Aicinām vēl šonedēļ piedalīties lietotāju apmierinātības aptaujā!

Paldies par viedokli!

|

The translation of this document is outdated.

Translation validity: 22.11.2023.–13.03.2025. Amendments not included: 11.03.2025.

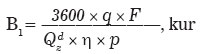

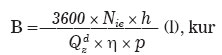

Procedures by which a Reduced Rate of Excise Duty or Exemption from Excise Duty shall be Applied to Individual Petroleum ProductsIssued pursuant to [25 June 2019; 21 December 2021] I. General Provisions1. The Regulation prescribes: 1.1. the procedures by which a reduced rate of excise duty (hereinafter - the duty) or exemption from the duty shall apply to petroleum products which are supplied and used according to Section 5, Paragraph five and Section 18, Paragraph one of the law On Excise Duties (hereinafter - the Law), or Section 3, Paragraphs seven, eight, and nine of the law On the Application of Taxes in Free Ports and Special Economic Zones, and also the procedures and cases where the conditions for the movement and control of excise goods provided for in the Law shall not apply; 1.2. the procedures by which individual petroleum products shall be labelled (marked) in order to apply thereto Section 14, Paragraph two or Section 18, Paragraph three of the Law, or Section 3, Paragraphs 8.1 and nine of the law On the Application of Taxes in Free Ports and Special Economic Zones; 1.3. the circulation of labelled (marked) petroleum products; 1.4. the procedures by which the State Revenue Service shall issue, re-register, or cancel the statement for the purchase of the petroleum products subject to duty exemption or relief and by which it shall issue the permit for the transfer or sale of the remainder of the petroleum products. [25 June 2019; 21 December 2021] 2. In accordance with this Regulation, the petroleum products referred to in Section 14, Paragraph two and Section 18, Paragraph three of the Law and Section 3, Paragraphs 8.1 and nine of the law On the Application of Taxes in Free Ports and Special Economic Zones shall be labelled (marked). 3. Section 14, Paragraph two of the Law or Section 3, Paragraph nine of the law On the Application of Taxes in Free Ports and Special Economic Zones shall apply if diesel fuel, petroleum, or fuel oil whose colorimetric index is less than 2.0 and kinematic viscosity at 50 °C is less than 25 mm2/s, or the substitute products and components of these petroleum products are labelled (marked) in accordance with this Regulation and they are supplied in accordance with the requirements referred to in Chapter IV of this Regulation. 4. [21 December 2021] 5. The petroleum products which are supplied and used for the purposes referred to in Section 18, Paragraph one, Clauses 1 and 6 of the Law shall be exempt from the duty if they are supplied in accordance with the requirements referred to in Chapter V of this Regulation, even if they are not labelled (marked) in accordance with this Regulation. [17 June 2009] 6. Section 18, Paragraph one, Clauses 2 and 3 of the Law shall apply if in the cases specified therein petroleum products are supplied in accordance with the requirements referred to in Chapter VI of this Regulation. 7. Section 3, Paragraph eight, Clauses 1, 2, and 3 of the law On the Application of Taxes in Free Ports and Special Economic Zones shall apply if in the cases specified therein petroleum products are supplied in accordance with the requirements referred to in Chapter VI of this Regulation. 8. Section 18, Paragraph one, Clause 4 of the Law or Section 3, Paragraph eight, Clause 4 of the law On the Application of Taxes in Free Ports and Special Economic Zones shall apply if petroleum products are supplied in accordance with the requirements referred to in Chapter IV of this Regulation. 9. Section 18, Paragraph one, Clause 5 of the Law shall apply if petroleum products are supplied in accordance with the requirements referred to in Chapter VII of this Regulation. 10. The petroleum products specified in this Regulation shall be supplied to the address indicated in the statement issued in accordance with this Regulation and also shall be filled into the tanks specified in the statement (if any are indicated), unless it has been laid down otherwise in this Regulation. 11. A person that supplies petroleum products to which a reduced rate of the duty or exemption from the duty applies (hereinafter - the supplier) to a person that uses petroleum products to which a reduced rate of the duty or exemption from the duty applies (hereinafter - the user) shall submit the reports provided for in the laws and regulations regarding the circulation of excise goods. 