|

Finance

and Capital Market Commission

Regulatory Provisions No. 1

Adopted 3 January 2019

|

Regulatory

Provisions for the Money Laundering and Terrorism Financing Risk

Management

Issued pursuant

to

Section 34.2, Paragraph four of the Credit Institution

Law, and Section 37.1

and Section 47, Paragraph

two, Clauses 1, 2 and 7 of the Law on the Prevention

of Money Laundering and Terrorism Financing

I. General

Provisions

1. Regulatory Provisions for the Money Laundering and

Terrorism Financing Risk Management (hereinafter - the

Provisions) prescribe the minimum requirements for the money

laundering and terrorism financing (hereinafter - the ML/TF) risk

management which shall be binding on the credit institutions

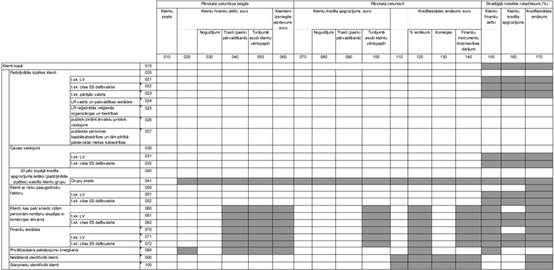

registered in the Republic of Latvia (hereinafter - the credit

institution). Credit institutions shall comply with the

requirements of these Provisions individually and at the level of

consolidation group or consolidation sub-group by ensuring the

ML/TF risk management consistent with the requirements of these

Provisions in the consolidation group or sub-group,and also in

any subsidiary.

2. The following terms are used in these Provisions:

2.1. ML/TF risk - impact and likelihood that the credit

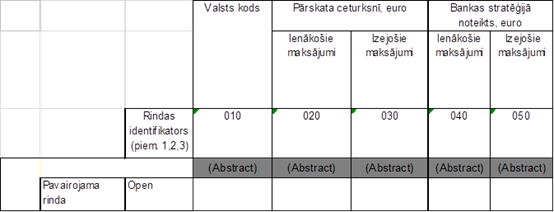

institution may be used for money laundering or terrorism

financing;

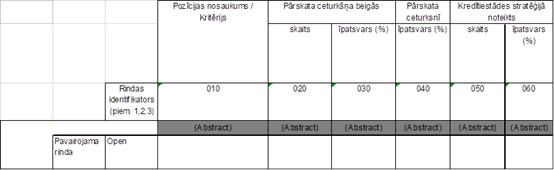

2.2. private banking services - financial services provided by

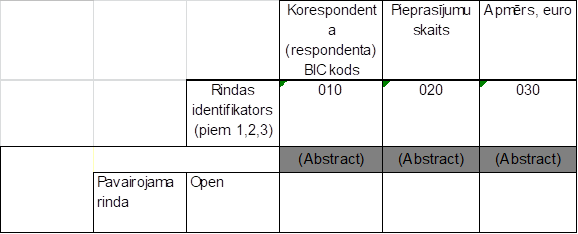

the credit institution to a customer by meeting both of the

following conditions:

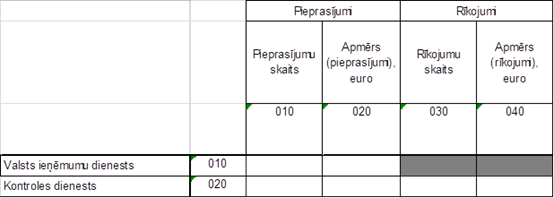

2.2.1. the total planned or actual annual credit turnover of

the customer exceeds EUR 1 000 000. If the customer has several

accounts opened with the credit institution, then the total

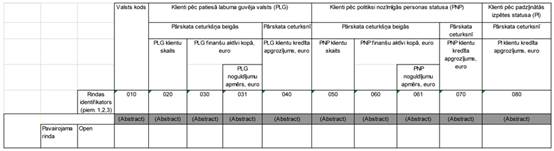

credit turnover shall be calculated by aggregating the credit

turnover of funds in all accounts;

2.2.2. the credit institution shall provide the customer with

special services, such as advice on financial planning,

investment, tax and inheritance issues, or special service

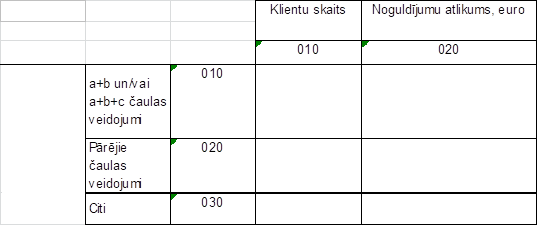

provision rules or service procedures, e.g. an employee

individually assigned to a customer who has the right to decide

on the increase of the restrictions imposed on the customer and

who is the only channel of communication between the customer and

credit institution, or special communication procedures have been

laid down, or provisions for the confidentiality of customer data

have been increased;

2.3. ML/TF risk exposure - impact of the ML/TF risk to which

the credit institution is exposed, considering the ML/FT risk

inherent to its customers, products and services, their delivery

channels and geographical scope of credit institution's

activities;

2.4. ML/TF risk management strategy - a document in which the

credit institution specifies the ML/TF risk exposure that it

deems possible to be assumed, considering its operational

development strategy and capacity to manage the ML/TF risk, and

also lays down the requirements by which the credit institution

shall ensure that the maximum thresholds of the ML/TF risk

exposure indicators specified thereby are not exceeded and the

ML/TF risk management;

2.5. financial assets - value of the monetary funds (deposits)

of a customer which have been transferred for storage into an

account of the credit institution for a definite or indefinite

time period with or without interest, fiduciary operations

(trusts (liabilities under management)), portfolios of customer's

financial instruments that are held at the credit institution,

including portfolios of financial instruments which have been

transferred to the credit institution for management, and also

any other financial assets (such as gold etc.);

2.6. income - the total actual income of the credit

institution in the reference quarter, including the

following:

2.6.1. the interest income received in the reference quarter

in accordance with template F02.00, row No. 010 of the Regulatory

Provisions No. 119 of 6 July 2016 of the Finance and Capital

Market Commission, Regulatory Provisions for the Drawing up of

Supervisory Financial Reports (hereinafter - the FINREP);

2.6.2. the income from the commission received in the

reference quarter in accordance with template F02.00, row No. 200

of the FINREP;

2.6.3. the profit and loss on transactions of trade in

financial instruments in the reference quarter in accordance with

template F02.00, aggregate of rows No. 220, No. 280, No. 287, No.

290 and No. 300 of the FINREP;

2.6.4. other income not specified in Paragraphs 2.6.1-2.6.3 of

these Provisions.

3. Within the framework of its internal control system, the

credit institution shall undertake the ML/TF risk assessment ,

and establish, maintain and develop a specific section for the

ML/TF risk management in the internal control system which

corresponds to its economic activity in accordance with the

requirements laid down in the Law on the Prevention of Money

Laundering and Terrorism Financing and its subordinate laws and

regulations.

4. Before introducing a new financial service or providing a

financial service to a new target audience of customers, the

credit institution shall assess the ML/TF risk inherent to such

services, customers and countries related thereto, and impact

thereof on the the capital necessary for covering the risk

associated with the credit institution. The credit institution

shall assess the need to develop new policies and procedures for

the ML/TF risk management of these financial services or to make

amendments to the existing policies and procedures.

5. The credit institution shall, on a regular basis, assess

and ensure elimination of the deficiencies established in the

internal control system for the ML/TF risk management in

operation of the existing financial services, including with

regard to the financial services the provisions of which are

being significantly changed.

