-Kiemėnai

there is a theoretical possibility that the share of the

dominating supplier in provision of the total natural gas

consumption of Latvia is less than 75 %, derogations from

Directive 2009/73/EC are not applicable to Latvia anymore.

3.3. Energy Infrastructure

Implementation of the infrastructure projects is a significant

aspect to complete the establishment of the internal market.

Closer integration of networks is of particular importance to the

countries the electricity or natural gas networks of which are

not connected to other EU countries, the so called "energy

islands".

For the time period from 2014 to 2020 a new financial

instrument has been established at the EU level within the

framework of which investments in the development of the EU

infrastructure in the field of transport, energy and

telecommunications - Connecting Europe Facility (hereinafter -

the CEF) - will be supported. The budget provided for the energy

sector for the time period from 2014 to 2020 within the scope of

the CEF forms 4.7 bill. euros.

In order to promote introduction of projects, implementation

of the long-term energy infrastructure policy is determined by

Regulation No 347/2013 of the European Parliament and of the

Council of 17 April 2013 on guidelines for trans-European energy

infrastructure and repealing Decision No 1364/2006/EC and

amending Regulations (EC) No 713/2009, (EC) No 714/2009 and (EC)

No 715/2009 (hereinafter - Regulation No 347/2013). Regulation No

347/2013 determines the establishment of lists of Projects of

Common Interest (hereinafter - the PCI) at the EU level. It is

provided for in Regulation No 347/2013 that projects which are

included in the PCI list will not only be able to apply for

financing, but also will be able to use procedures for rapid and

efficient receipt of permits, concurrently conforming to the

environmental assessment and protection standards. In order to

implement the requirements of Regulation No 347/2013, on 14

October 2013, using the procedure of delegated acts, the EC

adopted the first PCI list of the European Union (EC Regulation

No 1391/2013) which includes 248 projects - electricity and gas

transmission, storage and LNG projects, as well as projects in

the field of smart networks and oil. On 18 November 2015 the EC

presented the second PCI list of the European Union. The second

PCI list of the European Union which includes 195 projects in

total, will officially come into force at the beginning of 2016.

Regulation No 347/2013 also provides for the possibilities of

receiving EU support in cases when such projects are of strategic

importance, however, cannot be implemented, taking into account

only the market interests. The abovementioned Regulation will be

in force until 2020, and within this period the PCI list is

intended to be updated after every two years (in 2017 and 2019

accordingly). The role of the competent authority provided for

within the framework of Regulation No 347/2013 which is assigned

to facilitate the administrative procedures in relation to

introduction of the PCI of the energy sector is assigned to the