12. In accordance with the laws and regulations governing accounting and the laws and regulations regarding the circulation of excise goods, the supplier shall issue a supply document (hereinafter - the fuel supply document) for the supply of petroleum products, whereas the supplier shall issue a source document (hereinafter - the fuel source document) for transactions or actions with petroleum products. The fuel supply document and the fuel source document shall, in addition to the details provided for in the laws and regulations regarding the circulation of excise goods, contain the following information: 12.1. if petroleum products are supplied on the basis of the statement issued in accordance with this Regulation - the type, number, and date of issue of the statement issued to the user to whom the petroleum products are being supplied; 12.2. if petroleum products are supplied for the purposes referred to in Section 18, Paragraph one, Clauses 2 and 3 of the Law or Section 3, Paragraph eight, Clauses 1, 2, and 3 of the law On the Application of Taxes in Free Ports and Special Economic Zones - the registration numbers and places of registration of the aircraft (aeroplanes or other aerial means of transport) or ships (ships or other waterborne vessels) (except if petroleum products are supplied for the purposes referred to in Section 3, Paragraph eight, Clause 2 of the law On the Application of Taxes in Free Ports and Special Economic Zones) or the filling station referred to in Paragraph 95 of this Regulation that is specially equipped to supply ships; 12.3. whether the supplied petroleum products are labelled (marked); 12.4. the purpose of use of the petroleum products; 12.5. if petroleum products are supplied for the purposes referred to in Section 18, Paragraph one, Clause 3 of the Law or Section 3, Paragraph eight, Clauses 1, 2, and 3 of the law On the Application of Taxes in Free Ports and Special Economic Zones and the vehicle (if necessary, also the second vehicle) used is a ship which performs the bunkering or supply of ships - the registration number and place of registration of the ship that performs the bunkering or supply of ships; 12.6. if the user accepts only a part of the delivered amount of petroleum products - the amount of the accepted petroleum products. The user shall certify it with a signature. The supplier shall move the remaining amount of petroleum products, together with the same fuel supply document, back to the address of loading (filling) area; 12.7. for pre-packaged petroleum products - the number of packaging units and the amount (in litres) in each packaging unit. [30 March 2010; 15 June 2010] 13. The fuel supply document shall be issued if the petroleum products of one merchant are reloaded (pumped) from one ship to another ship. [30 March 2010; 10 February 2015] 14. If petroleum products are moved from a tax warehouse located in an airport area where a border crossing point has been established (hereinafter - the international airport) to an aircraft to supply it with petroleum products at such an international airport, using vehicles that are not involved in road traffic, and the movement of petroleum products is impossible in accordance with the procedures laid down in Sub-paragraph 12.6 of this Regulation, the supplier shall draw up the fuel supply document for the amount of fuel supplied to the aircraft. In this case, the following shall be indicated in the fuel supply document: 14.1. in the section regarding the consignee of petroleum products and the unloading point, only the name and address of the relevant international airport, the name of the merchant, the registration number of the aircraft, and the flight number shall be indicated; 14.2. in the section regarding the loading point, the loading (filling) area and the reference number of the tank or tank compartment, or the pressure equipment complex tank, or the registration number of the vehicle used to supply petroleum products to the aircraft shall be indicated; 14.3. in the section regarding petroleum products, only the following information shall be indicated: 14.3.1. the type, brand, and code of the Combined Nomenclature; 14.3.2. the actual temperature and actual density; 14.3.3. the filled in amount (in litres or (and) kilograms); 14.3.4. whether the supplied petroleum products are labelled (marked). [15 June 2010; 10 February 2015] 15. [17 June 2009] 16. [15 June 2010] 17. If petroleum products are moved in accordance with the procedures referred to in Paragraph 14 of this Regulation, the supplier shall, according to the laws and regulations governing the circulation of excise goods, perform accounting of the goods, including the petroleum products which have been filled in a vehicle for aircraft supply. [15 June 2010] 18. [15 June 2010] 19. If petroleum products are supplied for the purposes referred to in Section 18, Paragraph one, Clause 3 of the Law or Section 3, Paragraph eight, Clauses 1 and 3 of the law On the Application of Taxes in Free Ports and Special Economic Zones from the filling stations referred to in Paragraph 95 of this Regulation that is specially equipped to supply ships, the supplier shall, in addition to the details provided for in the laws and regulations regarding electronic cash register system receipts and the procedures for the circulation thereof, indicate the following in the electronic cash register system receipt: 19.1. the name of the user; 19.2. ship registration number and place of registration; 19.3. whether the supplied petroleum products are labelled (marked); 19.4. the note "exemption for ships". 