II. The ML/TF

Risk Management and Internal Control System for the ML/TF Risk

Management

6. The internal control system for the ML/TF risk management

of the credit institution shall include at least the

following:

6.1. the ML/TF risk management strategy of the credit

institution, including objectives of the ML/TF risk management

strategy;

6.2. the policies and procedures for the implementation of the

ML/TF risk management strategy, including the structure and

operational organisation of the ML/TF risk management, allocation

of the responsibilities and authorisation of the management and

employees in the area of ML/TF risk management, identification

and management of the ML/TF risk,including the measuring,

assessment, control, drawing up and submission of reports to the

management of the credit institution, recording and documentation

of customer information and transactions, requirements for the

independence of the remuneration system of employees engaged in

the ML/TF risk management from the results of the economic

activity of the credit institution, and also the the staff

resources and professional qualification required for the ML/TF

risk management;

6.3. the requirements for regular review of policies and

procedures in accordance with changes in laws and regulations or

operational processes of the credit institution, services

provided thereby, governance structure, customer base or regions

of activity;

6.4. the procedures for assessing (measuring) and maintaining

the capital needed to cover the ML/TF risks. Structure of the

capital needed to cover the ML/TF risks shall correspond to the

provisions of the Regulatory Provisions No. 199 of 29 November

2016 of the Finance and Capital Market Commission, Regulatory

Provisions for the Establishment of Process of Assessment of

Capital and Liquidity Adequacy;

6.5. the requirements for the provision of information

technologies (hereinafter - the IT) necessary for the ML/TF risk

management;

6.6. the requirements for undertaking a regular (at least

every 18 calendar months) assessment of the internal control

system for the ML/TF risk management by an independent external

auditor, stipulating the scope, procedures, objectives and

deadlines of the review of operation of the internal control

system for the ML/TF risk management, and also requirements for

the selection of an independent external auditor;

6.7. the requirements for regular review, efficiency

evaluation and improvement of the internal control system for the

ML/TF risk management by taking into account changes in activity

of the credit institution and external circumstances affecting

risks and activity of the credit institution;

6.8. the requirements for development of the ML/TF risk

exposure indicators and their maximum thresholds;

6.9. regular evaluation of the collection and assessment of

the ML/TF risk exposure indicators, and of their development

dynamics, and also taking of appropriate decisions in accordance

with the ML/TF risk management strategy of the credit

institution, and the requirements of the policies and procedures

for its implementation;

6.10. the requirements for carrying out the ML/TF risk stress

tests;

6.11. the methods (such as imposition of appropriate

restrictions etc.) for the ML/TF risk management of the credit

institution in compliance with the identified objectives of the

ML/TF risk management strategy.

7. The credit institution shall ensure continuous ML/TF risk

management for the entirety of its activities by taking into

account its interaction with other risks inherent to the activity

of the credit institution.

8. The credit institution shall ensure complete implementation

of all ML/TF risk management measures with regard to all

customers, including the customers who are persons associated

with the credit institution.

III. The ML/TF

Risk Management Strategy

9. The credit institution shall specify in the ML/TF risk

management strategy the maximum permissible thresholds for the

ML/TF risk exposure indicators which the credit institution is

willing to assume and is capable of managing by defining the

ML/TF risk exposure indicators and ML/TF risk-mitigating measures

in accordance with the requirements of Paragraph 10 of these

Provisions.

10. The credit institution shall develop the ML/TF risk

management strategy in accordance with the ML/TF risk inherent to

the activity of the credit institution. The credit institution

shall specify at least the following in the strategy:

10.1. the ML/TF risk exposure indicators of the credit

institution by including at least the following indicators:

10.1.1. the ML/TF risk exposure indicators inherent to the

customer base of the credit institution and their maximum

permissible thresholds up to which the internal control system

for the ML/TF risk management of the credit institution is

capable of ensuring the ML/TF risk management in accordance with

the requirements of laws and regulations, including the

following:

10.1.1.1. the proportion of the financial assets and credit

turnover of all customers that are subject to the enhanced due

diligence in accordance with Paragraphs 40, 41, 42 and 43 of the

Regulatory Provisions No. 3 of the Finance and Capital Market

Commission of 9 January 2018, Regulatory Provisions for Credit

Institutions and Licensed Payment and Electronic Money

Institutions Regarding Enhanced Customer Due Diligence

(hereinafter - Regulatory Provisions No. 3), and also of the

customers who were subject to the enhanced due diligence during

the reference period due to the ML/TF risk which was identified

upon the establishment of a business relationship and during the

business relationship, and which was present during the reference

period (hereinafter jointly - the customers subject to the

enhanced due diligence), in the total amount of financial assets

and credit turnover of credit institutionʼs customers by

separately identifying the maximum permissible thresholds for 1)

the State and local government institutions of the Republic of

Latvia; 2) associations and religious organisations registered in

the Republic of Latvia; 3) legal persons and legal arrangements

referred to in Paragraph 24.4 of Regulatory Provisions No. 3

whose main activity is not associated with the Republic of

Latvia, but which belong to a group of foreign undertakings with

good reputation known to the general public; and 4) capital

companies of a public person and subsidiaries completely owned by

them;

10.1.1.2. the proportion of the income from the customers

subject to the enhanced due diligence in the total amount of

income of the credit institution by separately identifying the

maximum permissible thresholds for 1) the State and local

government institutions of the Republic of Latvia; 2)

associations and religious organisations registered in the

Republic of Latvia; 3) legal persons and legal arrangements

referred to in Paragraph 24.4 of Regulatory Provisions No. 3

whose main activity is not associated with the Republic of

Latvia, but which belong to a group of foreign undertakings with

good reputation known to the general public; and 4) capital

companies of a public person and subsidiaries completely owned by

them;

10.1.1.3. the proportion of financial assets and credit

turnover of the customers who are shell arrangements in the total

amount of financial assets and credit turnover of credit

institutionʼs customers;

10.1.1.4. the proportion of income from the services which

have been provided to the customers who are shell arrangements in

the total amount of income of the credit institution;

10.1.1.5. the proportion of financial assets and credit

turnover of the 20 largest groups of associated customers of the

credit institution subject to the enhanced due diligence in terms

of credit turnover in the total amount of financial assets and

credit turnover of the credit institutionʼs customers subject to

the enhanced due diligence;

10.1.1.6. the proportion of income from the services which

have been provided to the 20 largest groups of associated

customers of the credit institution subject to the enhanced due

diligence in terms of the total credit turnover in the total

amount of income of the credit institution;

10.1.1.7. the proportion of financial assets and credit

turnover of the customers for the beneficial owner of which the

country of residence corresponds to any risk increasing factors

referred to in Paragraph 31 of Regulatory Provisions No. 3 in the

total amount of financial assets and credit turnover of credit

institutionʼs customers;

10.1.1.8. the proportion of the amount of credit turnover of

the customers that are a credit institution within the meaning of

the Law on the Prevention of Money Laundering and Terrorism

Financing in the total amount of credit turnover of transactions

of the customers of credit institutionʼs customers;

10.1.2. the proportions of the ML/TF risk exposure indicators

inherent to the services and products of the credit institution

regarding the proportion of amount of credit turnover and income

obtained from transactions conducted within the scope of

provision of private banking services in the total amount of

credit turnover of transactions of the customers of the credit

institution and of income of the credit institution;

10.1.3. the ML/TF risk exposure indicators inherent in

delivery channel of services and products of the credit

institution, including the following:

10.1.3.1. the proportion of financial assets and credit

turnover of the customers who have been identified remotely (a

customer has not participated in the identification in person) in

the total amount of financial assets and credit turnover of the

customers;

10.1.3.2. the proportion of financial assets and credit

turnover of the customers who have been identified through third

parties (agents, intermediaries) in the total amount of financial

assets and credit turnover of the customers;

10.1.3.3. the proportion of amount of credit turnover of the

transactions conducted by using service delivery channels with an

increased ML/TF risk (customers who themselves provide settlement

possibilities to other persons within the scope of e-commerce) in

the total amount of credit turnover of transactions of the

customers of the credit institution;

10.1.4. the ML/TF risk exposure indicators inherent to the

correspondent relationship of the credit institution regarding

turnover of incoming and outgoing payments of loro correspondents

(respondents) of the credit institution split by countries of

registration of loro correspondents (respondents) that correspond

to any of the groups of countries with inherent ML/TF risk

increasing factors in compliance with the requirements laid down

in Regulatory Provisions No. 3;

10.2. with regard to each of the ML/TF risk exposure

indicators of the credit institution specified in Paragraph 10.1

of these Provisions the credit institution shall, in line with

the objectives identified in the operational development

strategy, determine the maximum permissible thresholds for a

period, which is at least one calendar year, in the ML/TF risk

management strategy and comply with them;

10.3. the conditions limiting the ML/TF risk;

10.4. the envisaged ML/TF risk-mitigation methods;

10.5. the criteria for the adequacy of resources and

competence requirements for employees of structural units of the

internal control system for the ML/TF risk management the duties

of which include ML/TF risk control;

10.6. the principles for the establishment of the system for

staff authorisation with regard to the decisions affecting the

ML/TF risk exposure of the credit institution;

10.7. the principles for assessment of adequacy of the IT

provision necessary for the fulfilment of the ML/TF risk

management functions, as well as the procedures for independent

testing of IT systems which ensure the ML/TF risk control

function;

10.8. the principles for using information available to the

general public and from data bases for the purposes of

understanding economic activity of the customer;

10.9. the requirements for the evaluation of the ML/TF risk

management efficiency, including the following:

10.9.1. the requirements for an independent assessment of

operation of the internal control system for the ML/TF risk

management;

10.9.2. the requirements for the provision of information

regarding compliance with the requirements for the ML/TF risk

management strategy to the management of the credit

institution;

10.9.3. the requirements for informing the management of the

credit institution of any deviations from the approved ML/TF risk

management strategy and the policies and procedures for its

implementation.

11. The maximum permissible thresholds of the ML/TF risk

exposure indicators shall be determined by taking into account

the capacity of the credit institution to manage the ML/TF risk

associated with the nature of the existing and expected economic

activity of the credit institution, as well as the resources

available for the ML/TF risk management.

12. When determining credit turnover in the customer's

account, the credit institution shall include all incoming

payments therein. If according to the requirements laid down in

the policies and procedures of the credit institution all

transactions of the customer (including those with the credit

institution) are conducted by only using a current account of the

customer with the credit institution, then the credit institution

shall not include therein any payments made between different

accounts of this customer with this credit institution when

determining credit turnover in the customer's account.

13. The credit institution shall submit the ML/TF risk

management strategy to the Finance and Capital Market Commission

within one month after approval thereof by the council of the

credit institution.

14. The board of directors of the credit institution shall, on

a regular basis, assess whether the actual determined threshold

of or requirements for the ML/TF risk exposure indicators have

not been exceeded, as well as the reasons and grounds for it, if

the exceedance of thresholds of or requirements for the ML/TF

risk exposure indicators has been established. In the case of

significant deviations (the determined threshold has been

exceeded by 10 per cent) the credit institution shall each time,

concurrently with the report on the characterisation of the ML/TF

risk exposure of the credit institution in the previous quarter

referred to in Paragraph 19 of these Provisions, submit a report

to the Finance and Capital Market Commission.

IV.

Responsibility of Officials and Employees of the Credit

Institution

15. The council of the credit institution shall supervise how

the board of directors ensures the ML/TF risk management, and it

shall carry out at least the following activities:

15.1. approve the ML/TF risk management strategy and changes

in the ML/TF risk management strategy;

15.2. approve the policies for the implementation of the ML/TF

risk management strategy;

15.3. supervise and control how the board of directors of the

credit institution manages the ML/TF risk inherent to the

activity of the credit institution and whether this activity is

carried out in accordance with the ML/TF risk management

strategy;

15.4. determine that the internal audit body examines and

assesses on a regular basis the compliance of activity of the

credit institution with the ML/TF risk management strategy and

the policies and procedures for its implementation, and informs

the council of the examination results;

15.5. lay down routine and non-routine procedures for

information exchange between the council and the board of

directors. The council shall establish that at least once a

quarter it receives a report on the ML/TF risk management which

contains information regarding the achievement of the objectives

identified in the ML/TF risk management strategy;

15.6. determine the remuneration policy of the credit

institution which is not in contradiction with its ML/TF risk

management strategy and does not facilitate generation of

short-term income when conducting transactions which have or pose

an increased ML/TF risk, as well as determine that remuneration

of employees of structural units of the internal control system

whose duties include the ML/TF risk control does not depend on

indicators of economic activity of the credit institution;

15.7. on a regular basis, but at least once a year, on the

basis of financial results of activity and performance plans of

the credit institution and taking into account changes in laws

and regulations, economic situation, markets and market

development forecasts, as well as introduction of new financial

services, review the ML/TF risk management strategy and its

implementation policies, and assess adequacy of equity of the

credit institution to cover risks of the credit institution which

it has assumed or will assume.

16. The board of directors of the credit institution shall be

responsible for the implementation of the ML/TF risk management

strategy approved by the council of the credit institution and

the ML/TF risk management, and it shall carry out at least the

following activities:

16.1. ensure regular revision and updating of the ML/TF risk

assessment, as well as evaluation of the operating efficiency of

the internal control system in accordance with the requirements

laid down in Section 8, Paragraphs one and two of the Law on the

Prevention of Money Laundering and Terrorism Financing;

16.2. ensure the development of and compliance with the

policies and procedures for the implementation of the ML/TF risk

management strategy;

16.3. ensure the achievement of the objectives specified in

the ML/TF risk management strategy of the credit institution and

application of policies and procedures for the implementation of

the ML/TF risk management strategy to all structural units of the

credit institution in the Republic of Latvia and other

countries;

16.4. determine division of powers, duties and

responsibilities regarding the ML/TF risk management among

structural units and employees of the credit institution;

16.5. ensure that the employees of structural units of the

internal control system for the ML/TF risk management whose

duties include the ML/TF risk control are informed of the ML/TF

risk management strategy and the policies and procedures for its

implementation, and responsibility for the compliance with the

ML/TF risk management strategy of the credit institution and the

policies and procedures for its implementation;

16.6. ensure that employees whose qualification conforms to

the duties to be performed are engaged in the area of the ML/TF

risk management;

16.7. ensure that during performance of the ML/TF risk

management high ethical standards are maintained at all times,

including prevention of conflicts of interests which increase or

may increase the ML/TF risk, for example, when providing services

to the persons associated with the credit institution;

16.8. after analysis of results of the ML/TF risk stress tests

approve the corrective measures for the ML/TF risk management in

cases when they are necessary, and ensure development of changes

in the ML/TF risk management strategy. Changes in the ML/TF risk

management strategy shall be submitted to the council of the

credit institution for approval.