20. In addition to the accounting provided for by the laws and regulations governing the circulation of excise goods, the supplier shall indicate the following information: 20.1. if petroleum products are supplied on the basis of the statement issued in accordance with this Regulation - the type, number, and date of issue of the statement issued to the user to whom the petroleum products are being supplied; 20.2. if petroleum products are supplied for the purposes referred to in Section 18, Paragraph one, Clauses 2 and 3 of the Law or Section 3, Paragraph eight, Clauses 1, 2, and 3 of the law On the Application of Taxes in Free Ports and Special Economic Zones - the registration numbers and places of registration of the aircraft or ships (except for the case referred to in Paragraph 14 of this Regulation and if petroleum products are supplied for the purposes referred to in Section 3, Paragraph eight, Clause 2 of the law On the Application of Taxes in Free Ports and Special Economic Zones) or the filling station referred to in Paragraph 95 of this Regulation that is specially equipped to supply ships; 20.3. the amount of petroleum products in accordance with the purpose of use of the petroleum products, indicating labelled (marked) and unlabelled (unmarked) petroleum products separately; 20.4. the purpose of use of the petroleum products. [17 June 2009] 20.1 [1 February2019 / See Paragraph 2 of Amendments] 20.2 The user shall submit the submission for the obtaining, re-registration, or cancellation of the statements specified in this Regulation electronically using the Electronic Declaration System of the State Revenue Service. If the user is not a client of the Electronic Declaration System of the State Revenue Service, the submission may be submitted in paper form. [25 June 2019] 20.3 The data on the purchase of the authorised amount of petroleum products allocated to the user shall be recorded and the accounting of the purchased amount of petroleum products shall be ensured in the Electronic Application System of the Rural Support Service. [17 July 2018 / Paragraph shall come into force on 1 February 2019. See Paragraph 2 of Amendments] 20.4 The State Revenue Service shall issue the statements specified in this Regulation electronically in accordance with the laws and regulations regarding the circulation of electronic documents by using the Electronic Declaration System of the State Revenue Service. If the user is not a client of the Electronic Declaration System of the State Revenue Service, the statement shall be issued in paper form and sent to the legal address or declared place of residence of the user. [25 June 2019] 20.5 If the name, surname, or title of the user indicated in the statement changes, the State Revenue Service shall update the information indicated in the statement and send or issue the re-registered statement to the user. [25 June 2019] II. Labelling (Marking) of Oil Products21. It is permitted to label (mark) petroleum products in a tax warehouse and only by an approved warehousekeeper (hereinafter - the warehousekeeper) that has been granted such rights. [30 March 2010] 21.1 If the flow method is used for the labelling (marking) of petroleum products, the warehousekeeper shall submit to the State Revenue Service a description of the technological process approved by a test laboratory accredited by a national accreditation body in accordance with the laws and regulations regarding the assessment, accreditation, and supervision of conformity assessment bodies, or by a test laboratory accredited by another European Union Member State. [10 February 2015] 22. The warehousekeeper shall notify the State Revenue Service in paper or electronic form of the time of labelling (marking) not later than two working days before the labelling (marking) of the petroleum products. [17 June 2009] 23. The warehousekeeper shall ensure and shall be responsible for the labelling (marking) of petroleum products in the Republic of Latvia in accordance with this Regulation. 24. Petroleum products shall be labelled (marked) by using the equipment (devices) which conforms to fire safety, environmental protection, operational, and technical requirements. 25. Petroleum products shall be considered labelled (marked) if the red dye referred to in Paragraph 26 of this Regulation and the chemical substance referred to in Paragraph 27 of this Regulation (fiscal marker) have been added to 1000 litres of petroleum products in the corresponding amount. [14 November 2023] 26. N-ethyl-1-(4-phenylazophenylazo)naphthyl-2-amine (CAS number 6368-72-5) shall be used as the red dye - at least 5.0 grams. [14 November 2023] 27. Butoxybenzene (CAS number 1126-79-0) shall be used as the chemical substance (fiscal marker) - at least 9.5 grams but no more than 14.0 grams. [14 November 2023] 28. The warehousekeeper shall ensure the procurement of the substances referred to in Paragraphs 26 and 27 of this Regulation. 