17. When determining the member of the board of directors who

shall supervise the area of the ML/TF prevention in the credit

institution and assigning one or several employees to be

responsible for the compliance with the requirements for the

ML/TF prevention in accordance with Section 10, Paragraphs one

and two of the Law on the Prevention of Money Laundering and

Terrorism Financing, the credit institution shall determine in

its internal regulatory enactments the division of their

responsibility by envisaging division of responsibility for at

least the following issues:

17.1. the routine and extraordinary informing of the council

and board of directors of the credit institution of the

compliance with the requirements for the ML/TF risk management

strategy of the credit institution, including by providing

accurate and complete information regarding the ML/TF risk

exposure and dynamics thereof;

17.2. the suitability and adequacy of the ML/TF risk

management measures, and duly provision of the changes necessary

for the ML/TF risk management;

17.3. the provision of reports to the board of directors on

all cases when deviations from the approved ML/TF risk management

strategy and the policies and procedures for its implementation

have been established in the course of the ML/TF risk

management.

V. Supervision

of the ML/FT Risk Exposure

18. The credit institution shall lay down the procedures for

gathering and assessing the ML/TF risk exposure indicators,

including the following:

18.1. the sources of information;

18.2. the procedures for acquiring and assessing

information;

18.3. the employees of the credit institution who are entitled

to prepare, assess and verify the information characterising the

ML/TF risk exposure;

18.4. the procedures for providing information regarding the

ML/TF risk exposure indicators to the board of directors and

council of the credit institution and the scope of this

information, as well as the requirements for providing reports on

exceeding the thresholds specified in the ML/TF risk management

strategy or exceeding the potentials;

18.5. the employee who provides the information referred to in

Paragraphs 19 and 49 and the report referred to in Paragraph 14

of these Provisions to the Finance and Capital Market Commission

by using the Data Reporting System of the Finance and Capital

Market Commission.

19. The credit institution shall, by the last date of the

first month of each calendar quarter, submit to the Finance and

Capital Market Commission a report on the characterisation of the

ML/TF risk exposure of the credit institution in the prior

quarter in accordance with Annexes to these Provisions

electronically in an XML (Extensive Markup Language) file format

according to the XSD (XML Schema Definition) schema prepared by

the Finance and Capital Market Commission.

20. The credit institution shall fill in the report on the

characterisation of the ML/TF risk exposure of the credit

institution in the prior quarter referred to in Paragraph 19 of

these Provisions by using the following forms annexed to these

Provisions as Annexes 1-3:

20.1. M 11.00 Characterisation of the Money Laundering and

Terrorism Financing Risk Exposure (hereinafter - Annex 1);

20.2. M 12.00 Amount of Turnover of Payments of Loro

Correspondents (Respondents) of the Credit Institution Split by

Countries of Registration of Loro Correspondents (Respondents)

(hereinafter - Annex 2);

20.3. M 13.00 Indicators Individually Defined by the Credit

Institution (hereinafter - Annex 3).

21. The credit institution shall, concurrently with the

filling-in of the forms of Annexes referred to in Paragraph 20 of

these Provisions, fill in the forms annexed to these Provisions

as Annexes 4-7 and include therein the actual indicators for the

reference period:

21.1. M 14.00 Number of Requests from Correspondent Credit

Institutions with which the Credit Institution has Opened a

Nostro Account (Correspondent Account), and Amount of Funds of

Transactions Referred to Within the Scope of Requests

(hereinafter - Annex 4);

21.2. M 15.00 Number of Requests/Orders of the State Revenue

Service and the Control Service and Amount of Transactions

Referred to Within the Scope Thereof (hereinafter - Annex 5);

21.3. M 16.00 Characterisation of Transactions of Customers by

Countries (hereinafter - Annex 6);

21.4. M 17.00 Customers with whom the Credit Institution has

Decided (after the ML/TF risk assessment) to Terminate the

Business Relationship, and the Balance of Their Deposits

(hereinafter - Annex 7).

22. The coloured fields in Annexes 1 and 5 to these Provisions

shall not be completed.

Procedures for the Filling in of

Annex 1

23. When providing the report on the characterisation of the

ML/TF risk exposure of the credit institution in the prior

quarter referred to in Paragraph 19 of these Provisions to the

Finance and Capital Market Commission at an individual level (a

credit institution registered in the Republic of Latvia shall not

include data on its branches in a Member State or a third

country), the credit institution shall fill in Annex 1 which

consists of the following three main reporting groups:

23.1. the indicators the actual amount of which is indicated

for the situation at the end of the reference quarter (on the

last day), column No. 010-060 with the collective title of the

group "At the end of the reference quarter";

23.2. the indicators the actual amount of which is indicated

for the reference quarter, column No. 070-140 with the collective

title of the group "In the reference quarter";

23.3. the thresholds determined in the ML/TF risk management

strategy of the credit institution for the reference year - the

proportion of the ML/TF risk exposure indicators, column No.

150-170 with the collective title of the group "Thresholds

determined in the strategy (%)".

24. Upon filling in row No. 010 with the title "Customers in

total" in Annex 1, the credit institution shall indicate the

following data in columns:

24.1. the actual data on the situation at the end of the

reference quarter (on the last day) for the total number of all

customers in column No. 010 with the title "Number of customers"

in accordance with Annex 1 to the Regulatory Provisions No. 271

of the Finance and Capital Market Commission of 12 November 2014,

Regulatory Provisions for the Preparation of Information

regarding Amount of Daily Deposits and Number of Customers, item

code No. 050 - column with the title "Number of customers",

sub-column with the title "Total";

24.2. the actual data on the situation at the end of the

reference quarter (on the last day) for the total amount of all

financial assets of customers shall be indicated in column No.

020 with the title "Financial assets of customers, EUR",

including also the data on other financial assets not indicated

in column No. 030-050;

24.3. the actual data on the situation at the end of the

reference quarter (on the last day) for the deposits of all

customers shall be indicated in column No. 030 with the title

"Deposits" in accordance with total sum of rows No. 090, No. 110,

No. 120 and No. 130 of the FINREP template F20.06;

24.4. the actual data on the situation at the end of the

reference quarter (on the last day) for the fiduciary operations

(trusts (liabilities under management)) of all customers shall be

indicated in column No. 040 with the title "Trusts (liabilities

under management)" in accordance with the total sum of rows No.

010 and No. 110 of the FINREP template F22.02;

24.5. the actual data on the situation at the end of the

reference quarter (on the last day) with regard to the securities

of customers held by all customers shall be indicated in column

No. 050 with the title "Customers' Securities under Custody", in

accordance with column 13 with the title "Total amount of

securities (EUR)" of Annex 1 to the Regulation No. 163 of

Latvijas Banka of 15 March 2018, Regulations for Compiling

Reports on Securities;

24.6. the actual data on the situation at the end of the

reference quarter (on the last day) for the amount of loans

granted to all customers shall be indicated in column No. 060

with the title "Loans granted to customers, EUR" in accordance

with the column No. 10 and rows No. 090, No. 110, No. 120 and No.

150 of the FINREP template F18.00.a;

24.7. the data on the total actual credit turnover of all

customers in the reference quarter shall be indicated in group of

columns No. 070-100 with the collective title of the group "In

the reference quarter", including the credit turnover in current

accounts of customers (deposits), fiduciary operation accounts

(trusts (liabilities under management)) of customers, and

securities accounts held by the customers;

24.8. the data on the actual total income of the credit

institution in the reference quarter shall be indicated in the

group of columns No. 110-140 with the collective title of the

group "In the reference quarter", in accordance with the scope of

the income specified in Paragraph 2.6 of these Provisions.

25. Upon filling in row No. 020 with the title "Customers

subject to the enhanced due diligence" and row No. 030 with the

title "Shell arrangements" in Annex 1, the credit institution

shall indicate the following data in columns:

25.1. the actual data on the situation at the end of the

reference quarter (on the last day) with regard to the total

number of all customers subject to the enhanced due diligence and

shell arrangements, amount of the total financial assets thereof

(listing them in the relevant columns by deposits, fiduciary

operations (trusts (liabilities under management)) and customers'

securities under custody), and amount of the loans granted

thereto shall be indicated in the group of columns No. 010-060

with the collective title of the group "At the end of the

reference quarter" by dividing this information in sub-rows by

countries of registration of customers according to the

provisions of the titles of sub-rows No. 021-023 and No. 031-032,

as well by separating in sub-row No. 024-027 categories of the

customers subject to the enhanced due diligence which include 1)

the State and local government institutions of the Republic of

Latvia; 2) associations and religious organisations registered in

the Republic of Latvia; 3) legal persons and legal arrangements

referred to in Paragraph 24.4 of the Regulatory Provisions No. 3

the main activity of which is not associated with the Republic of

Latvia, but which belong to a group of foreign undertakings with

good reputation known to the general public; and 4) capital

companies of a public person and subsidiaries completely owned by

them;

25.2. the actual data on the total actual credit turnover of

all customers subject to the enhanced due diligence and shell

arrangements, including credit turnover in current accounts of

customers (deposits), accounts of fiduciary operations of

customers (trusts (liabilities under management)) and securities

accounts held by customers, and on the actual income of the

credit institution from servicing such customers shall be

indicated in the group of columns No. 070-140 with the collective

title of the group "In the reference quarter" (dividing them in

the relevant columns by received interest income, received

commissions and profit or loss on transactions of trade in

financial instruments) by dividing information in the relevant

sub-rows by countries of registration of customers according to

the provision of the titles of sub-rows No. 021-023 and No.

031-032, as well as by separating in sub-row No. 024-027

categories of the customers subject to the enhanced due diligence

which include 1) the State and local government institutions of

the Republic of Latvia; 2) associations and religious

organisations registered in the Republic of Latvia; 3) legal

persons and legal arrangements referred to in Paragraph 24.4 of

Regulatory Provisions No. 3 the main activity of which is not

associated with the Republic of Latvia, but which belong to a

group of foreign undertakings with good reputation known to the

general public; and 4) capital companies of a public person and

subsidiaries completely owned by them;

25.3. the proportion of financial assets of all customers

subject to the enhanced due diligence, including 1) the State and

local government institutions of the Republic of Latvia; 2)

associations and religious organisations registered in the

Republic of Latvia; 3) legal persons and legal arrangements

referred to in Paragraph 24.4 of Regulatory Provisions No. 3 the

main activity of which is not associated with the Republic of

Latvia, but which belong to a group of foreign undertakings with

good reputation known to the general public; and 4) capital

companies of a public person and subsidiaries completely owned by

them, specified in the ML/TF risk management strategy of the

credit institution in accordance with Paragraphs

10.1.1.1-10.1.1.4 of these Provisions, and the proportion of

financial assets of shell companies in the total amount of

financial assets of customers, the proportion of credit turnover

of such customers in the total amount of credit turnover of

customers of the credit institution and the proportion of income

of the credit institution obtained from the servicing of such

customers in the total amount of income of the credit institution

expressed as percentage shall be indicated in the relevant

columns of the group of columns No. 150-170 with the collective

title of the group "Thresholds determined in the strategy

(%)".

26. Upon filling in row No. 040 with the title "20 largest

customers of groups of (enhanced due diligence) associated

customers by the total credit turnover" in Annex 1, the credit

institution shall indicate the following data in columns:

26.1. the actual data on the situation at the end of the

reference quarter (on the last day) with regard to the total

number of these groups of associated customers shall be indicated

in the group of columns No. 010-060 with the collective title of

the group "At the end of the reference quarter" by listing

separately the number of groups which constitute these 20 largest

groups of (enhanced due diligence) associated customers by the

total credit turnover, amount of the total financial assets of

all groups of associated customers (dividing them in the relevant

columns by deposits, fiduciary operations (trusts (liabilities

under management)) and customers' securities under custody) and

amount of the loans granted to such customers;

26.2. the actual data on the total actual credit turnover of

groups of associated customers, including credit turnover in

current accounts of customers (deposits), accounts of fiduciary

operations of customers (trusts (liabilities under management))

and securities accounts held by customers, and on the actual

income of the credit institution in the reference quarter shall

be indicated in the group of columns No. 070-140 with the

collective title of the group "In the reference quarter"

(dividing them in the relevant columns by received interest

income, received commissions and profit or loss on transactions

of trade in financial instruments);

26.3. the proportion of financial assets and credit turnover

of customers of the credit institution subject to the enhanced

due diligence specified in the ML/TF risk management strategy of

the credit institution in accordance with Paragraphs

10.1.1.5-10.1.1.6 of these Provisions, in the total amount of

financial assets and credit turnover of customers, the proportion

of credit turnover of such customers in the total amount of

financial assets and credit turnover and the proportion of income

obtained from the services provided to the 20 largest groups of

associated customers of the credit institution subject to

enhanced due diligence by the total credit turnover in the total

amount of income of the credit institution expressed as

percentage shall be indicated in the relevant columns of the

group of columns No. 150-170 with the collective title of the

group "Thresholds determined in the strategy (%)".

27. Upon filling in row No. 050 with the title "Customers with

a risk increasing factor" in Annex 1, the credit institution

shall indicate the following data in columns:

27.1. the actual data on the situation at the end of the

reference quarter (on the last day) with regard to the total

number of customers for the beneficial owners of which the

country of domicile corresponds to any risk increasing factors

referred to in Paragraph 31 of Regulatory Provisions No. 3

(hereinafter in this Paragraph - customers with a risk increasing

factor), and the actual total amount of financial assets shall be

indicated in the group of columns No. 010-060 with the collective

title of the group "At the end of the reference quarter"

(dividing them in the relevant columns by deposits, fiduciary

operations (trusts (liabilities under management)) and customers'

securities under custody) and amount of the loans granted to such

customers by dividing this information in sub-rows by countries

of registration of the customers according to the provision of

the title of sub-row No. 051-052;

27.2. the actual data on the total actual credit turnover of

customers with a risk increasing factor, including credit

turnover in current accounts of customers (deposits), accounts of

fiduciary operations of customers (trusts (liabilities under

management)) and securities accounts held by customers, and on

the actual income of the credit institution from the servicing of

such customers shall be indicated in the group of columns No.

070-140 with the collective title of the group "In the reference

quarter" (dividing them in the relevant columns by received

interest income, received commissions and profit or loss on

transactions of trade in financial instruments) by dividing

information in the relevant sub-rows by countries of registration

of customers according to the provision of the title of sub-row

No. 051-052;

27.3. the proportion of financial assets and credit turnover

of customers with a risk increasing factor specified in the ML/TF

risk management strategy of the credit institution in accordance

with Paragraph 10.1.1.7 of these Provisions in the total amount

of financial assets and credit turnover of customers of the

credit institution expressed as percentage shall be indicated in

the relevant columns of the group of columns No. 150-170 with the

collective title of the group "Thresholds determined in the

strategy (%)".