28.1 The labelling (marking) of petroleum products by using the flow method in the dispensing process shall ensure the uniform and continuous mixing of the petroleum products involved and the substances referred to in Paragraph 25 of this Regulation in the correct proportions and the equipment used shall ensure full automation of the technological process and computer program management. [10 February 2015] 29. The warehousekeeper shall store the labelled (marked) petroleum products, if they are not labelled (marked) using the flow method, in a separate tank specifically intended for them, bearing the inscription "Iezīmēti (marķēti) naftas produkti" [Labelled (marked) petroleum products] and whereof the State Revenue Service has been informed in writing. It is prohibited to store other petroleum products in the abovementioned tank. The tank in which the labelled (marked) petroleum products are stored shall be equipped with a meter that complies with the laws and regulations regarding the metrological requirements for the specific measuring instrument and that ensures accumulated and permanent accounts of the labelled (marked) petroleum products dispensed from the tank. If the labelled (marked) petroleum products are stored in tanks that are connected into a technologically integrated system, the stationary dispensing device shall be equipped with the appropriate meter. [17 June 2009; 10 February 2015] 30. The warehousekeeper shall ensure that the authorised officials of the State Revenue Service or other control authorities have free access to the tanks in which the labelled (marked) petroleum products are stored. 31. Prior to the supply of the labelled (marked) petroleum products to users, the warehousekeeper shall obtain a document (and its translation into the official language if the document is issued in another European Union Member State) issued by the customs laboratory of the State Revenue Service or a test laboratory accredited by a national accreditation body in accordance with the laws and regulations regarding the assessment, accreditation, and supervision of conformity assessment bodies, or by a test laboratory accredited by another European Union Member State that shall contain details (information) certifying that the relevant petroleum products are labelled (marked) in accordance with the requirements laid down in Paragraph 25 of this Regulation (hereinafter - the supporting document). [3 November 2009; 30 March 2010] 31.1 If petroleum products are labelled (marked) using the flow method, the conformity with the requirements referred to in Paragraph 25 of this Regulation shall be certified by a conformity certification in which the warehousekeeper shall include at least the following information: 31.1 1. the name and address of the tax warehouse; 31.1 2. the amount of labelled (marked) petroleum products; 31.1 3. the name of the test laboratory referred to in Paragraph 21.1 of this Regulation which has approved the description of the technological process for the labelling (marking) of petroleum products using the flow method, the accreditation body, the number of the approved technological process and the date; 31.1 4. the conformity certification with the substance mixing requirements referred to in Paragraph 25 of this Regulation; 31.1 5. the position, name and surname, and signature of the person issuing the conformity certification, the date and place of issue. [10 February 2015] 32. In order to obtain the supporting document referred to in Paragraph 31 of this Regulation, the warehousekeeper shall take a sample (at least one litre) of the labelled (marked) petroleum products from the tank in which the labelled (marked) petroleum products are stored, seal the packaging of the sample, and submit it to the customs laboratory of the State Revenue Service or a test laboratory accredited by a national accreditation body in accordance with the laws and regulations regarding the assessment, accreditation, and supervision of conformity assessment bodies, or by a test laboratory accredited by another European Union Member State in order to determine whether the petroleum products are labelled (marked) in accordance with the requirements laid down in Paragraph 25 of this Regulation. [10 February 2015] 33. When technically equipping a tank in accordance with the requirements referred to in Paragraph 29 of this Regulation, the warehousekeeper shall ensure that during the sampling and also during the time period when the relevant labelled (marked) petroleum products are supplied to users, no other petroleum products (or other substances) are filled into the tank in which the labelled (marked) petroleum products are stored. If the tank is refilled with petroleum products (or other substances), the previously issued supporting document referred to in Paragraph 31 of this Regulation shall cease to be valid and the warehousekeeper shall be required to obtain a new supporting document to be able to supply the relevant petroleum products to users. [17 June 2009] 34. In order to control the conformity with the requirements referred to in Paragraph 33 of this Regulation, the warehousekeeper shall seal the tank in which the labelled (marked) petroleum products are stored and its equipment (including after sampling). The warehousekeeper shall coordinate the procedures for sealing the tank with the State Revenue Service. The State Revenue Service is entitled to require that the tank and its equipment are sealed in the presence of the responsible official of the State Revenue Service. [17 June 2009] 35. [17 June 2009] 36. The warehousekeeper shall, in accordance with the laws and regulations governing the circulation of excise goods, record the labelled (marked) petroleum products and actions with them and shall additionally record the meter readings after each dispensing. 37. In the report on the circulation of petroleum products (fuel) provided for in the laws and regulations governing the circulation of excise goods, the warehousekeeper shall also provide details on the petroleum products labelled (marked) during the previous month and the labelled (marked) petroleum products supplied to users. III. Procedures by Which Petroleum Products to Which a Reduced Rate of the Duty or Exemption from the Duty Applies Shall Be Brought into the Republic of Latvia38. It shall be permitted to bring (import) petroleum products into the Republic of Latvia from a foreign country that is not a European Union Member State to apply Section 14, Paragraph two of the Law and Section 18, Paragraph one of the Law or Section 3, Paragraphs eight and nine of the law On the Application of Taxes in Free Ports and Special Economic Zones under the condition that these are moved to a tax warehouse where it is permitted to perform actions with petroleum products. This condition shall not apply to products to which Section 18, Paragraph one, Clauses 2, 3, and 6 of the Law or Section 3, Paragraph eight, Clauses 1, 2, and 3 of the law On the Application of Taxes in Free Ports and Special Economic Zones apply if the supply of the relevant products takes place in accordance with the customs procedure, i.e. release for free circulation. [17 June 2009; 21 December 2021] 39. The conditions referred to in Paragraph 38 of this Regulation shall not apply to petroleum products which a user brings in according to Section 18, Paragraph one, Clause 1 of the Law to be used for purposes other than fuel or heating fuel if the relevant products: 39.1. fall under the Combined Nomenclature codes 2710 12 21, 2710 12 25, and 2710 19 29 and in accordance with the requirements of technical regulations or standards are filled into sealed package with the volume not exceeding 250 litres, prepared for sale and are not intended to be used for the operation of internal combustion engines (with spark ignition and with compression ignition); 39.2. fall under the Combined Nomenclature code 2905 11 00; 39.3. are not referred to in Paragraph 41 of this Regulation. [17 June 2009; 10 February 2015] 40. Paragraphs 29, 30, 31, 32, 33, 34, 36, and 37 of this Regulation shall apply to the labelled (marked) petroleum products referred to in Paragraph 38 of this Regulation. [17 June 2009] 41. If petroleum products (including labelled (marked) petroleum products) are brought into the Republic of Latvia from other European Union Member States, the requirements prescribed by the Law (including the conditions regarding the taxpayer and also the requirements laid down in Section 25 of the Law) shall apply to such petroleum products (including labelled (marked) petroleum products) that fall under the following Combined Nomenclature goods items and codes: 41.1. 1507-1518 if these products are intended to be used as heating fuel or fuel; 41.2. 2707 10, 2707 20, 2707 30, and 2707 50; 41.3. 2710 12-2710 20 90 (if the products that conform to the Combined Nomenclature codes 2710 12 21, 2710 12 25, and 2710 19 29 in accordance with the requirements of technical regulations or standards are filled into a sealed package with the volume not exceeding 250 litres, prepared for sale and are not intended to be used for the operation of internal combustion engines (with spark ignition and with compression ignition), they may be imported in accordance with the conditions referred to in Paragraph 43 of this Regulation); 41.4. 2711 (except for 2711 11, 2711 21, and 2711 29); 41.5. 2901 10; 41.6. 2902 20, 2902 30, 2902 41, 2902 42, 2902 43, and 2902 44; 41.7. 2905 11 00 if they are not products of synthetic origin and these products are intended to be used as heating fuel or fuel; 41.8. 3824 90 97 if these products are intended to be used as heating fuel or fuel. [17 June 2009; 10 February 2015] 42. In compliance with the requirements laid down in the Law (including the conditions regarding the taxpayer and also the requirements laid down in Section 25 of the Law), it shall be permitted to bring into the Republic of Latvia from other European Union Member States such petroleum products (including labelled (marked) petroleum products) which are not referred to in Paragraph 41 of this Regulation. 43. In accordance with Section 18, Paragraph one, Clause 1 of the Law, the user may bring into the Republic of Latvia from other European Union Member States (without submitting a duty security or using the documents specified in Commission Regulation (EC) No 684/2009 of 24 July 2009 implementing Council Directive 2008/118/EC as regards the computerised procedures for the movement of excise goods under suspension of excise duty) petroleum products for use for purposes other than fuel or heating fuel that: 43.1. fall under the Combined Nomenclature codes 2710 12 21, 2710 12 25, and 2710 19 29 if, in accordance with the requirements of technical regulations or standards, these are filled into sealed package with the volume not exceeding 250 litres, prepared for sale and are not intended for the operation of internal combustion engines (with spark ignition and with compression ignition); 43.2. fall under the Combined Nomenclature code 2905 11 00; 43.3. are not referred to in Paragraph 41 of this Regulation. [17 June 2009; 30 March 2010] 44. It shall be permitted to bring the labelled (marked) petroleum products referred to in Paragraph 41 of this Regulation into the Republic of Latvia if there is a relevant supporting document. 