28. Upon filling in row No. 060 with the title "Customers who

themselves provide settlement possibilities to other persons

within the scope of e-commerce" in Annex 1, the credit

institution shall indicate the following data in columns:

28.1. the actual data on the situation at the end of the

reference quarter (on the last day) with regard to the total

number of customers who conduct transactions by using service

delivery channels with an increased ML/TF risk, and the total

actual amount of financial assets of such customers shall be

indicated in the group of columns No. 010-030 with the collective

title of the group "At the end of the reference quarter", whereas

in column No. 030 these shall be indicated by separating deposits

from the total financial assets of customers and dividing this

information in sub-rows by countries of registration of customers

according to provision of the title of sub-row No. 061-062;

28.2. the actual data on the total actual credit turnover of

such customers shall be indicated in the group of columns No.

070-140 with the collective title of the group "In the reference

quarter", whereas in columns No. 080 and No. 090 these shall be

indicated by separating credit turnover in current accounts of

customers (deposits) and accounts of fiduciary operations of

customers (trusts (liabilities under management)) from the total

turnover of customers, and on the actual income of the credit

institution from servicing such customers, whereas in column No.

130 these shall be indicated by separating the actual amount of

received commissions from the total income of the credit

institution from the servicing of such customers and dividing

this information in sub-rows by countries of registration of

customers according to the provision of the title of sub-row No.

061-062;

28.3. column No. 160 of column group No. 150-170 under the

common title of the group "Thresholds determined in the strategy

(%)" includes the proportion of credit turnover of customers of

the credit institution who conduct transactions by using service

delivery channels with an increased ML/TF risk (customers who

themselves provide settlement possibilities to other persons

within the scope of e-commerce) specified in the ML/TF risk

management strategy of the credit institution in accordance with

Paragraph 10.1.3.3 of these Provisions in the total amount of

credit turnover of transactions of customers of the credit

institution.

29. Upon filling in row No. 070 with the title "Financial

institutions" in the Annex 1, the credit institution shall

indicate the following data in columns:

29.1. the actual data on the situation at the end of the

reference quarter (on the last day) with regard to the total

number of customers who are financial institutions, and the total

actual amount of financial assets of such customers shall be

indicated in the group of columns No. 010-030 with the collective

title of the group "At the end of the reference quarter", whereas

in column No. 030 these shall be indicated by separating deposits

from the total financial assets of customers and dividing this

information in sub-rows by countries of registration of the

customers according to provision of the title of sub-row No.

071-072;

29.2. the actual data on the total actual credit turnover of

such customers shall be indicated in the group of columns No.

070-140 with the collective title of the group "In the reference

quarter", whereas in columns No. 080 and No. 090 these shall be

indicated by separating credit turnover in current accounts of

customers (deposits) and accounts of fiduciary operations of

customers (trusts (liabilities under management)) from the total

turnover of customers, and on the actual income of the credit

institution from servicing such customers, whereas in column No.

130 these shall be indicated by separating the actual amount of

received commissions from the total income of the credit

institution from the servicing of such customers and dividing

this information in sub-rows by countries of registration of the

customers according to the provision of the title of sub-row No.

071-072;

29.3. the proportion of credit turnover of customers who are

the financial institutions specified in the ML/TF risk management

strategy of the credit institution in accordance with Paragraph

10.1.1.8 of these Provisions in the total amount of credit

turnover of customers of the credit institution shall be

indicated in column No. 160 of the group of columns No. 150-170

with the collective title of the group "Thresholds determined in

the strategy (%)".

30. Upon filling in row No. 080 with the title "Provision of

private banking services" in the Annex 1, the credit institution

shall indicate the following data in columns:

30.1. the actual data on the situation at the end of the

reference quarter (on the last day) with regard to the total

number of customers serviced within the scope of the provision of

private banking services shall be indicated in the group of

columns No. 010-030 with the collective title of the group "At

the end of the reference quarter", whereas the amount of deposits

of such customers shall be indicated in column No. 030;

30.2. the actual data on the total actual credit turnover of

customers serviced within the scope of the provision of private

banking services, including credit turnover in current accounts

of customers (deposits), accounts of fiduciary operations of

customers (trusts (liabilities under management)) and securities

accounts held by customers, and on the actual income of the

credit institution from servicing of such customers shall be

indicated in the group of columns No. 070-140 with the collective

title of the group "In the reference quarter", whereas in columns

No. 130 and No. 140 these shall be indicated by separating income

from commissions and profit or loss on transactions of trade in

financial instruments from such income;

30.3. the proportion of credit turnover of transactions

conducted within the scope of the provision of private banking

services specified in the ML/TF risk management strategy of the

credit institution in accordance with Paragraph 10.1.2 of these

Provisions, and the proportion of the obtained income in the

total credit turnover of transactions of customers of the credit

institution and in the total amount of income of the credit

institution shall be indicated in columns No. 160 and 170 of the

group of columns No. 150-170 with the collective title of the

group "Thresholds determined in the strategy (%)".

31. Upon filling in row No. 090 with the title "Remotely

identified customers" and row No. 100 with the title "Customers

identified by intermediaries" in the Annex 1, the credit

institution shall indicate the following data in columns:

31.1. the actual data on the situation at the end of the

reference quarter (on the last day) with regard to the total

number of customers who have been identified remotely (a customer

has not participated in the identification in person)

(hereinafter - the remotely identified customers), and customers

whose identification has been performed through third parties

(agents, intermediaries) (hereinafter - the customers identified

by intermediaries), the total amount of financial assets of the

remotely identified customers and the customers identified by

intermediaries (listing them in the relevant columns by deposits,

fiduciary operations (trusts (liabilities under management)) and

customers' securities under custody), and amount of the loans

granted to the remotely identified customers and the customers

identified through intermediaries shall be indicated in the group

of columns No. 010-060 with the collective title of the group "At

the end of the reference quarter";

31.2. the actual data on the total actual credit turnover of

the remotely identified customers and the customers identified by

intermediaries shall be indicated in the group of columns No.

070-140 with the collective title of the group "In the reference

quarter", including the credit turnover in current accounts of

customers (deposits), fiduciary operation accounts (trusts

(liabilities under management)) of customers, and securities

accounts held by the customers;

31.3. the proportion of financial assets of the remotely

identified customers and the customers identified by

intermediaries specified in the ML/TF risk management strategy of

the credit institution in accordance with Paragraphs 10.1.3.1 and

10.1.3.2 of these Provisions, in the total amount of financial

assets of customers, and the proportion of credit turnover of

such customers in the total amount of credit turnover of

customers of the credit institution shall be indicated in the

relevant columns of the group of columns No. 150-170 with the

collective title of the group "Thresholds determined in the

strategy (%)".

Procedures for the Filling in of

Annex 2

32. When providing the report on the characterisation of the

ML/TF risk exposure of the credit institution in the prior

quarter referred to in Paragraph 19 of these Provisions to the

Finance and Capital Market Commission, the credit institution

shall fill in Annex 2 by indicating the group of countries with

inherent ML/TF risk increasing factors in accordance with the

requirements laid down in Regulatory Provisions No. 3. Annex 2

consists of the following three main reporting groups:

32.1. the code of the relevant country, column No. 010 with

the title "Country code";

32.2. the indicators the actual amount of which must be

indicated with regard to the reference quarter, group of columns

No. 020 and No. 030 with the collective title of the group "In

the reference quarter";

32.3. the thresholds determined in the ML/TF risk management

strategy of the credit institution - the proportion of the ML/TF

risk exposure indicators, group of columns No. 040 and No. 050

with the collective title of the group "Determined in the bank

strategy, EUR".