45. Paragraph 29 of this Regulation shall apply to the labelled (marked) petroleum products referred to in Paragraph 41 of this Regulation. Authorised officials of the State Revenue Service or other control authorities shall have free access to the tanks in which the labelled (marked) petroleum products are stored. 46. The tank in which the labelled (marked) petroleum products referred to in Paragraph 41 of this Regulation are stored and its equipment shall be sealed. The procedures for the sealing shall be coordinated with the State Revenue Service. The State Revenue Service is entitled to require that the tank and its equipment are sealed by an employee of the State Revenue Service or in his or her presence. [17 June 2009] IV. Labelled (Marked) Petroleum Products Supplied and Used in Free Ports and Special Economic Zones and also Used as Heating Fuel[21 December 2021] 47. The user shall obtain a statement on the right to purchase labelled (marked) petroleum products (hereinafter - the statement for the purchase of labelled (marked) petroleum products) which is provided for: 47.1. in Annexes 6 and 7 to this Regulation to be able to use the labelled (marked) petroleum products for the purposes specified in Section 14, Paragraph two or Section 18, Paragraph one, Clause 4 of the Law or Section 3, Paragraph eight, Clause 4 of the law On the Application of Taxes in Free Ports and Special Economic Zones; 47.2. in Annex 8 to this Regulation to be able to use the labelled (marked) petroleum products for the purposes specified in Section 3, Paragraph nine of the law On the Application of Taxes in Free Ports and Special Economic Zones. [17 June 2009] 48. [21 December 2021] 49. The statement referred to in Sub-paragraph 47.1 of this Regulation for the purchase of labelled (marked) petroleum products shall be issued for an indefinite period. The statement referred to in Sub-paragraph 47.2 of this Regulation for the purchase of labelled (marked) petroleum products shall be issued for a year. [17 June 2009; 21 December 2021] 50. If the user is a natural person, in order to obtain the statement for the purchase of labelled (marked) petroleum products (for use as heating fuel), the user shall submit a submission in accordance with Annex 1 to this Regulation. The submission shall be submitted to the State Revenue Service. The following documents shall be appended to the submission: 50.1. a copy of the technical passport for the relevant combustion plant, electric power generation plant, or the combined plant that generates electric power and heat (hereinafter - the combustion plant) with a reference regarding the capacity of the plant; 50.2. documents that certify the right to possession of the relevant building or the right to perform the management of the relevant building and documents containing information on the area (m2) or volume (m3) of the building to be heated according to external dimensions, or the heating supply project in which the heat consumption is indicated; 50.3. [21 December 2021]; 50.4. a calculation of the required amount of the type of labelled (marked) petroleum products made by using the methods referred to in Paragraph 55 of this Regulation and the information indicated in the documents referred to in Sub-paragraphs 50.1 and 50.2 of this Regulation; 50.4.1 a layout of the storage tanks and combustion plants, showing the location of the fuel meter; 50.4.2 an explanation if it is technically impossible to ensure that the tanks and the combustion plants are connected into a technologically integrated system; 50.5. if the amount of the labelled (marked) petroleum products to be consumed exceeds 7000 litres per year: 50.5.1. documents that certify that the relevant combustion plant or the storage tank for labelled (marked) petroleum products which is connected to the relevant combustion plant is equipped with a meter that ensures accumulated and permanent accounts of the heating fuel consumed; 50.5.2. and labelled (marked) petroleum products are stored in tanks which are connected into a technologically integrated system - documents that certify that the tank in the technologically integrated system which is connected to the relevant combustion plant is equipped with a meter that ensures accumulated and permanent accounts of the heating fuel consumed; 50.5.3. and that the meter is not the original part of the relevant combustion plant or the storage tank for labelled (marked) petroleum products or part of the technologically integrated system which is connected to the relevant combustion plant and it is installed separately - a copy of the technical passport for the meter. [17 June 2009; 3 November 2009; 10 February 2015; 21 December 2021] 51. If the user is not a natural person, in order to obtain the statement for the purchase of labelled (marked) petroleum products (for use as heating fuel), the user shall submit a submission in accordance with Annex 3 to this Regulation. The submission shall be submitted to the State Revenue Service. The following documents shall be appended to the submission: 51.1. a copy of the technical passport for the relevant combustion plant with a reference regarding the capacity of the plant; 51.2. information on the type of labelled (marked) petroleum products used and the maximum consumption in the relevant combustion plant: 51.2.1. the types and number of