33. Upon filling in a row in Annex 2, and, where necessary,

copying it and numbering it in sequence in the first column of

each row, the credit institution shall indicate the following

data on loro correspondents (respondents) of the credit

institution in columns:

33.1. the code of the country of registration of the relevant

loro correspondent of the credit institution shall be indicated

in column No. 010 in accordance with the international standard

ISO 3166-1:2013;

33.2. the actual data on the total actual amount of incoming

and outgoing payments of the loro correspondent (respondent) of

the credit institution of the relevant country of registration in

the reference quarter shall be indicated in the group of columns

No. 020 and 030 with the collective title of the group "In the

reference quarter";

33.3. the turnover of incoming and outgoing payments of loro

correspondents (respondents) of the credit institution specified

in the ML/TF risk management strategy of the credit institution

in accordance with Paragraph 10.1.4 of these Provisions split by

countries of registration of loro correspondents (respondents)

that correspond to any of the groups of countries having the

ML/TF risk increasing factors in compliance with the requirements

laid down in Regulatory Provisions No. 3.

Procedures for the Filling in of

Annex 3

34. If the credit institution has individually defined

indicators which are not specified in Paragraph 10 of these

Provisions, the credit institution shall fill in Annex 3 by

copying and numbering rows in sequence in the first column of

each row, if necessary, and indicating the following data in

columns:

34.1. the item designation or criterion, column No. 010 with

the title "Item designation/criterion";

34.2. depending on the defined item designation or criterion -

the number and percentage at the end of the reference quarter,

group of columns No. 020 and No. 030 with the collective title of

the group "At the end of the reference quarter";

34.3. depending on the defined item designation or criterion -

the percentage in the reference quarter, column No. 040 with the

title "In the reference quarter";

34.4. the maximum thresholds determined individually in the

ML/TF risk management strategy of the credit institution

depending on the defined item designation or criterion - the

number and percentage, group of columns No. 050 and No. 060 with

the collective title of the group "Determined in the strategy of

the credit institution".

Procedures for the Filling in of

Annex 4

35. Upon filling in Annex 4, the credit institution shall

provide the actual indicators for the reference period with

regard to the number of requests submitted by each correspondent

credit institution with which the credit institution has opened a

nostro account (correspondent account), and the amount of funds

of transactions referred to within the scope of the requests by

copying and numbering rows in sequence in the first column of

each row, where necessary, and indicate the following data in

columns:

35.1. the identification code of the relevant correspondent in

BIC format in accordance with the international standard ISO

9362:2014, column No. 010 with the title "BIC code of

correspondent (respondent)";

35.2. the number of requests received from the correspondent

in the reference quarter, column No. 020 with the title "Number

of requests";

35.3. the amount of funds of transactions referred to within

the scope of the requests, column No. 030 with the title "Amount,

EUR".

36. Upon filling in column No. 010 with the title "BIC code of

correspondent (respondent)" in Annex 4, the credit institution

shall indicate only the identification code of the correspondent

consisting of 8 or 11 symbols in BIC format in accordance with

the international standard ISO 9362:2014.

Procedures for the Filling in of

Annex 5

37. The credit institution shall fill in Annex 5 by indicating

the number of requests/orders from the State Revenue Service and

the Office for Prevention of Laundering of Proceeds Derived from

Criminal Activity on unusual or suspicious transactions, and the

amount of funds of transactions referred to within the scope of

requests/orders. Annex 5 consists of the following two main

reporting groups:

37.1. the number of requests and the amount of funds of

transactions referred to within the scope of requests, group of

columns No. 010 and No. 020 with the collective title of the

group "Requests";

37.2. the number of orders regarding freezing of funds and the

amount of funds to be frozen referred to within the scope of

orders, group of columns No. 030 and No. 040 with the collective

title of the group "Orders".

38. Upon filling in row No. 010 with the title "State Revenue

Service", group of columns No. 010 and No. 020 with the

collective title of the group "Requests" in Annex 5, the credit

institution shall indicate the number of requests received from

the State Revenue Service on unusual or suspicious transactions,

and the amount of funds of transactions referred to within the

scope of requests.

39. Upon filling in row No. 020 with the title "Control

Office" in Annex 5, the credit institution shall indicate the

following data in columns:

39.1. the number of requests received from the Office for

Prevention of Laundering of Proceeds Derived from Criminal

Activity on unusual or suspicious transactions, and the amount of

funds of transactions referred to within the scope of requests

shall be indicated in the group of columns No. 010 and No. 020

with the collective title of the group "Requests";

39.2. the number of orders received from the Office for

Prevention of Laundering of Proceeds Derived from Criminal

Activity on the freezing of funds, and the amount of funds to be

frozen referred to within the scope of orders shall be indicated

in the group of columns No. 030 and No. 040 with the collective

title of the group "Orders".

Procedures for the Filling in of

Annex 6

40. The credit institution shall complete Annex 6 by

indicating the characterisation of customer transactions by

countries. Annex 6 consists of the following four main reporting

groups:

40.1. code of the respective country, column No. 010 with the

title "Country code";

40.2. group of columns No. 020-040 with the collective title

of the group "Customers by the country of the beneficial owner

(BO)";

40.3. group of columns No. 050-070 with the collective title

of the group "Customers by the status of a politically exposed

person (POP)";

40.4. column No. 80 with the title "Customers by the status of

enhanced due diligence (EDD)".

41. Upon filling in a row in Annex 6, and, where necessary,

copying it and numbering it in sequence in the first column of

each row, the credit institution shall indicate the following

data in column No. 010-040 regarding customers by the country of

the beneficial owner:

41.1. the code of the country of origin of the customer in

accordance with the international standard ISO 3166-1:2013 based

on the country of domicile of the beneficial owner - in column

No. 010. For example, if the country of domicile of the

beneficial owner of the customer is a third country or a Member

State, the credit institution shall indicate the country code of

the third country or Member State which is the country of

domicile of the beneficial owner of the customer;

41.2. the actual data on the number of customers according to

the country of domicile of beneficial owners shall be indicated

in column No. 020 with the title "Number of BO customers" at the

end of the reference quarter. For example, if a customer has one

beneficial owner, the credit institution shall indicate number

"one" next to the code of the country of domicile of the

beneficial owner of the customer contained in column No. 010. If

a customer has more than one beneficial owner, and each

beneficial owner is from its own country of domicile, the credit

institution shall divide them in proportion, namely, assuming

that three beneficial owners form a whole, and each beneficial

owner constitutes 1/3 of the whole. Thus the credit institution

shall, according to the country of origin of the beneficial

owner, indicate number "0.33" next to the code of the country of

domicile of the beneficial owner of the customer contained in

column No. 10 (hereinafter - the principle of

proportionality);

41.3. the data on the actual amount of financial assets of

customers according to the country of domicile of beneficial

owners shall be indicated in column No. 030 with the title

"Financial assets of BO in total, EUR" at the end of the

reference quarter, whereas in column No. 031 these shall be

indicated by separating deposits of the customer who has a

beneficial owner from the total financial assets. The credit

institution shall comply with the principle of proportionality

referred to in Paragraph 41.2 of the Provisions when indicating

the actual amount of financial assets;

41.4. the data on the actual credit turnover of customers

according to the country of domicile of beneficial owners shall

be indicated in column No. 040 with the title "Credit turnover of

BO customers, EUR" at the end of the reference quarter. The

credit institution shall comply with the principle of

proportionality referred to in Paragraph 41.2 of the Provisions

when indicating the actual credit turnover.

42. Upon filling in a row in Annex 6, and, where necessary,

copying it and numbering it in sequence in the first column of

each row, the credit institution shall indicate in columns No.

010 and No. 050-061 the following data on customers by the status

of a politically exposed person according to their country of

domicile:

42.1. the code of the country of domicile of the customers who

are politically exposed persons shall be indicated in column No.

010 with the title "Country code" in accordance with the

international standard ISO 3166-1:2013;

42.2. the actual data on the number of customers who are

politically exposed persons from the relevant country of

residence shall be indicated in column No. 050 with the title

"Number of PEP customers" at the end of the reference

quarter;

42.3. the data on the actual amount of financial assets of

customers who are politically exposed persons shall be indicated

in column No. 060 with the title "Financial assets of PEP in

total, EUR" at the end of the reference quarter, whereas in

column No. 061 these shall be indicated by separating deposits of

the customers who are politically exposed persons from the

relevant country of domicile from the total financial assets;

42.4. the data on the actual credit turnover of the customers

who are politically exposed persons from the relevant country of

domicile shall be indicated in column No. 070 with the title

"Credit turnover of PEP customers, EUR" in the reference

quarter.

43. Upon filling in a row in Annex 6, and, where necessary,

copying it and numbering it in sequence in the first column of

each row, the credit institution shall indicate the following

data on customers by the status of enhanced due diligence (column

No. 80) according to their country of domicile:

43.1. the code of the country of domicile of the customers who

are subject to the enhanced due diligence shall be indicated in

column No. 010 with the title "Country code" in accordance with

the international standard ISO 3166-1:2013;

43.2. the actual data on the credit turnover of the customers

who are subject to the enhanced due diligence shall be indicated

in column No. 80 with the title "Credit turnover of EDD

customers, EUR" in the reference quarter.

44. When filling in Annex 6, the credit institution shall

ensure the following:

44.1. the total sum of column No. 020 with the title "Number

of BO customers" in Annex 6 corresponds to the total sum of row

No. 010 with the title "Customers in total" and column No. 010

with the title "Number of customers" in Annex 1;

44.2. the total sum of column No. 030 with the title

"Financial assets of BO in total, EUR" in Annex 6 corresponds to

the total sum of row No. 010 with the title "Customers in total"

and column No. 020 with the title "Financial assets of customers,

EUR" in Annex 1;

44.3. the total sum of column No. 031 with the title "Amount

of BO deposits, EUR" in Annex 6 corresponds to the total sum of

row No. 010 with the title "Customers in total" and column No.

030 with the title "Deposits" in Annex 1;

44.4. the total sum of column No. 040 with the title "Credit

turnover of BO customers, EUR" in Annex 6 corresponds to the

total sum of row No. 010 with the title "Customers in total" and

column No. 070 with the title "Credit turnover of customers, EUR"

in Annex 1;

44.5. the total sum of column No. 080 with the title "Credit

turnover of EDD customers, EUR" in Annex 6 corresponds to the

total sum of row No. 020 with the title "Customers subject to

enhanced due diligence" and column No. 070 with the title "Credit

turnover of customers, EUR" in Annex 1.

Procedures for the Filling in of

Annex 7

45. The credit institution shall fill in Annex 7 by providing

information regarding customers (shell arrangements) with whom

the credit institution has decided to terminate the business

relationship and their balance of deposits (deposits of the

customers are still serviced by the credit institution). Annex 7

consists of the following two main reporting groups:

45.1. the number of customers (shell arrangements), column No.

010 with the title "Number of customers";

45.2. the balance of deposits of customers (shell

arrangements), column No. 020 with the title "Balance of

deposits, EUR".

46. Upon filling in row No. 010 with the title "a+b and/or

a+b+c shell arrangements" in Annex 7 , the credit institution

shall indicate the following data in columns in accordance with

the indications of a shell arrangement referred to in Section 1,

Clause 15.1 of the Law on the Prevention of Money

Laundering and Terrorism Financing (in a combination of

indications referred to in Sub-clauses "a" and "b" and/or "a",

"b" and "c"):

46.1. the number of customers (shell arrangements) whom the

credit institution has decided to terminate the business

relationship - in column No. 10 with the title "Number of

customers";

46.2. the balance of deposits of customers (shell

arrangements) at the end of the reference quarter (as at the last

day thereof) - in column No. 20 with the title "Balance of

deposits, EUR".

47. Upon filling in row No. 020 with the title "Other shell

arrangements" of Annex 7, the credit institution shall indicate

the following data in columns based on the indications referred

to in Section 1, Clause 15.1 of the Law on the

Prevention of Money Laundering and Terrorism Financing (in a

combination, such as the indications referred to only in

Sub-clause "a" or Sub-clauses "a" and "c"):

47.1. the number of other customers (shell arrangements) with

whom the credit institution has decided to terminate the business

relationship - in column No. 10 with the title "Number of

customers";

47.2. the balance of deposits of other customers (shell

arrangements) at the end of the reference quarter (on the last

day) - in column No. 20 with the title "Balance of deposits,

EUR".

48. When completing row No. 030 with the title "Other" of

Annex 7, the credit institution shall indicate the following data

in columns:

48.1. the number of other customers who are not shell

arrangements and with which the credit institution has decided to

terminate the business relationship according to the provisions

of its ML/TF prevention policy - in column No. 10 with the title

"Number of customers";

48.2. the balance of deposits of other customers who are not

shell arrangements at the end of the reference quarter (on last

day) - in column No. 20 with the title "Balance of deposits,

EUR".

49. The credit institution shall immediately provide

information to the Finance and Capital Market Commission

regarding each case when an existing or potentially significant

non-compliance with the requirements for the ML/TF risk

management strategy has been established.

50. The credit institution shall prepare the report on the

characterisation of the ML/TF risk exposure referred to in

Paragraph 19 of these Provisions in accordance with the

requirements and procedures laid down in the Regulatory

Provisions No. 146 of the Finance and Capital Market Commission

of 14 October 2008, Regulatory Provisions for the Submission of

Electronically Prepared Reports.

51. If the Finance and Capital Market Commission finds that

the report on the characterisation of the ML/TF risk exposure is

incomplete or inaccurate, it shall notify the person who has

submitted the report thereof. The credit institution shall submit

the corrected report to the Finance and Capital Market Commission

not later than on the following working day after receipt of the

notice on the existence of errors from the Finance and Capital

Market Commission, unless the Finance and Capital Market

Commission has specified another deadline.

52. If the credit institution finds that the report on the

characterisation of the ML/TF risk exposure is incomplete or

inaccurate, it shall immediately inform the Finance and Capital

Market Commission thereof and submit a corrected report.

VI. ML/TF Risk

Stress Testing and Methods for the Capacity of the Credit

Institution to Manage ML/TF Risk

53. The credit institution shall, on regular basis, but at

least once a year, perform ML/TF risk stress tests regarding at

least the following risk factors:

53.1. the termination of correspondent relationships with the

direct correspondents of the credit institution in cooperation

with which payments are made in the relevant currencies;

53.2. the impact of geopolitical events;

53.3. the impact of restrictions on activity imposed within

the scope of sanctions or corrective measures, which have been

applied to the credit institution.

54. The credit institution shall develop stress test scenarios

according to the ML/TF risk inherent to the activity of the

credit institution.

55. The credit institution shall gather results of stress

tests, assess the risks identified within the scope of the tests

and their impact on liquidity, capital and financial indicators,

as well as provide a report to the board of directors.

56. The credit institution shall submit to the Finance and

Capital Market Commission the results of stress tests and the

decisions taken on their basis regarding ML/TF risk management

within 30 days after such decisions have been taken.