combustion plants; 51.2.2. the rated output of the combustion plant (MW); 51.2.3. the planned operation time during the reference period (h); 51.2.4. [10 February 2015]; 51.2.5. [10 February 2015]; 51.2.6. the lowest combustion heat (kJ/kg) and density (kg/l) of the labelled (marked) petroleum products; 51.2.7. the efficiency factor of the plant in accordance with the technical passport data of the relevant combustion plant; 51.2.8. [10 February 2015]; 51.2.9. [10 February 2015]; 51.2.10. [10 February 2015]; 51.3. the total amount (in litres) of labelled (marked) petroleum products used in the relevant combustion plant during a specific time period (for example, in a month, in a year) which is calculated by using the information indicated in the documents referred to in Sub-paragraphs 51.1, 51.2, and 51.4 of this Regulation; 51.4. if labelled (marked) petroleum products are intended to be used for the production of heat for heating - documents that certify the right to possession of the relevant building or the right to perform the management of the relevant building and documents containing information on the area (m2) or volume (m3) of the building to be heated according to external dimensions, or the heating supply project in which the heat consumption is indicated; 51.5. if labelled (marked) petroleum products are intended to be used for the production of heat energy in the technological process of product manufacturing (processing) or for the production or use of electric power in combined plants that produce electric power and heat energy: 51.5.1. documents that certify the right to possession of the site where the manufacturing process (processing) will take place; 51.5.2. the amount of labelled (marked) petroleum products required that is calculated by using the methods referred to in Paragraph 56 of this Regulation; 51.5.1 a layout of the storage tanks and combustion plants, showing the location of the fuel meter; 51.5.2 an explanation if it is technically impossible to ensure that the tanks and the combustion plants are connected into a technologically integrated system; 51.6. if the amount of the labelled (marked) petroleum products to be consumed exceeds 7000 litres per year: 51.6.1. documents that certify that the relevant combustion plant or the storage tank for labelled (marked) petroleum products which is connected to the relevant combustion plant is equipped with a meter that ensures accumulated and permanent accounts of consumption; 51.6.2. and labelled (marked) petroleum products are stored in tanks which are connected into a technologically integrated system - documents that certify that the tank in the technologically integrated system which is connected to the relevant combustion plant is equipped with a meter that ensures accumulated and permanent accounts of the heating fuel consumed; 51.6.3. and that the meter is not the original part of the relevant combustion plant or the storage tank for labelled (marked) petroleum products or part of the technologically integrated system which is connected to the relevant combustion plant and it is installed separately - a copy of the technical passport for the meter. [17 June 2009; 3 November 2009; 10 February 2015; 21 December 2021] 52. In order to obtain the statement for the purchase of labelled (marked) petroleum products (for use in free ports and special economic zones in accordance with Section 3, Paragraph nine of the law On the Application of Taxes in Free Zones and Special Economic Zones), the user shall submit a submission to the State Revenue Service in accordance with Annex 5 to this Regulation. If the equipment or machinery referred to in Section 3, Paragraph nine of the law On the Application of Taxes in Free Zones and Special Economic Zones is used at several addresses which are located in the territory of one free port or special economic zone, the address where the tank for the storage of labelled (marked) petroleum products is located shall be indicated separately and the addresses where labelled (marked) petroleum products will be used shall be indicated separately in the submission. The following documents shall be appended to the submission: 52.1. a layout of the territory (where the activity takes place) approved by the free port authority or the zone authority; 52.2. a certification regarding the stationary plant, crane and similar objects, equipment that is used in construction works only in the territory of the free zone, machinery that according to its structure is not intended for traffic on public roads and is used only in the territory of the free zone (hereinafter - the equipment and (or) machinery) in which labelled (marked) petroleum products will be used, indicating the following information: 52.2.1. the name, type, model, identification number, and designation of the equipment or machinery to be used by which the equipment or machinery unit is identifiable; 52.2.2. the consumption of labelled (marked) petroleum products (in litres per engine hour) supported by the technical documentation of the equipment or machinery; 52.2.3. the number of engine hours per year which the equipment or machinery is expected to work; 52.2.4. the amount of labelled (marked) petroleum products expected to be consumed by the equipment or machinery per year; 52.2.5. the total amount (in litres) of labelled (marked) petroleum products to be used by the equipment or machinery; 52.3. the technical documentation of the equipment or machinery to be used that supports the accuracy of the information referred to in Sub-paragraph 52.2 of this Regulation; 52.4. [10 February 2015]; 52.5. if the amount of the labelled (marked) petroleum products to be consumed exceeds 7000 litres per year, documents that certify that the tanks specified in the submission are equipped with a meter that ensures accumulated and permanent accounts of the consumption of labelled (marked) petroleum products to be used; 52.6. a document that certifies the volume of the tanks specified in the submission. [3 November 2009; 10 February 2015; 25 June 2019] 52.1 If the submission referred to in Paragraph 52 of this Regulation is submitted in order to obtain the statement for the purchase of marked (labelled) petroleum products (for use in free ports and special economic zones in accordance with Section 3, Paragraph nine of the law On the Application of Taxes in Free Ports and Special Economic Zones) repeatedly, only the documents referred to in Paragraph 52 of this Regulation in which the information has changed shall be attached to the submission. [25 June 2019] 53. The user shall store labelled (marked) petroleum products only on the sites and in the tanks specified in the statement and shall move these only in the cases referred to in Paragraphs 72 and 123 of this Regulation. [17 June 2009; 3 November 2009; 21 December 2021] 54. [10 February 2015] 55. Natural persons shall calculate the amount of labelled (marked) petroleum products required for heating for the time period of one year by using one of the following methods: 55.1. the first method: 55.1.1. calculate the amount of labelled (marked) petroleum products for heating (B1) by using the following formula:

q - the consumption of heat energy (kWh/m2 per year) provided for in a project for buildings that have a heat supply project or 139 kWh/m2 per year for buildings that do not have a heat supply project (assumed annual rate of heat consumption); F - the area of the premises to be heated (m2); Qzd - the lowest combustion heat of labelled (marked) petroleum products 41 160-42 840 kJ/kg; ƞ - the efficiency factor of the heating plant; p - the density of labelled (marked) petroleum products 0.85 kg/l); 55.1.2. calculate the amount of labelled (marked) petroleum products for the supply of hot water (B2) by using the following formula:

n - the number of the consumers of hot water; qn - 0.1 m3 of water every 24 hours per resident; cv - the amount of heat required to heat 1 m3 of water by 1 °C, 4200 kJ/(m3 x °C); tk - the normative temperature of hot water 50 °C; ta.vid. - the average annual normative temperature of cold water 10 °C; Qzd - the lowest combustion heat of labelled (marked) petroleum products 41 160-42 840 kJ/kg; ƞ - the efficiency factor of the heating plant; p - the density of labelled (marked) petroleum products 0.85 kg/l); 55.1.3. calculate the total amount of labelled (marked) petroleum products by using the following formula: B = B1 + B2; 55.1. the second method: 55.2.1. calculate the amount of labelled (marked) petroleum products for heating (Bapk) by using the following formula:

Vā - the external volume of the part of a building to be heated (m3); qa - the number of specific heat consumption for heating 1.764 kJ/m3 °C; a - correction factor 1.1-1.25; tiekš. - the average calculated indoor temperature of premises - plus 20 °C; tārg. - calculated outdoor air temperature - minus 20 °C; kt - the average temperature factor in the heating season 0.51; N - the number of days in the heating season (210 days); n - duration of heating (hours) every 24 hours; Qzd - the lowest combustion heat of labelled (marked) petroleum products 41 160-42 840 kJ/kg; ƞ - the efficiency factor of the heating plant; p - the density of labelled (marked) petroleum products 0.85 kg/l); 55.2.2. calculate the amount of labelled (marked) petroleum products for the supply of hot water (Bk.ūd.) by using the following formula:

n - the number of the consumers of hot water; qn - 0.1 m3 of water every 24 hours per resident; cv - the amount of heat required to heat 1 m3 of water by 1 °C, 4200 kJ/(m3 x °C); tk - the normative temperature of hot water 50 °C; ta.vid. - the average annual normative temperature of cold water 10 °C; Qzd - the lowest combustion heat of labelled (marked) petroleum products 41 160-42 840 kJ/kg; ƞ - the efficiency factor of the heating plant; p - the density of labelled (marked) petroleum products 0.85 kg/l); 55.2.3. calculate the total amount of labelled (marked) petroleum products by using the following formula: B = Bapk. +B k.ūd. [21 December 2021] 56. If the user is not a natural person, the labelled (marked) petroleum products required for the production of heat for heating, in combustion plants, or for the production of heat energy in the technological process of product manufacturing (processing) shall be calculated for the time period of one year by using one of the following methods and by multiplying the obtained result by a predicted capacity factor ranging from 0.1 to 0.9 (depending on the intensity of use and the technical capabilities of the equipment): 56.1. according to the rated output of the equipment: